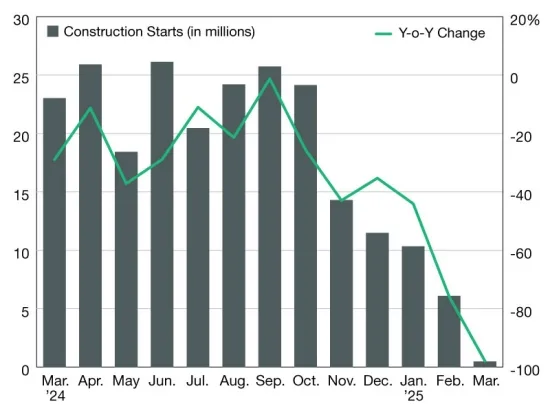

- Industrial construction starts dropped by over 40% in summer 2025 compared to 2024.

- Monthly activity declined steadily, with August 2025 at just 9.8 MSF, well below prior years.

- Year-over-year drops reached double digits in the first five months of 2025.

- The slowdown points to more measured development amid shifting market conditions.

Summer Drop Signals New Industrial Momentum

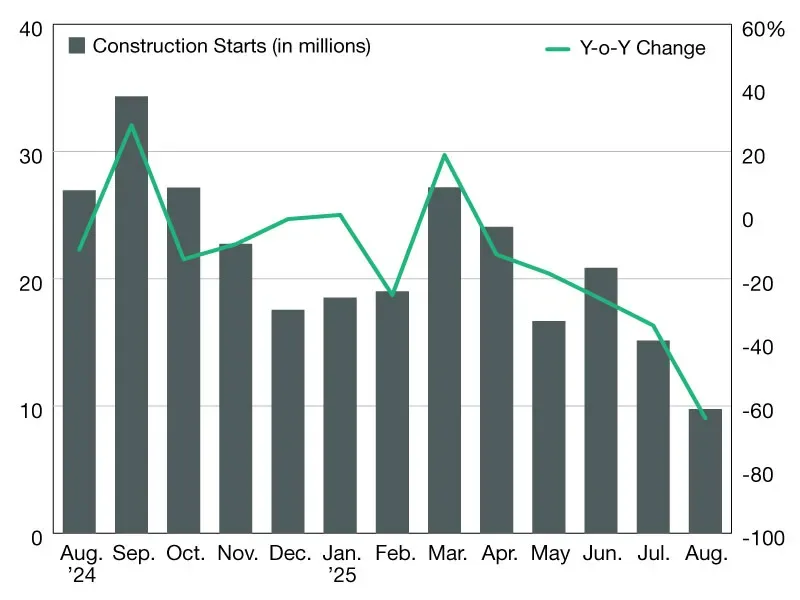

The Commercial Property Executive reports that industrial construction momentum slowed dramatically across the US in 2025, data from Yardi Matrix and CommercialEdge show. Groundbreakings in the summer totaled 45.8 MSF, representing a 41.7% drop from summer 2024’s 78.5 MSF and an even steeper decline from the 88.8 MSF seen in 2023.

The decrease was reflected monthly, with starts falling from 20.9 MSF in June to only 9.8 MSF by August. This marks a stark departure from the steadier activity levels seen in previous summer periods.

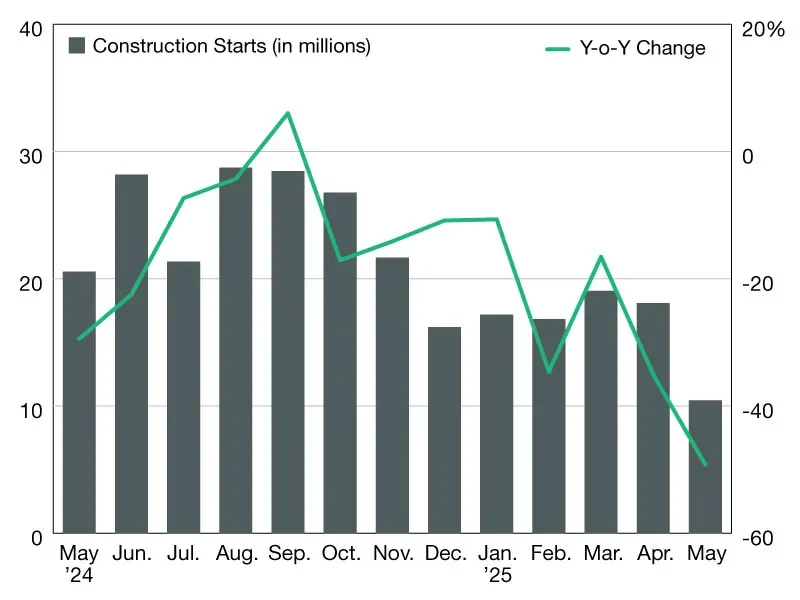

Spring and Early 2025 Provide Limited Cushion

Industrial construction starts showed relative resilience in spring, totaling 68 MSF. That’s just 4% below 2024’s spring mark. A strong March helped offset a weak start to the year. Winter 2025 posted a 10.7% decrease compared to the previous winter.

Early 2025’s slow momentum became clear as monthly starts dropped by double-digit percentages year-over-year. January fell by 26.9%, while February and March were also well below 2024 levels. This pattern mirrored broader real estate trends, with weaker-than-expected spring performance across multiple sectors.

Year-over-Year Contraction Dominates

After a volatile but relatively strong 2024, industrial momentum turned negative in late 2024 and continued into 2025. By May 2025, construction starts had dropped more than 40% from the previous year. This pattern of double-digit declines became a clear signal that developers remained cautious. Cooling demand and economic headwinds weighed heavily on sentiment.

Why It Matters

The sharp slowdown in industrial construction reflects shifting market conditions—higher interest rates, tempered tenant demand, and a shift away from the aggressive expansions of prior years. Developers now appear to be calibrating to market realities, prioritizing a strategic pace. Although the current industrial pipeline is smaller, this reset may lay the groundwork for stability if fundamentals improve.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes