- Lending to rent-stabilized multifamily properties in New York dropped 74% after major bank exits since 2019.

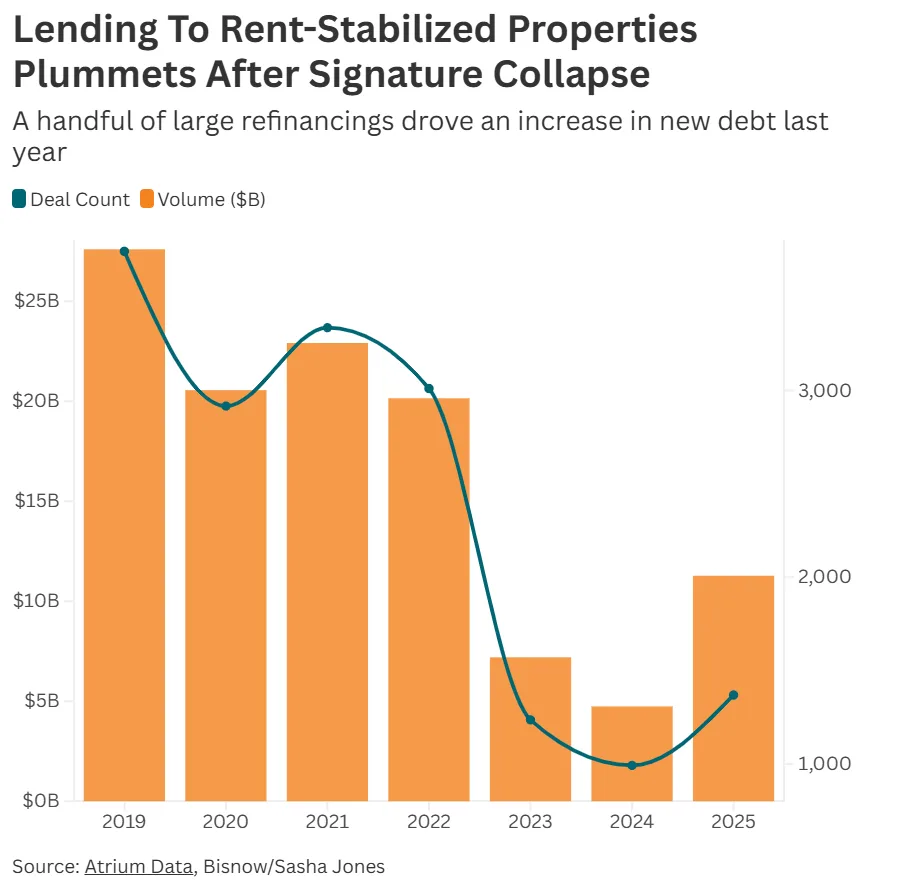

- Flagstar Bank (formerly NYCB) reduced originations from $3.9B in 2019 to just $58M in 2025.

- Delinquency rates for pre-1974 rent-stabilized loans hit 11.5%, up from 3.7% two years prior.

- Big banks’ market share has grown, but absolute lending volumes remain sharply lower than pre-crisis levels.

Major Lenders Retreat

Multifamily lending for New York’s rent-stabilized apartments has dropped dramatically in recent years. Bisnow reports that once-dominant players such as Flagstar Bank (formerly New York Community Bancorp) have sharply reduced their exposure, issuing just $58M in new loans in 2025 compared to $3.9B annually previously, according to Atrium Data. The 2023 collapse of Signature Bank further deepened the credit gap, forcing property owners to seek scarce and costly refinancing options.

Finance Volume Plunges

Combined, lenders provided $27.6B in multifamily mortgages secured by rent-stabilized buildings in 2019. Last year, that figure shrank to under $11.3B across approximately 1,400 loans. Market disruptions and changing regulations—including the 2019 Housing Stability and Tenant Protection Act—led to a 74% drop in rent-stabilized lending volume over six years. Asset values have fallen 40% since 2019, while the average rent-stabilized loan now exceeds five years in age.

Distress and Delinquencies Rise

Delinquencies for securitized loans tied to rent-stabilized properties built before 1974 surged to 11.5% by late 2025, up from 3.7% in 2023. In contrast, NYC market-rate property loan delinquencies remain below 0.6%. The number of stabilized residential units with outstanding debt now approaches 665,000. Difficulty accessing capital is acute for landlords carrying violations or operating overleveraged properties. The financing strain reflects a broader slowdown in commercial real estate activity, with property transactions across sectors falling to their lowest levels in more than a decade.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Banks and Alternatives Step In

While big banks, led by JPMorgan Chase and Wells Fargo, have increased their market share in rent-stabilized multifamily lending—from 20% in 2019 to 41% in 2025—the overall volume remains down. Giant deals like Wells Fargo’s $3.15B refinancing for Blackstone’s Stuyvesant Town and Peter Cooper Village skew recent totals. Alternative lenders, including REITs, insurers, and debt funds, have reduced their activity in the space, funding $4.8B in 2025, down from $8.7B in 2019. Despite distress, select private equity and institutional players are eyeing opportunities through distressed debt acquisitions and foreclosures.