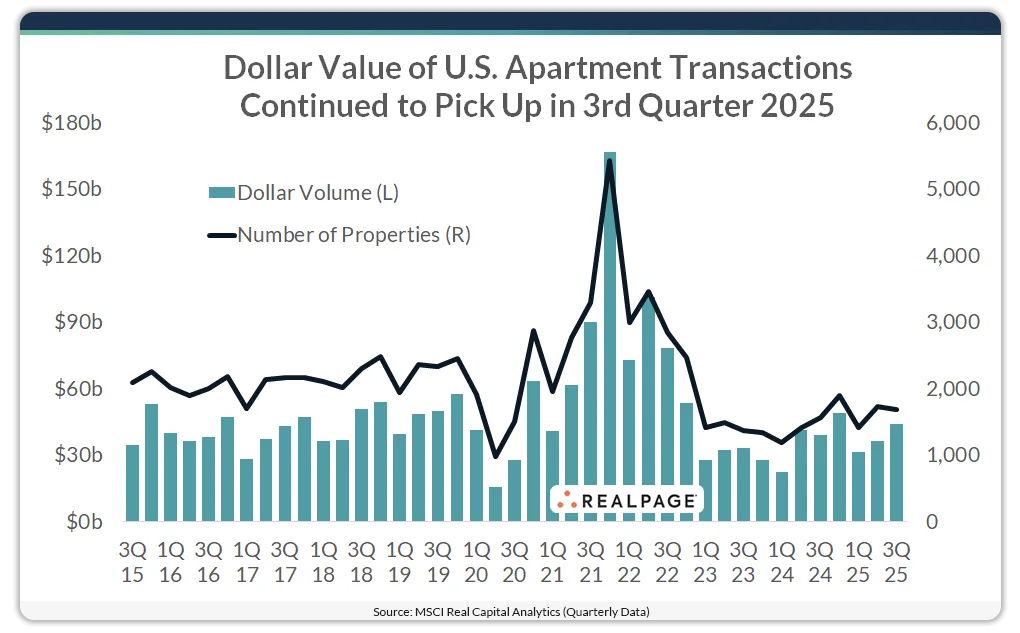

- US apartment transaction volume reached $43.8B in Q3 2025, up 13% year-over-year and 21% from Q2.

- The number of assets sold declined slightly from the prior quarter, with 1,680 properties trading hands.

- Cap rates rose to 5.63%, the highest since 2017, but apartments still offer the lowest cap rates among major asset classes.

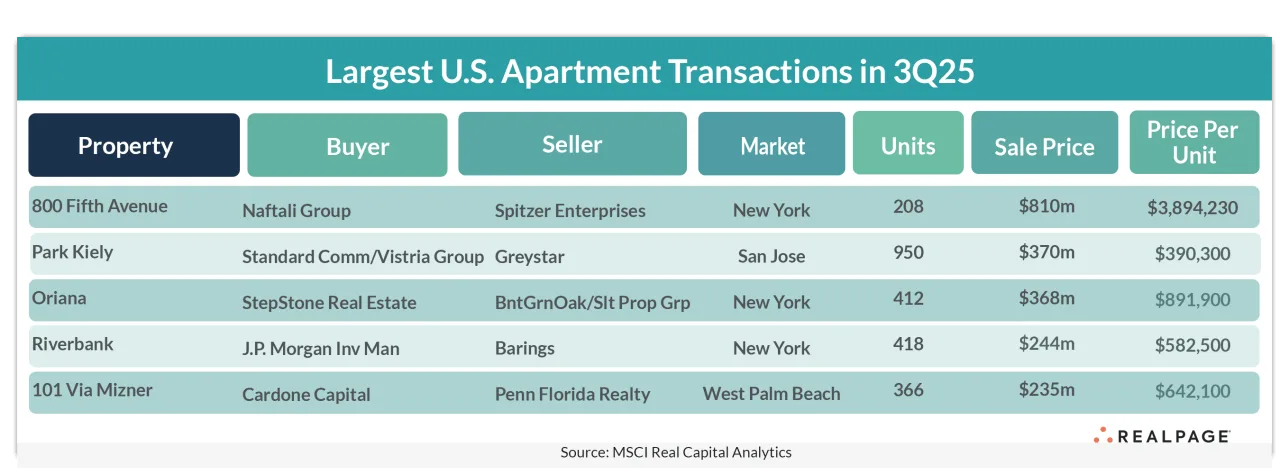

- The quarter’s largest deal was Naftali Group’s $810M purchase of 800 Fifth Avenue in Manhattan, at nearly $3.9M per unit.

A Surge in Dollar Volume

RealPage reports that multifamily investment activity remained strong in Q3 2025. According to MSCI Real Capital Analytics, investors poured $43.8B into apartment deals between July and September. That marked a 13% increase from a year earlier and a 21% jump from Q2. While the number of properties sold slipped slightly to 1,680 from 1,728, higher pricing helped boost overall volume.

However, the market still lags pre-pandemic norms. The five-year quarterly average remains significantly higher, at about $55.6B.

Prices Stay High as Cap Rates Climb

Apartment pricing held firm. The average price per unit hit $227,167 in Q3, continuing a stretch of elevated valuations. Unit pricing has stayed above $200,000 in 15 of the past 17 quarters. Before 2021, average per-unit prices hovered around $151,000.

Cap rates for apartment deals climbed to 5.63%, the highest level in more than eight years. Despite rising rates, apartments remain more attractive than other major property types. They still offer the lowest cap rates in commercial real estate.

Strong Annual Growth

In the year ending Q3 2025, apartment sales reached $159.9B. A total of 6,717 properties changed hands during that period. Compared to the prior 12 months, dollar volume rose by 23% and transaction count increased by 22%.

Sales dropped in 2020 during the pandemic, when about 7,300 properties sold for $148.2B. In 2021, pent-up demand caused a surge, with 13,500 properties trading at a total of $359.4B. While 2025 levels remain well below that peak, the market continues to recover.

NYC Leads the Quarter’s Top Deals

The five largest apartment transactions of the quarter all exceeded $235M. Three of them occurred in New York City, confirming the metro’s dominance in high-value multifamily trades.

- 800 Fifth Avenue (New York, NY): Naftali Group acquired the 208-unit luxury building for $810M in August. The firm plans to demolish the 1979-built tower and replace it with high-end condos. The site includes 35,000 SF of office and 3,000 SF of retail.

- Park Kiely (San Jose, CA): Standard Communities and The Vistria Group bought this 948-unit property from Greystar for $370M. The buyers will convert it to affordable housing and invest over $19M in renovations.

- Oriana (New York, NY): StepStone Real Estate paid $367.5M for the 412-unit building in Midtown East. Built in 1982 and last renovated in 2016, the property features rooftop decks, a penthouse lounge, and a vintage arcade.

- Riverbank (New York, NY): J.P. Morgan Investment Management bought the 418-unit tower for $243.5M. The 44-story building in Hell’s Kitchen was originally developed as condos in 1987.

- 101 Via Mizner (Boca Raton, FL): Cardone Capital acquired this 366-unit asset for $235M. The previous owner filed for Chapter 11 in January. Cardone is considering a condo conversion.

Looking Ahead

Multifamily deals are likely to continue rising into 2026, especially if interest rate volatility stabilizes. Investors are showing renewed interest in both stabilized and redevelopment assets. Major markets like New York and San Jose remain magnets for large-scale capital.

Even with rising cap rates, strong pricing and steady demand keep multifamily properties in favor. Apartments continue to play a key role in diversified real estate portfolios.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes