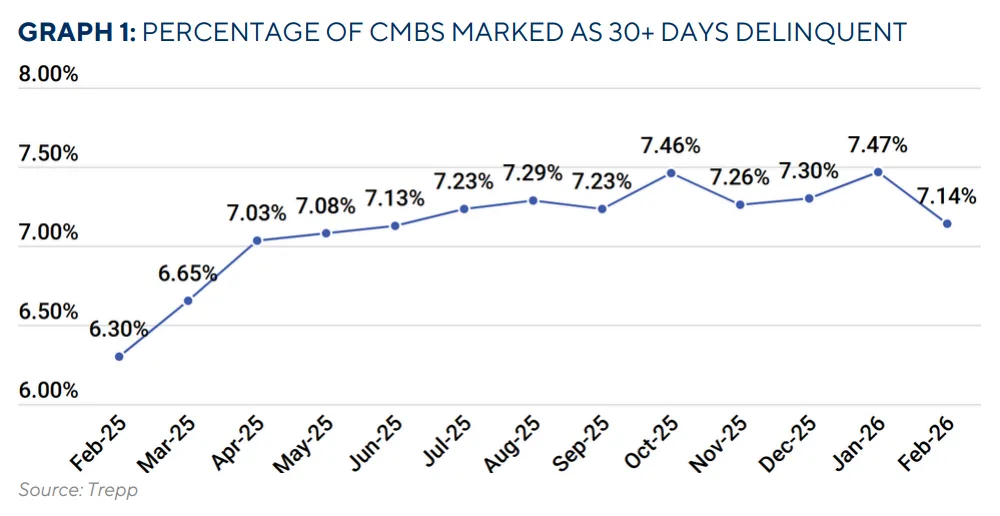

- CMBS delinquency rate declined to 7.14% in February, down 33 basis points from January.

- Large extensions of office and retail loans drove most of the month’s improvement.

- Office and retail sectors saw significant delinquency rate decreases, led by office falling to 11.2%.

- Year-over-year, overall CMBS delinquencies increased by 84 basis points.

Delinquency Rates Show Improvement

The overall CMBS delinquency rate decreased in February, dropping to 7.14%, according to Trepp. This 33-basis-point decline was largely driven by extensions and modifications on several large office and retail loans, which helped offset challenges from maturing debt.

Without the inclusion of loans performing past maturity (known as performing matured balloons), the delinquency rate stands at 7.14%. If these loans were included, the rate would be 8.75%. The percentage of seriously delinquent loans—those 60+ days late, in foreclosure, REO, or non-performing matured status—fell 20 basis points to 6.89% in February.

Sectors Driving the Change

Office and retail loans accounted for most of the improvement. Modifications or extensions on five large office loans and four mall loans accounted for a notable reduction in delinquency balances. Office delinquencies declined 114 basis points to 11.20%, retreating from the previous month’s record high of 12.34%. Retail rates fell 74 basis points to 6.30%, the lowest level since August 2024.

Multifamily rates dropped slightly by nine basis points to 6.85%. Lodging saw an increase, rising to 5.94%. Industrial ticked up marginally to 0.67%. Recent reporting has also shown that distress tied to office and multifamily loans has pushed CMBS delinquencies higher in recent months, underscoring how sector-specific weakness continues to shape loan performance.

CMBS 2.0+ Trends

For post-2008 issuance (CMBS 2.0+), delinquencies mirrored the broader trend. The rate declined 33 basis points to 7.05%, with serious delinquencies at 6.8%. By sector, office delinquency rates for CMBS 2.0+ dropped 115 basis points to 11.08%, while retail improved post-modification, decreasing to 5.99%.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Why It Matters

CMBS delinquency rates act as a key barometer for stress across commercial real estate markets. Loan performance often moves closely with broader market sentiment. February’s improvement offered some relief for lenders and investors. However, the decline largely reflects heavy workout activity, especially loan extensions in office and retail.

Even so, overall delinquency levels remain higher than last year’s levels. Meanwhile, lodging and industrial delinquency rates rose slightly, signaling ongoing pressure in certain property sectors.