- The median percentage of CRE loan modifications to non-owner-occupied borrowers rose 65 bps through the first 9 months of 2024.

- Smaller banks saw the largest percentage spike (217%), though absolute modification levels remain lower than mid- and large-sized banks.

- Only 11% of the $755M in office CMBS loans maturing in September were paid off, with nearly half securing short-term extensions.

- Rising delinquencies, especially in office and multifamily, are driving lenders to reconsider extensions and demand more concessions from borrowers.

- Private equity and credit funds are stepping in as alternative capital sources but with higher return demands and stricter terms.

US banks continued to modify commercial real estate loans through Q3 as a means to manage risk and avoid defaults, as reported by GlobeSt.

By The Numbers

According to Moody’s Ratings, CRE loan modifications for NOO borrowers increased by 65 bps over the last 9 months. Smaller banks reported the sharpest rise, with modifications spiking 217%—from 10 to 32 bps.

However, absolute levels remain modest compared to mid-sized banks, which saw the largest total percentage of modifications, rising 61% to 193 bps. The largest banks (>$700B) reported a modest 14% increase, reaching 79 bps.

The rise in modifications reflects ongoing market stress, as Federal Reserve rate cuts have offered little opportunity for refinancing. Extensions remain the preferred strategy for lenders and borrowers alike to keep loans performing and delay losses.

Still Extending & Pretending

The “extend-and-pretend” approach—granting short-term loan extensions to avoid forced asset sales—has dominated the CRE market, particularly for high-quality properties. However, its effectiveness is waning.

In September alone, only 11% of the $755M in office CMBS loans maturing were paid off, compared to a 31% YTD payoff rate. Nearly half of the remaining loans were extended, reflecting lender reluctance to realize steep losses.

But lenders are losing patience, especially for underperforming assets. “Even institutional, great household names have hit the end of their rope,” said Glenn Grimaldi, CEO of Naftali Credit Partners.

Banks, too, are more prepared to foreclose or accept discounted transactions rather than extend them indefinitely.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Subscribe

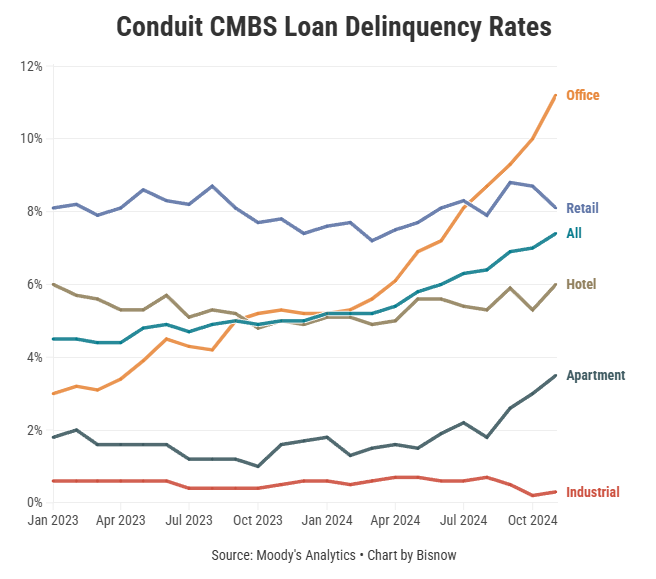

Rapidly Rising Delinquencies

Office delinquencies have accelerated, reaching 11.2% in November—three times higher than at the start of 2023. Moody’s expects the rate to peak above 14% in 2025.

Multifamily assets also show stress, driven by rising operating costs and slowing rent growth.

These pressures have started to expose market realities. Seven properties in 2024 have already sold at losses exceeding $100M from their prior sale prices, up from just two in 2023.

“There’s maybe a sign of capitulation,” said Matt Reidy, Director at Moody’s Analytics. “Lenders are saying, ‘We just need to take our lumps.’”

Private Capital Steps Up

As banks tighten lending, private equity and private credit funds are filling the gap, providing capital for landlords seeking loan extensions or modifications. But this new wave of liquidity comes at a cost.

“Returns that private equity and private credit are getting now look like equity returns at senior debt levels,” said Grimaldi, whose firm is finalizing a $300M raise. Private investors often demand preferred returns and first-dollar repayment structures to minimize downside risk.

For larger banks, channeling capital through private vehicles has become an attractive alternative to direct lending, helping mitigate regulatory concerns while maintaining exposure to CRE assets.

Risks of Delaying

While extensions have delayed a full-blown market disruption, they come with risks. The Federal Reserve Bank of New York warns that extend-and-pretend strategies are stacking loan maturities into future years, amplifying the risk of a sudden, widespread capital hit if conditions don’t improve.

Additionally, these strategies are stifling new lending. “It’s not only pushing the can down the road but also limiting capital going to more profitable projects,” said Trepp Chief Economist Rachel Szymanski.

Market Reset Ahead

The extend-and-pretend era is nearing its end. As lenders face growing delinquencies and borrowers exhaust their options, more distressed assets are expected to hit the market in 2025, exposing sellers to significant price corrections.

“You will see some distress [in 2025], but alternative sources of capital will take up the slack where banks pull back,” Grimaldi said.

For investors, the coming year presents a window of opportunity as sidelined capital waits to acquire assets at steep discounts. While this market reset may be painful for asset owners, it could ultimately help recalibrate the CRE sector after years of uncertainty.