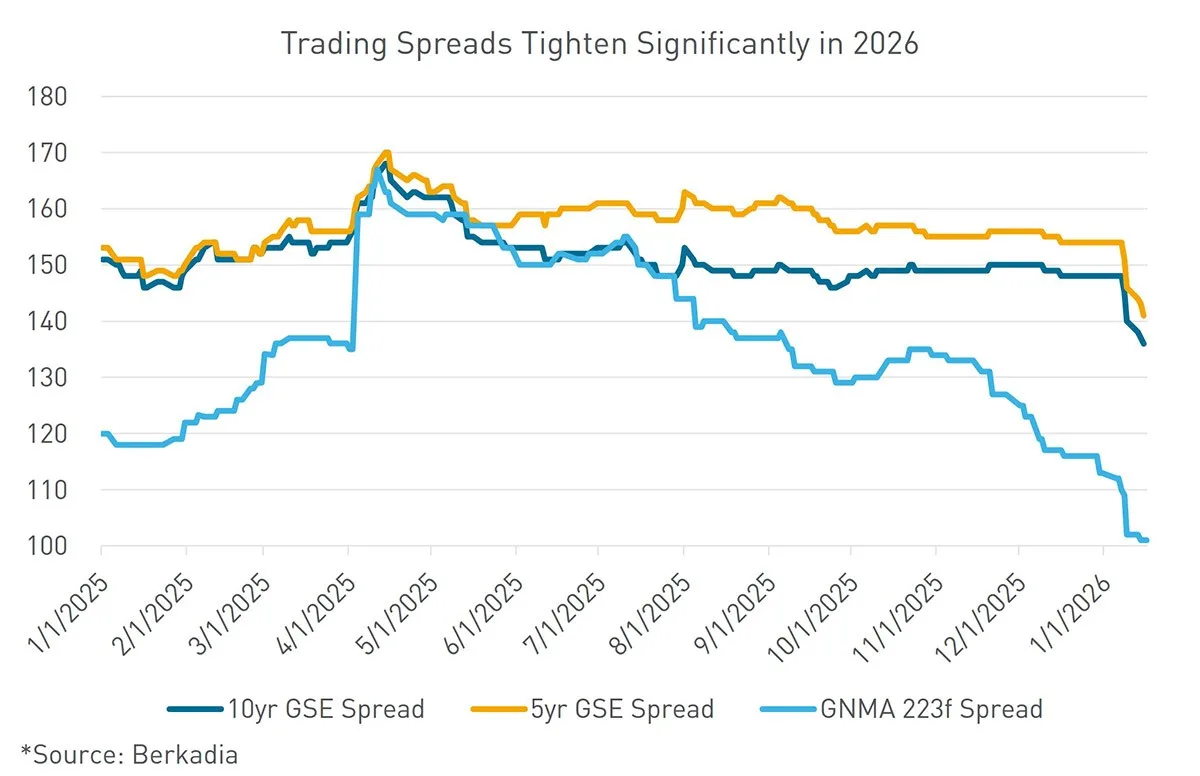

- Agency CMBS spreads tightened by roughly 15 bps in January 2026 following policy moves and a presidential announcement.

- FHFA increased agency multifamily loan purchase caps to $88B per agency, supporting affordable housing financing.

- Ginnie Mae spreads are at their tightest since May 2022, driven by dealer demand and limited issuance.

- The Fed’s future moves remain uncertain, with labor market softness and ongoing political scrutiny for Chair Powell.

Strong Demand for Agency CMBS

Agency CMBS markets kicked off 2026 with tightening trading spreads and abundant liquidity, reflecting renewed investor appetite. A major policy announcement directed GSEs to purchase $200B in mortgage-backed securities in an effort to lower rates. According to Berkadia, this move pushed Fannie Mae DUS spreads about 15 bps tighter across tenors, even as issuance volumes lagged typical weekly levels.

Multifamily Lending Caps Raised

The Federal Housing Finance Agency (FHFA) raised agency multifamily loan purchase caps to $88B per agency for 2026, a 20.5% increase year-over-year. The continuing 50% mission-driven business requirement and a workforce housing exemption ensure robust capital flows to affordable and workforce housing. Third-party lenders—including life companies, banks, and debt funds—have also signaled strong activity for the year ahead.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Ginnie Mae Spreads Tighten Further

Ginnie Mae (GNMA) 223f spreads reached their tightest levels since May 2022, thanks largely to steady dealer demand and the effects of recent policy signals. Temporary issuance slowdowns and continued appetite from broker-dealers accelerated the tightening, even as volume begins to rebound. This continued compression aligns with broader patterns in CMBS markets, where tightening spreads have pointed to a recovery in lending momentum. The Trump administration’s push for increased purchases of mortgage-backed securities further reinforced spread compression early in 2026.

Fed Outlook Remains Unclear

The Federal Reserve cut rates by 25 bps in December. However, the path forward remains unclear due to mixed inflation and labor data. Inflation gauges have moderated, reducing immediate pressure for more hikes. Meanwhile, softness in labor market indicators is now the main reason for potential rate cuts. Ongoing political scrutiny of Chair Powell and uncertainty around Fed leadership continue to fuel speculation about future moves. These dynamics are likely to affect agency CMBS and broader CRE capital markets.