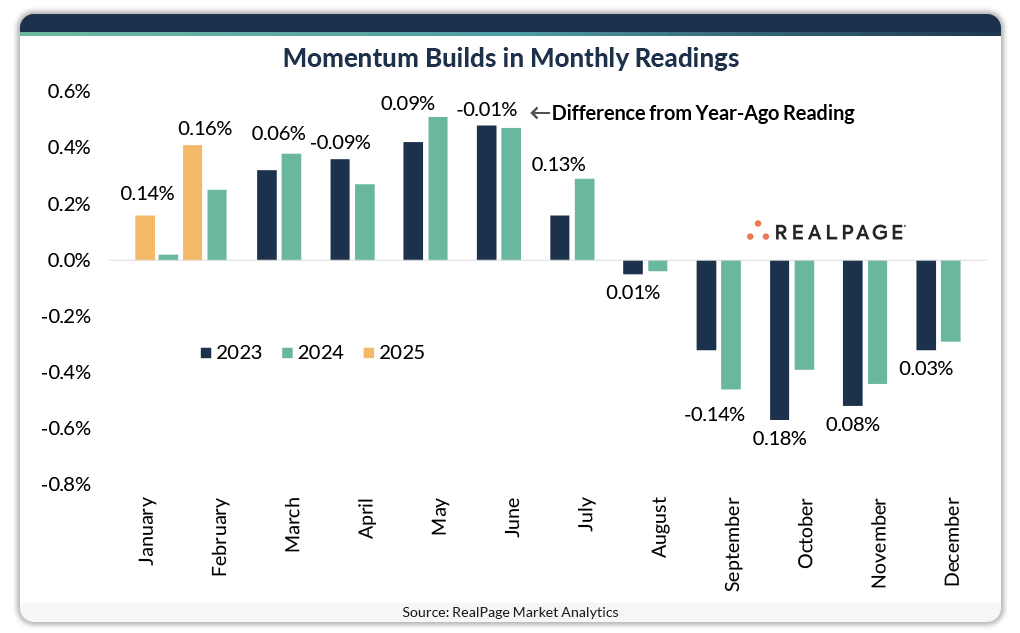

- Apartment rents grew 0.41% MoM in February, the highest growth for the month since 2022, signaling some stabilization after two years of stagnation.

- The national occupancy rate rose 10 bps to 95% in February, with 80% of US markets showing MoM growth.

