America’s Rental Market at the Start of 2024

Here are this year’s most competitive rental markets according to RentCafe.

Jordan B. & Han-Gwon Lung

February 28, 2024

Together with

Good morning. Miami leads the nation as the hottest U.S. rental market, while the Midwest emerges as a major contender. Meanwhile, Macy’s plans to close 150 stores over the next 3 years and focus on its luxury brands to stay relevant as a retailer in 2024 and beyond.

Today’s issue is brought to you by Greysteel Advisory.

Market Snapshot

|

|

||||

|

|

*Data as of 2/27/2024 market close.

RENTAL MARKET

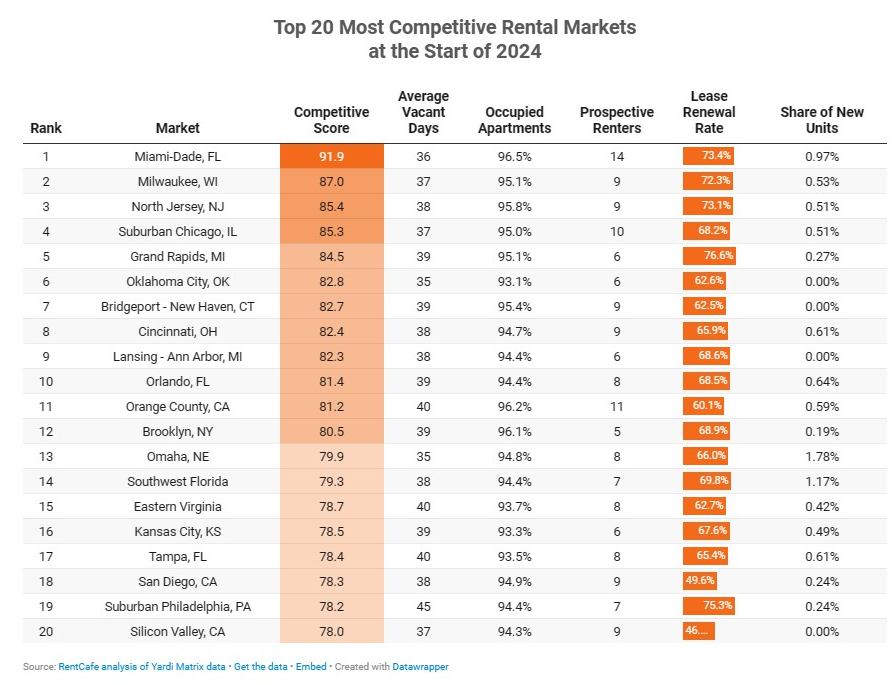

Miami Tops US Rental Market to Start 2024; Midwest Continues to Make Moves

At the start of 2024, Miami held strong as the top rental destination, with the Midwest continuing to rise as a major contender. RentCafe’s recent analysis uncovers key trends, showcasing the shifting competitive rental landscape.

Source: RentCafe analysis of Yardi Matrix data

Rental landscape: The national Rental Competitiveness Index (RCI) stands at 73.4, reflecting a moderately competitive market. Despite an increase in vacancy duration to 41 days on average, Miami kicks off the year as the leader in rental market competitiveness, driven by its robust economy and lifestyle appeal. The Midwest, shedding its “Rust Belt” image, is seeing a resurgence thanks to its affordability and booming tech and manufacturing sectors, particularly in Milwaukee, which ranks as the nation’s second-hottest renting spot.

Source: RentCafe analysis of Yardi data

Miami reigns supreme: Miami leads the nation as the hottest rental market at the beginning of 2024, scoring 91.9 on the Rental Competitiveness Index. The city’s vibrant economy continues to attract professionals, resulting in 14 renters competing for each vacant apartment. With just 3.5% of units available, Miami enjoys high demand and swift occupancy within 36 days.

Midwestern momentum: The Midwest region has emerged as the most competitive for renting in 2024, securing seven spots among the nation’s top 20 hottest rental markets. The shift is driven by affordability and economic growth. In cities like Milwaukee, there’s high demand for rental assets, pushing occupancy rates to 95.1%. Lease renewal rates are at 72.3%, with nine applicants vying for each available unit. This trend signifies the region’s appeal for renters aiming to save for homeownership goals.

College town hotspots: Fayetteville, AR, leads as the hottest small rental market, with its appeal significantly bolstered by the University of Arkansas’s record-breaking enrollment. The city exemplifies the intense competition found in smaller markets, where demand from students and faculty, coupled with limited supply, creates a competitive renting environment. Other notable mentions include Lafayette, IN, and Lehigh Valley, PA, which face similar challenges and opportunities.

➥ THE TAKEAWAY

Looking ahead: Apartment rents are at their lowest since March 2022, with a notable supply increase leading to a national median rent decrease for one and two-bedroom units. Despite the overall market loosening, certain areas, especially Miami and Milwaukee, face heightened competition. This is further exacerbated in college towns and regions with booming economies, where the supply of new rentals is not keeping up with demand, leading to heightened competition and occupancy rates.

SPONSORED BY GREYSTEEL

Transformative Tax Strategies

With 45L and 179D energy efficiency tax incentives as high as $5,000 per unit and $5.00 per square foot, our clients average more than $150,000 in tax benefits. These tax incentives are available not only for real estate investors, but also for commercial developers, single family home developers, manufactured home developers, REITs, and architects.

Greysteel Advisory’s expert team of tax professionals, attorneys, and engineers make the process of harnessing 45L and 179D energy efficiency tax incentives simple, fast, and profitable.

