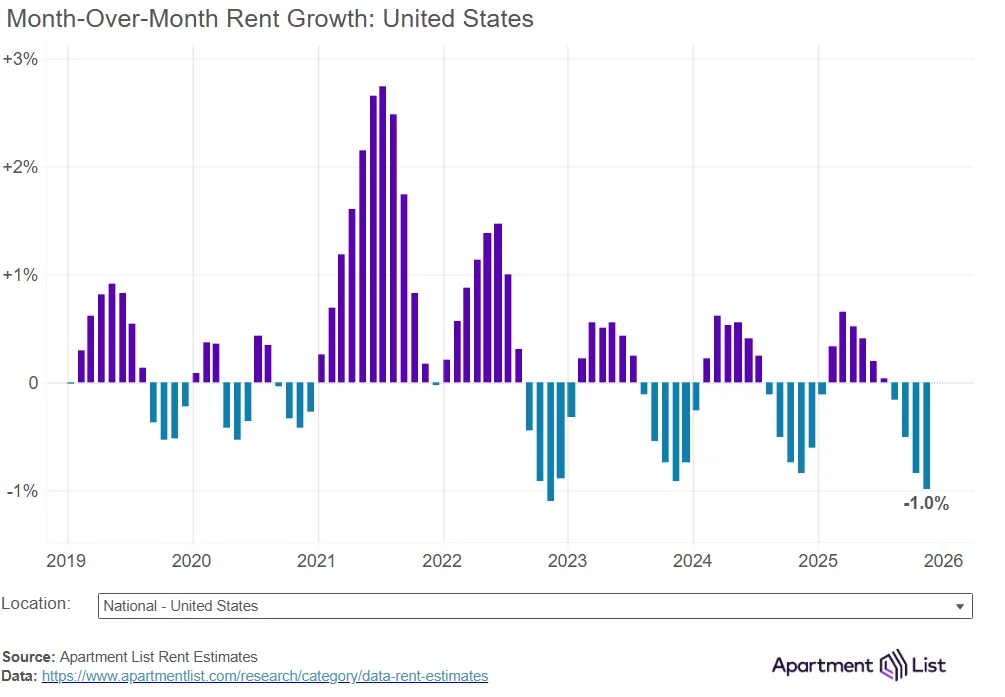

- National median rent fell 1.0% in November, marking the fourth straight monthly decline. Rents are now down 1.1% year-over-year.

- Vacancy rate reached a record-high 7.2%, driven by a surge in new supply and weaker rental demand.

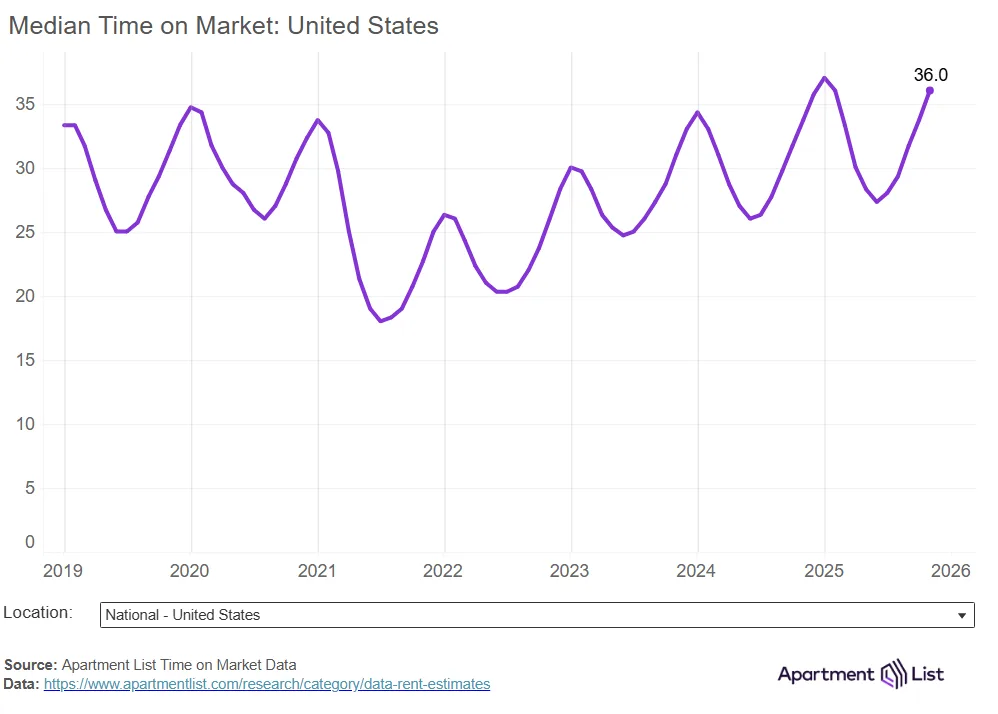

- Leasing times are rising, averaging 36 days—up from 34 a year ago and double the 2021 average.

