- CMBS issuance hit $115B in 2024, up 150% YoY from 2023, as investor demand for securitized loans on performing assets surged.

- The market continues to grow in 2025, with $17B issued in the first six weeks of the year, doubling early 2023 volumes.

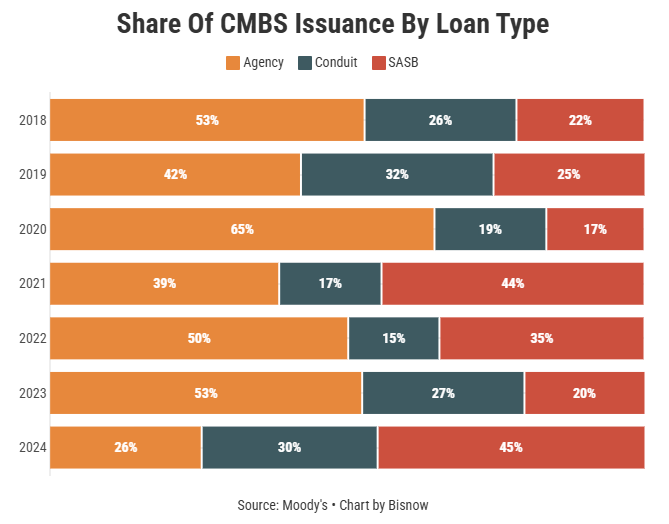

- In 2024, single-asset, single-borrower (SASB) loans accounted for 45% of CMBS volume, while conduit loans and agency-backed debt shifted.

- Despite rising issuance, CMBS delinquency rates remain elevated, with office loan defaults hitting a record 11% in December.

After many years of sluggish activity, the commercial mortgage-backed securities (CMBS) market roared back to life in 2024, according to Bisnow.

By The Numbers

According to Kroll Bond Rating Agency (KBRA), CMBS closed out the year with $115B in issuance—150 % higher than in 2023. This momentum has continued into 2025, with $8B issued in January and another $9B in the first half of February.

CMBS debt issuance gained traction in 2H24, fueled by major single-borrower transactions. In October alone, 15 SASB loans exceeded $1B each, compared to just four such loans in all of 2023.

Shifting Market Composition

The composition of CMBS loans has evolved to meet shifting market conditions:

- SASB Loans Surge: SASB loans made up 45% of issuance in 2024, more than doubling from 2023 levels. These loans—often backed by trophy assets like Manhattan’s Seagram Building, which secured a $1.2B loan in February—have become the preferred financing structure.

- Conduit Loans Rebound: Conduit loans, which bundle multiple properties into a single security, comprised 30% of CMBS volume in 2024, continuing a steady upward trend.

- Agency Loans Decline: Fannie Mae (FNMA) and Freddie Mac-backed CMBS issuance fell to 26% of market share after dominating over half of CMBS volume in 2023.

“SASB has been backfilling where conduit and agency is lacking—it’s like a full circle,” said Twinkle Roy, an economist at Moody’s.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Investor Demand Driving Activity

Investor appetite for high-quality, cash-flowing assets—particularly multifamily, industrial, and Class A office properties—has driven CMBS issuance. Banks, still cautious after years of distress, have also warmed up to structured debt as an alternative to keeping assets on their balance sheets.

The Federal Reserve’s shift to a “higher-for-longer” interest rate environment has pushed property owners to secure 5-year loans instead of the traditional 10-year CMBS debt. Nearly 70% of conduit deals in 2024 were for 5-year loans, up from 42% in 2023, according to KBRA.

Office Still a Concern

Despite the resurgence in issuance, CMBS delinquency rates remain elevated, especially in the office sector. Office-backed CMBS debt hit an all-time high delinquency rate of 11% in December, reflecting ongoing challenges for underperforming properties.

While the overall delinquency rate dipped slightly in January, analysts believe distress levels haven’t peaked yet.

“Today’s issuance is at a new basis, at a different interest rate environment, and it is, generally speaking, better-quality assets,” said Aaron Jodka, director of research for U.S. capital markets at Colliers. “That’s allowing us to see strong new issuance alongside elevated delinquency rates.”

Looking Ahead

CMBS issuance is expected to continue its upward trajectory in 2025, with SASB and conduit loans leading the charge. New York City remains a major hotspot, with recent deals including a $3.5B loan for Rockefeller Center, a $1.1B loan for 3 Bryant Park, and the $1.2B Seagram Building refinancing.

As the market stabilizes, more banks are also moving away from “extend-and-pretend” strategies, pushing borrowers to refinance rather than delay maturities. With Federal Reserve rate cuts no longer a near-term certainty, CMBS debt remains a critical funding source for large commercial deals in a shifting financial landscape.