- Data center construction in primary US markets declined for the first time since 2020.

- Vacancy rates remain at a record low of 1.4% across major data center hubs.

- Rising costs and financing hurdles are driving rent growth and shifting activity to smaller markets.

- Preleasing and off-market deals are increasing as supply tightens and demand rises.

Supply Shortfall Hits Key Markets

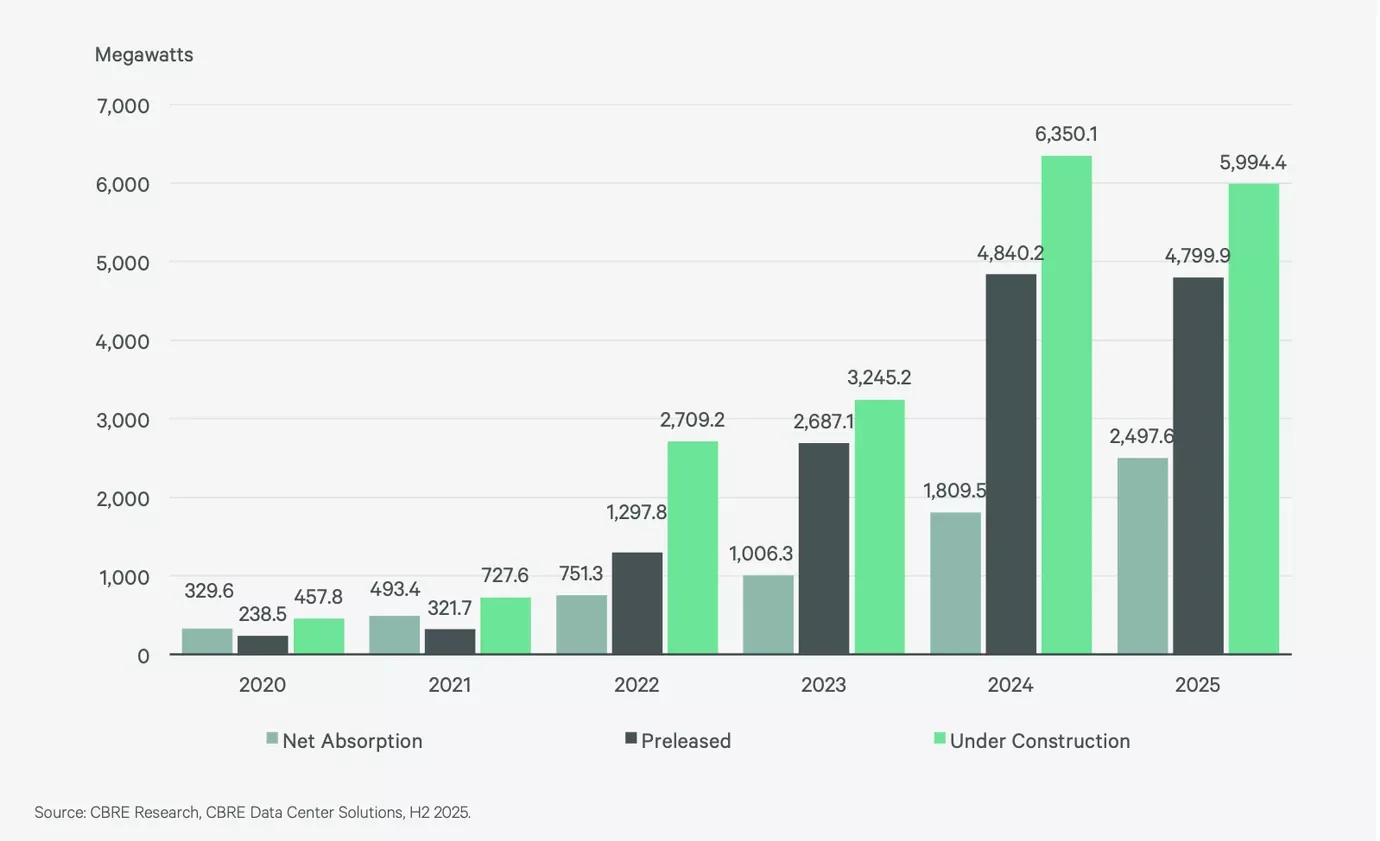

Bisnow reports that the pace of data center construction is slowing in the largest US markets, marking the first year-over-year decline in capacity underway since 2020. According to new data from CBRE, about 5,994 megawatts of data center projects were under construction in the primary hubs by the end of 2025, down from 6,350 megawatts at the end of 2024. The top markets include Northern Virginia, Atlanta, Dallas-Fort Worth, Chicago, Phoenix, Silicon Valley, New York Tri-State, and Hillsboro, Oregon.

Demand Continues to Outpace Supply

The slowdown comes as vacancy rates hover at a historic low of 1.4% in these markets. The rapid adoption of artificial intelligence and increased computing needs are fueling demand for data center space, intensifying the supply-demand imbalance. Limited available space is prompting more preleasing and off-market transactions as occupiers rush to secure capacity before delivery, a trend already evident in fast-growing hubs like Atlanta, which led the nation in data center absorption last year.

Cost Pressures and Construction Headwinds

Several obstacles are hindering new data center developments, including permitting delays, zoning challenges, and difficulties securing power. Rising costs for construction, land, labor, and equipment are further compounding the problem. CBRE reports that pricing for 3 to 10 MW deals jumped 12.5% year-over-year, and expects rent growth to exceed inflation for the next several years.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Shift Toward Secondary and Frontier Markets

A growing share of data center construction is moving toward smaller, frontier markets outside the main hubs. A recent JLL study found that 64% of ongoing US data center capacity is now in these emerging locations. Meanwhile, broader development activity appears to be plateauing, with studies predicting a gradual decline in new project spending after a peak in 2026, largely due to upfront capital challenges and lender caution in the absence of committed tenants.