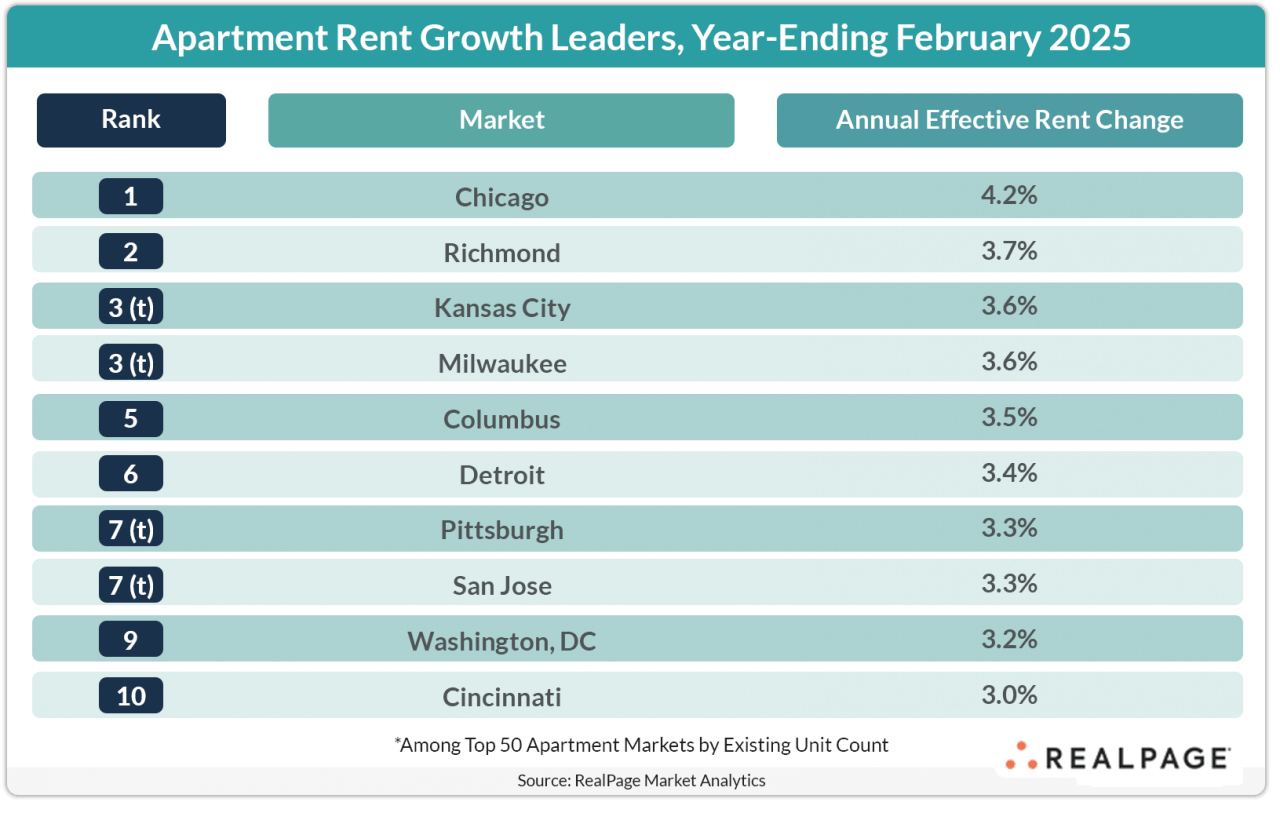

- Chicago led the nation in rent growth, up 4.2% YoY, while Austin faced more rent cuts, posting the steepest annual drop at 7.2%.

US apartment rents saw modest growth in February, continuing January’s positive trend. This marks the highest February reading since 2022, pointing to a potential stabilizing market after nearly two years of stagnant rents.

Steadily Increasing Occupancy

According to RealPage, rents for market-rate apartments rose 0.41% MoM in February, slightly below the long-term February average of 0.53%.

Ehe effective asking rent in professionally managed market-rate units for the 12 months ending in February 2025 inched up 0.8%. While still below long-term norms, this was the highest annual growth reading since July 2023, signaling a return to more typical rent dynamics.

The MoM growth in February, at 0.41%, is also an improvement over the same period in 2024 (0.25%), suggesting overall rent growth may pick up momentum as the year continues.

Steadily Increasing Occupancy

Along with rent growth, occupancy levels also showed positive signs in February. The national occupancy rate rose by 10 bps to 95%, a 90-bp YoY gain.

Demand continued to push occupancy higher, especially in markets with high levels of apartment supply, such as Phoenix, Fort Worth, and Orlando, where occupancy rose by 20 bps MoM. Overall, 80% of US markets recorded MoM occupancy increases, a higher-than-usual share for February.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

RealPage Chief Economist Carl Whitaker pointed out this trend supports the narrative that demand is catching up with supply, particularly as new construction slows down in many major markets. Rising occupancy suggests operators can leverage demand to stabilize properties, even as the market absorbs new inventory.

