- Prime office buildings in Midtown Manhattan, such as those on Park Avenue, are fully leased with rents exceeding $275 PSF, while older buildings languish with vacancies and lower rents.

- Financial firms are driving demand for high-end spaces, with tenants like Citadel, Elliott Investment Management, and Blue Owl Capital expanding their footprints.

- With limited new construction and top-tier space almost fully occupied, demand may shift to other Manhattan submarkets offering relatively affordable rents.

Manhattan’s office market is experiencing a tale of two extremes, as reported by Bloomberg. Trophy buildings in Midtown, particularly along Park Avenue, are commanding record rents and full occupancy, driven by demand from financial firms and proximity to Grand Central Terminal.

Conversely, many older buildings face climbing vacancies and dwindling interest, underscoring a widening gap between the city’s top and bottom-tier office assets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

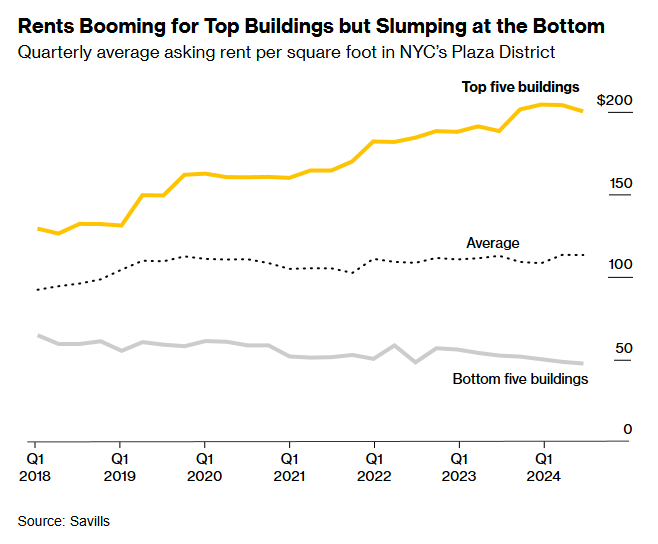

Booming Trophy Market

Top-tier properties in Midtown, especially those in the Plaza District, are seeing unprecedented demand.

Park Avenue’s Seagram Building, for instance, boasts full occupancy, with asking rents reaching $275 PSF. This trend extends to other trophy towers, like 280 Park Avenue and SL Green’s One Vanderbilt, both fully leased with high-profile tenants.

The competition for these premier spaces has intensified, with firms like Citadel, Elliott Investment Management, and JPMorgan Chase (JPM) securing large office footprints. Blue Owl Capital also expanded its space at the Seagram Building by 73%, citing the benefits of being near clients and peers in the financial corridor.

Struggling Older Properties

While trophy assets thrive, many older buildings in Midtown face significant challenges. At 425 Madison Avenue, a 19-story building constructed in 1927, nearly 25% of space is vacant, with asking rents under $37 PSF—less than half the citywide average.

This disparity is worsened by tenant preferences for modern, transit-accessible spaces, coupled with limited new construction in Manhattan. Developers have largely pulled back since the pandemic, and the borough has just 2.5 MSF of office space under construction, 80% of which is already pre-leased.

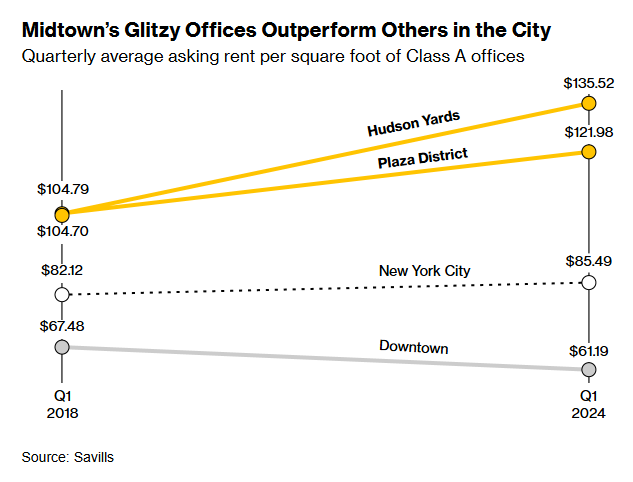

Hudson Yards and Beyond

The Hudson Yards district continues to attract high-profile tenants, commanding some of the highest rents in the country.

At the Spiral, a 66-story skyscraper, HSBC Bank USA (HSBC) reports an 80% office-utilization rate, doubling the occupancy of its previous location. Neighboring towers, including those in Brookfield’s (BN) Manhattan West complex, are also renewing leases at much higher rates.

With trophy spaces nearing full capacity, demand is beginning to trickle into other Manhattan submarkets. Lower Manhattan’s Brookfield Place, for example, is in talks with Jane Street Group for an expansion, reflecting the growing interest in high-quality but still affordable properties outside Midtown.

What’s Next?

Manhattan’s office market will likely continue to see a divergence between top-tier buildings and older assets. As trophy spaces fill up and rents soar, companies seeking value may increasingly turn to well-located properties in Lower Manhattan and other emerging submarkets.

For landlords of aging buildings, the challenge remains: invest in significant renovations or risk obsolescence in a market increasingly dominated by premium, amenity-rich spaces.nt activity, the rise in vacancy poses challenges for landlords. Average rents in the metro grew by 8.1% YoY to $6.17 PSF, still trailing higher-priced markets like Orange County ($15.95) and Los Angeles ($15.05).

With significant new developments in the pipeline and steady investor interest, Dallas is poised to maintain its position as a top industrial market, even as it navigates the challenges of rising vacancy and a shifting demand landscape.