- The 1Q24 Fear and Greed Index holds steady at 52 out of 100, although optimism has fallen slightly since last quarter.

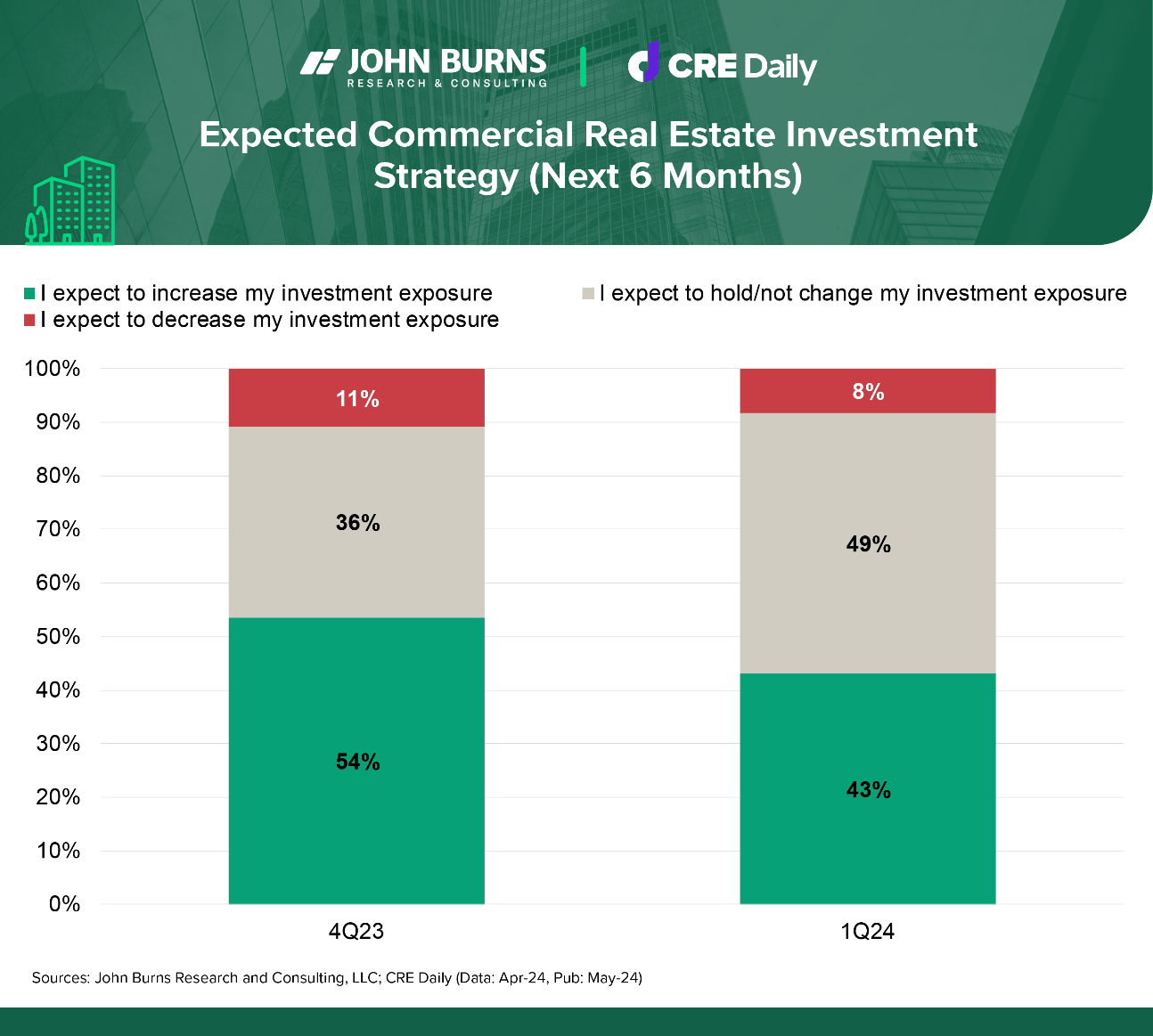

- Respondents who plan to increase their CRE exposure over the next 6 months fell from 54% to 43%.