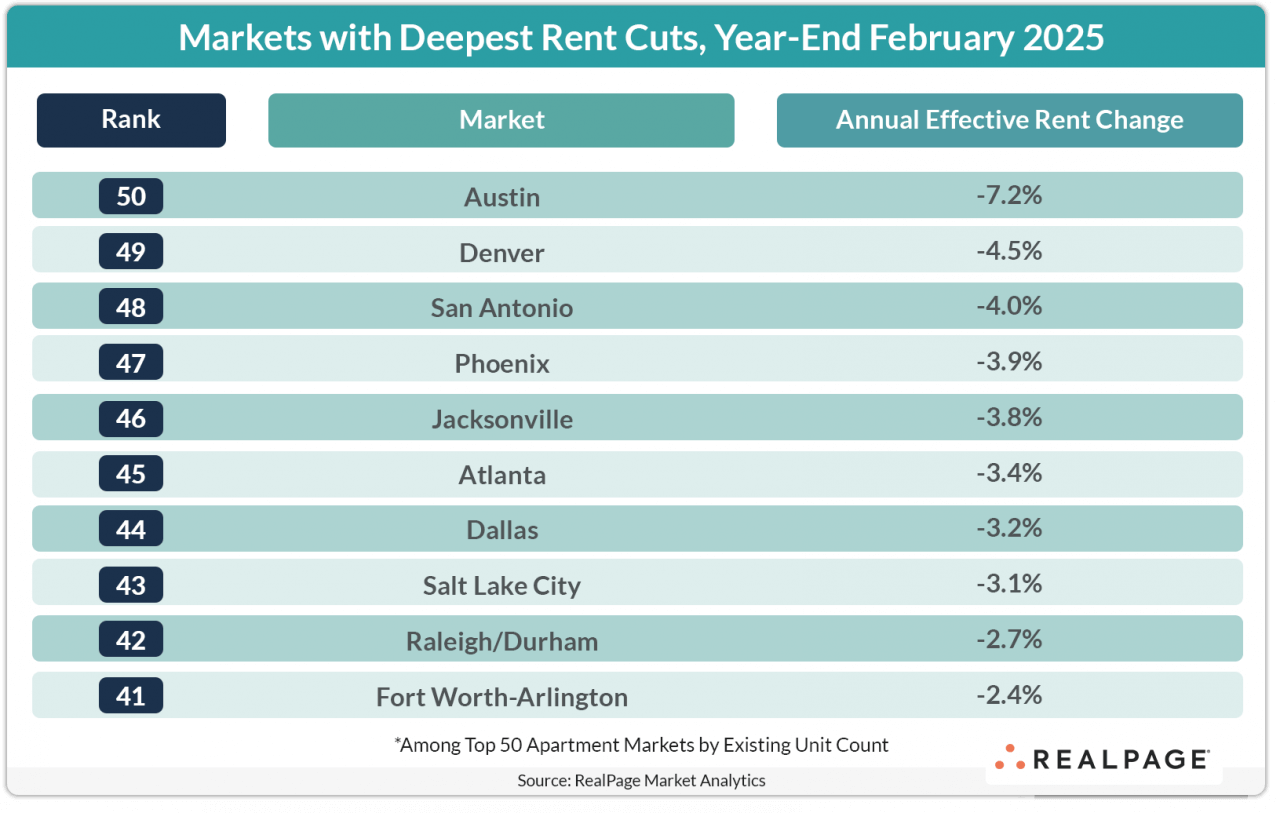

Supply-Driven Rent Cuts

Despite the positive trends, rent cuts continued in about one-third of the nation’s largest apartment markets.

These rent cuts are generally concentrated in markets where supply is high, including Austin, which recorded the deepest YoY rent cut of 7.2%. While this was a slight improvement from past months, Austin remains a challenging market for landlords, with rent cuts still prevalent.

Other markets have seen more favorable conditions. Chicago posted the highest rent growth among major US markets, up 4.2% YoY. Other top-performing markets included Richmond (3.7%), Pittsburgh (3.3%), San Jose (3.3%), and Washington, DC (3.2%).

Competing For Tenants

The use of concessions also continued to rise in February, revealing the stiff competition these days in the multifamily market. The average concession for stabilized apartment assets was approximately 31 days discounted, up 1% from February 2024.

Concessions are more common in the South, particularly in markets like Cape Coral, San Antonio, and Crestview-Destin, where up to 25% of vacant units offer discounts. The popularity of concessions highlights how operators are adjusting to attract tenants, particularly in markets with more vacancies.

As supply and demand dynamics evolve, concessions are expected to remain a key tool for property managers to maintain high occupancy rates.