As deal flow has slowed and the industry is in a holding pattern waiting for interest rates to drop, now is the moment to capitalize on this opportunity.

Please support our sponsors. It helps keep CRE Daily free.

✍️ Editor’s Picks

-

Still manageable: JPMorgan’s head honcho Jamie Dimon expects CRE issues to remain minimal if the U.S. avoids recession, citing manageable stress levels.

-

7-Day Multifamily: Underwriting multifamily properties is different than SFH. Learn the nuances of underwriting for multifamily deals so you never overpay. (sponsored)

-

Loan woes: CRE loans continue to cause concern among banks. CLO distress rates have quadrupled and many banks are overexposed with vacancy tight at 4.3%.

-

Cap rates chat: The latest NNN market analysis by Chris Lomuto at Northmarq reveals that average closing cap rates are lower, with potential valuation growth on the horizon.

-

Cost-cutting strats: Developers and construction companies in NYC are tackling high costs creatively by exploring prefab, smart materials, and shifting expenses to tenants.

-

Bouncing back: JLL’s (JLL) 2023 revenues reached $20.7B with a 4% increase in 4Q23, although consolidated fee revenue fell by 11%.

🏘️ MULTIFAMILY

-

Rent regulation victory: Blackstone (BX) has thrown in the towel, keeping 6.2K units rent-stabilized at Stuy Town-Peter Cooper Village amidst an ongoing legal battle.

-

House, lease, hope: A new LA pilot program is leasing buildings to house the homeless, seeking a citywide expansion and aiming for 1.7K units by year-end.

-

Condo crunch: Rising HOA fees and insurance premiums make Florida condo ownership less attractive. Jacksonville condo prices are down 7%, while Miami is down 3%.

🏭 Industrial

-

Building boom: The industrial property boom, driven by e-commerce leases and low rates, has hit historic levels, not saturating all markets.

-

Data center delight: Prime Data Centers plans a $1.3B turnkey data center campus on 206 acres in rural Caldwell County, TX.

-

Industrial insights: In 2023, CA’s Inland Empire witnessed strong industrial activity with 19.4MSF under construction and $52.1B in transactions.

🏬 RETAIL

-

Grocery wars: The FTC blocks Kroger’s (KR) $24.6B acquisition of Albertsons (ACI), citing anti-competitive concerns.

-

Blooming brands: Bloomin’ Brands (BLMN), the parent company of Outback Steakhouse, is closing 41 older restaurants but opening the same amount, aiming for increased profitability.

-

Luxury buying: Luxury brands like Prada and Gucci are buying up prime retail real estate in NYC, challenging traditional leasing norms.

-

Smart growth: Crombie REIT (CROMF) shifts its focus to compact developments for 2024, aiming for solid returns with short completion times.

🏢 OFFICE

-

Pension pivot: Canadian pension funds and global real estate pioneers are selling holdings, including an NYC project for just $1, amid ongoing office market concerns.

-

Midtown moves: Barings (BBDC) buys a 330KSF Midtown office building for $160M, 85% leased, from Principal Real Estate Investors.

-

Lost lease: Bankrupt WeWork exits a 92KSF location at the LA Gas Company Tower due to a failed negotiation. The office tower, worth $632M in 2021, is now valued at just $270M.

RETAIL RESET

Macy’s to Close 150 Stores, Focus on Luxury Brands

Wikimedia Commons/Caldorwards4

Macy’s (M) has unveiled a new strategy to close 150 stores across the nation over the next three years in a bid to revitalize its flagging retail business.

Quick overview: The first phase of 50 store closures is set to be completed by the end of the fiscal year, with the remaining 100 closures expected by the end of 2026. Notably, Macy’s plans to monetize $600M–$750M worth of assets by 2026, potentially involving property sales.

Strategic closures: Macy’s decision to shutter 150 stores signifies a significant shift for the legendary retailer, accounting for 25% of its square footage while contributing only 10% of sales. By reducing store count to about 350 post-closures, Macy’s is positioning itself for greater efficiency and profitability.

Luxury in focus: In a strategic pivot, Macy’s is directing its attention to its luxury brands, Bloomingdale’s and Bluemercury, with plans to open 15 new Bloomingdale’s locations and 30 more Bluemercury stores within the next three years. On top of that, 30 existing Bluemercury stores are slated for remodeling.

➥ THE TAKEAWAY

Financial outlook: Despite slumping sales and financial challenges, Macy’s remains attractive due to its valuable real assets. With analysts highlighting the potential value of Macy’s real estate holdings, the retailer’s move towards revitalizing its business model and optimizing its portfolio underscores a forward-looking approach to weathering industry headwinds and driving future success.

📈 CHART OF THE DAY

Many commercial mortgages initially set to mature in 2023 have been rescheduled to expire between 2024 and 2028, leading to an increase in commercial mortgage debt maturities from $659B at EOY 2022 to $929B by EOY 2023.

This shift in maturities also exhibits significant variation across different investors and property types.

A mere 3% ($28B) of the multifamily and healthcare mortgages held or guaranteed by agencies such as Fannie Mae, Freddie Mac, FHA, and Ginnie Mae are set to mature in 2024. Life insurance companies will witness 8% ($59B) of their outstanding mortgage balances maturing in the same year. Depository institutions face a 25% ($441B) maturity rate, while the figures are even higher for CMBS, CLOs, or other ABS at 31% ($234B). A substantial 36% ($168B) of mortgages held by credit companies and other lenders will also mature in 2024.

SHARE CRE DAILY & EARN REWARDS

You currently have 0 referrals, only 1 away from receiving B.O.T.N Multifamily Deal Screener .

What did you think of today’s newsletter? |