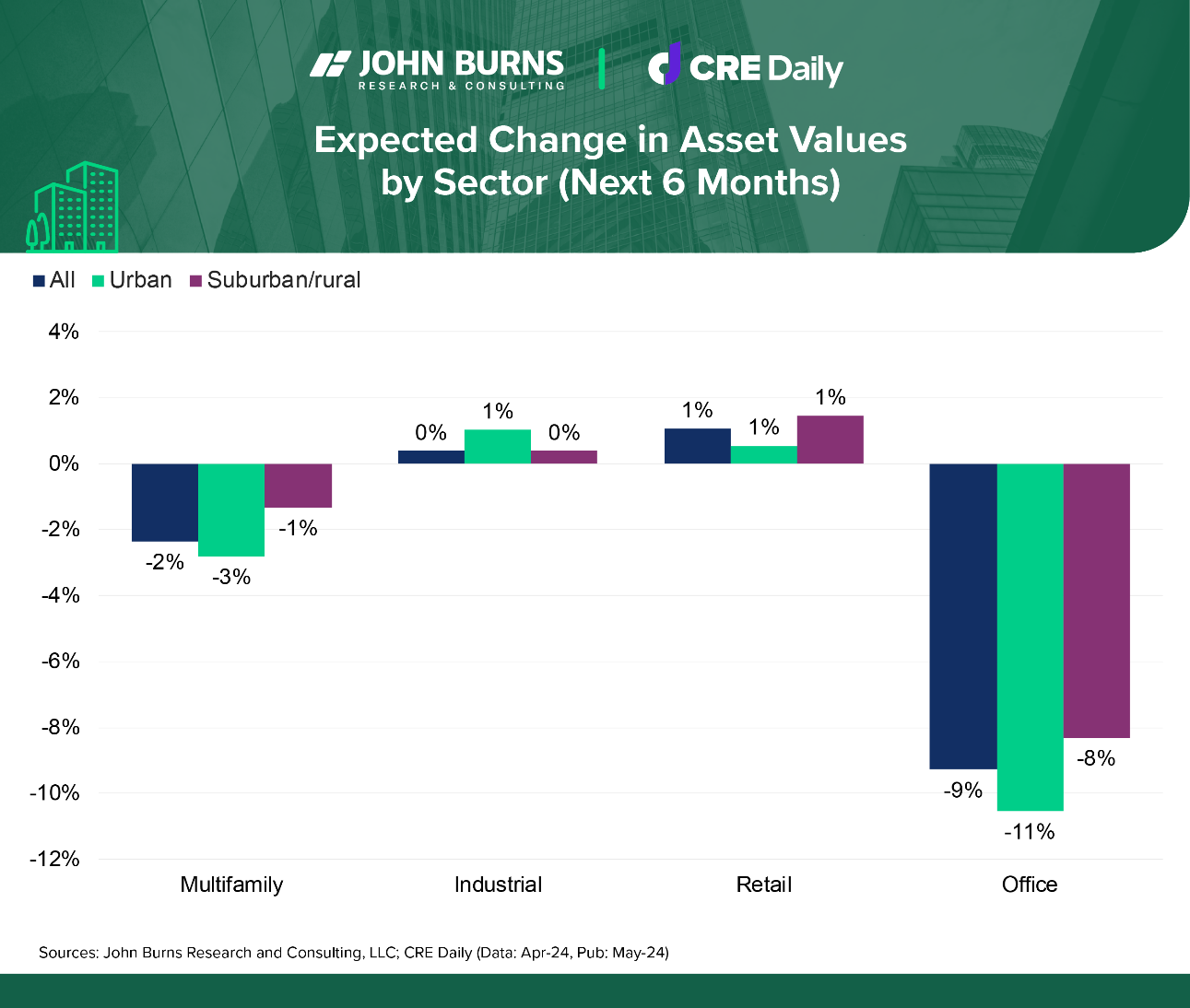

- Industrial and retail properties were resilient and will see higher allocations, while office and multifamily face challenges.

- Overall, urban asset values are expected to drop more than suburban ones across property types.

The Burns + CRE Daily Fear and greed index, created in collaboration with CRE Daily, reflects sentiment across various cre sectors, including multifamily, industrial, retail, and office. This survey provides a lot of insight into whether values and development will likely increase or decrease, and is one of the factors we consider when forecasting multifamily construction.

1400+ commercial real estate (CRE) investors became even less optimistic this quarter, largely because optimism over declining rates has waned. The 1Q24 survey findings are available for download below.

Holding Steady Amid Uncertainty

The 1Q24 index remained stable at 52 out of 100, indicating a balanced market. Sector-specific values ranged from 42 (office) to 56 (industrial).

- Holding pattern: 68% of surveyed investors are currently maintaining their current cre exposure, up from 66% in 4Q23 and 49% in 3Q23.

- Up and down: Only 20% of respondents increased their CRE exposure last quarter, while 12% decreased their exposure. Over the next six months, 43% plan to increase their CRE exposure, down from 54% last quarter.

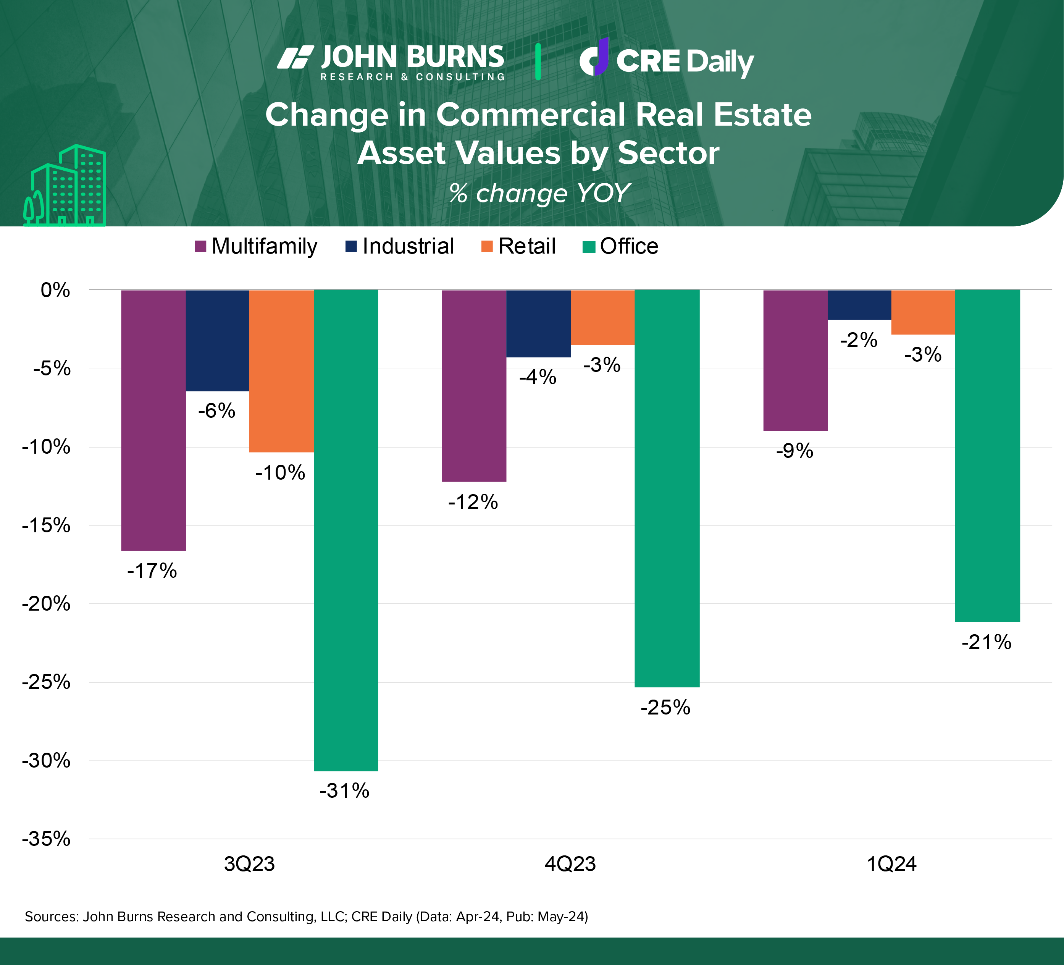

- Lower values: Investors are seeing declining asset values across all major property types, though decreases are less severe compared to past quarters. In Q1, YoY asset values fell by -9% for multifamily, -2% for industrial, -3% for retail, and a steep -21% for office.

Multifamily, Office Challenges

- Mixed multifamily: Overbuilding and high defaults plagued Class A and C properties. Class B saw better occupancy rates but insufficient demand for rent growth. Dwindling downtown demand also lowered the premium for urban multifamily, expected to slip in value by 3%.

- Office owner onus: Many loans for owner-occupied commercial properties were fixed between 2019 and 2022, leading to potential financial strain as these loans mature. Elevated vacancy rates in central business districts also make urban office properties particularly vulnerable.

- Reducing exposure: Over the next 6 months, respondents plan on shedding 9% of their office holdings (-11% urban, -8% suburban/rural offices). They also plan on cutting 2% of multifamily assets (-3% urban, -1% suburban/rural multifamily).

Retail, Industrial Bright Spots

- Retail resilience: Limited supply, especially in prime locations, is expected to drive growth over the next few years. Retail investors anticipate stable or growing asset values by year-end 2024.

- Industrial strength: Strong tenant demand due to onshoring and population growth supports stable or growing industrial asset values. Investors highlight ongoing demand for industrial spaces ranging from 30 KSF to 150 KSF.

- Increasing exposure: Over the next 6 months, respondents plan on adding to their industrial assets (+1% urban) and increasing retail property exposure by 1% across the board.

High Costs, Hawkish Fed

- Waiting with bated breath: Regional lenders remain on the sidelines, with little change expected in 2024. Meanwhile, high capital costs and expenses are affecting all CRE sectors. Investors remain cautious, awaiting bigger rate cuts that seem increasingly unlikely.

- Capital on the sidelines: As long as the timing of future rate cuts remains uncertain, capital will stay on the sidelines. One anticipated rate cut this year is seen as insufficient to entice patient capital or begin larger interest rate and cap rate compression.

Why It Matters

The latest insights from the 1Q24 Burns + CRE Daily Fear and Greed Index offer a nuanced view of market sentiment. Most investors are hitting ‘Pause’ before increasing or decreasing CRE exposure over the next 6 months.

The expectation of high capital costs and the slow interest rate adjustments are keeping capital on the sidelines. While there are opportunities in certain sectors, like retail and industrial, the broader cre market is waiting with bated breath to see what the Fed will do.