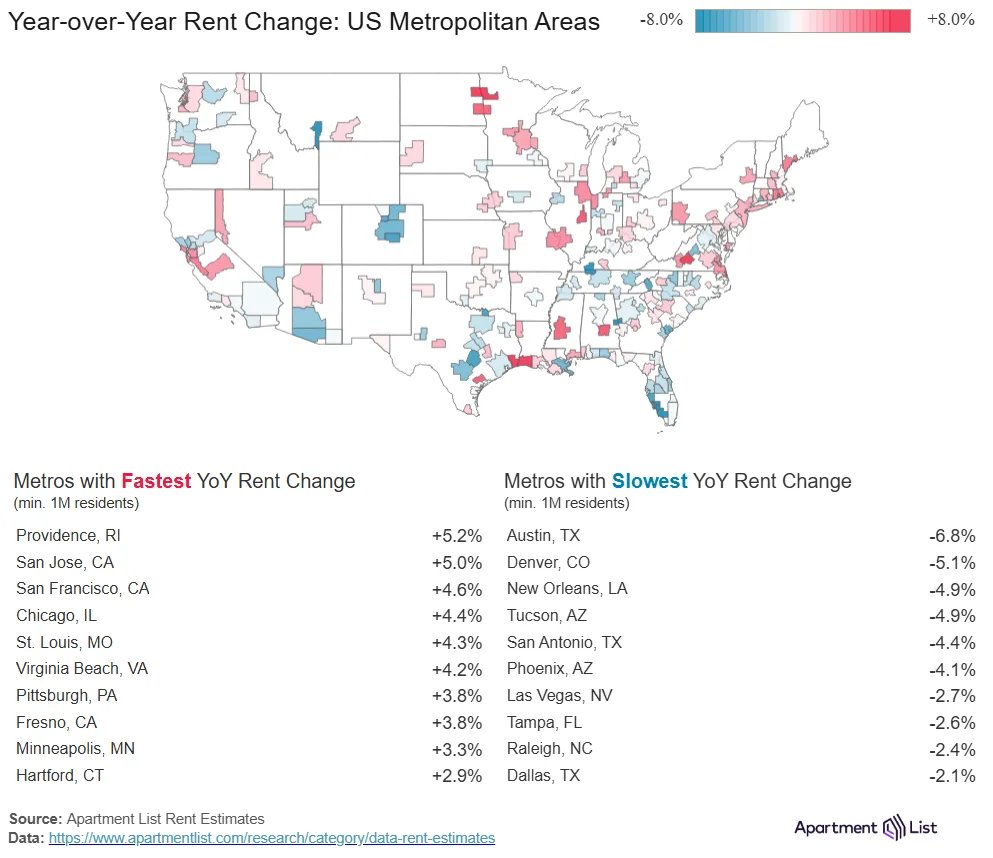

- Sun Belt markets lead rent declines, with Austin down 6.8% annually. Providence, RI, saw the fastest growth at +5.2%.

Another Month, Another Dip

Apartment List reports that the national median rent dropped 1.0% in November to $1,367. This marks the fourth monthly decline in a row. Rents now sit 1.1% lower than a year ago and 5.2% below the August 2022 peak.

While seasonal slowdowns are expected, the timing has shifted. Rent prices began falling in August for the third year in a row, earlier than in most pre-pandemic years.

Earlier in 2025, annual rent growth looked like it might turn positive. However, weak summer demand reversed that trend.

Supply Surge Meets Soft Demand

A historic wave of new apartments continues to reshape the market. Developers delivered over 600,000 new multifamily units in 2024—the highest in nearly four decades. In 2025, deliveries slowed but stayed elevated. More than 240,000 units came online in the first half of the year, 31% above the 10-year average for that period.

This supply increase pushed the national multifamily vacancy rate to 7.2% in November. That’s the highest level since Apartment List began tracking this metric in 2017. Property owners face more competition and have less leverage on pricing due to the growing inventory.

At the same time, a cooling labor market has dampened renter demand. This combination has prolonged the soft conditions in many markets.

Leasing Takes Longer as Vacancies Rise

Units are also sitting on the market for longer. In November, it took an average of 36 days for a listed apartment to lease—up from 34 days last year and 18 days in 2021.

This trend reflects the slowdown in demand and the seasonal off-peak. It’s the fifth straight month that leasing times have increased.

Sun Belt Markets See the Steepest Declines

Rent trends vary sharply by region. Of the 54 largest US metros, 52 saw rents fall month-over-month in November. Rents dropped year-over-year in 29 of them.

The steepest declines appeared in the South and Mountain West. Austin, TX, saw the biggest drop, with median rent falling 6.8% over the past year. Rents there are now more than 20% below their 2022 peak. Austin also leads the nation in new housing permits, underscoring the link between supply and falling rents.

Other Sun Belt metros with high permitting activity—like Phoenix, Denver, Dallas, San Antonio, and Orlando—also experienced sharp rent declines.

In contrast, Providence, RI, posted the fastest annual rent growth at +5.2%. The city has benefited from an influx of renters looking for affordable options outside of Boston and New York. Since 2020, rents in Providence have jumped more than 40%—the largest increase among major metros.

What’s Next

The market continues to show signs of softness. Rent prices are falling, vacancies are high, and new units keep entering the market. Although construction has started to slow, elevated supply levels remain.

Once this wave of new supply is absorbed, the market may tighten. Developers will likely pull back, and pricing power could return. However, weaker labor market conditions and softening construction sentiment suggest that recovery will take time.

Bottom Line

Renters still have the upper hand as more supply hits the market and leasing slows. While rents remain above pre-pandemic levels, the recent cooling is likely to continue into early 2026.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes