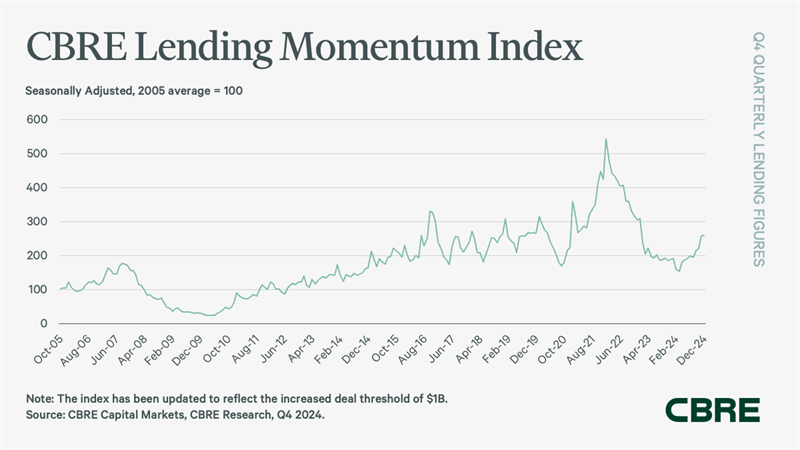

- The CBRE Lending Momentum Index jumped 37% YoY and 21% from Q3, indicating a strong recovery in commercial real estate lending.

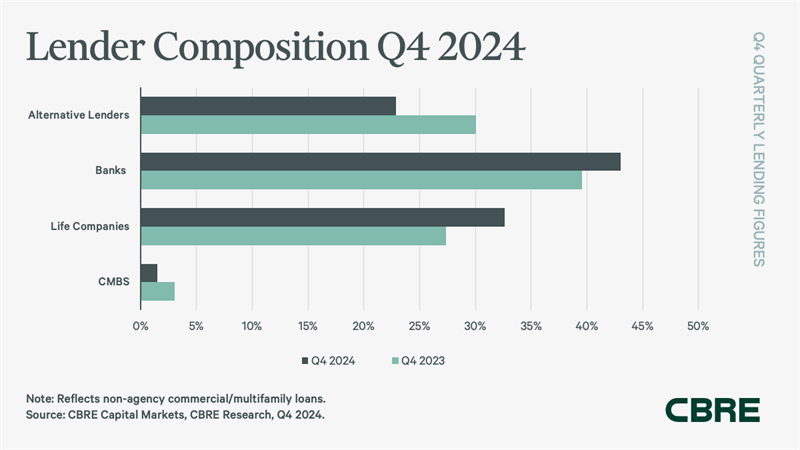

- Banks accounted for 43% of non-agency loans, increasing their market share from 18% in Q3 due to balance sheet cleanup and improved regulatory conditions.

- Spreads on closed commercial mortgage loans fell by 49 bps YoY, while multifamily loan spreads tightened to their lowest level since early 2022.

- Multifamily agency loan originations rose 87% in Q4, reaching $53B, as agency mortgage rates dropped to 5.4%, their lowest level since mid-2023.

The commercial real estate lending market saw significant growth in Q4, as capital reallocation and improving fundamentals fueled a spike in loan originations, according to CBRE.

Despite some deal deferrals due to shifting Treasury yields, a strong capital base and steady investor interest supported competitive lending across banks, life insurance companies, and debt funds.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Zooming Out

The cbre lending Momentum Index closed the quarter at 259, far exceeding the pre-pandemic five-year average of 229. According to James Millon, US President of Debt & Structured Finance at CBRE, lenders should remain active in 2025 as maturing debt fuels refinancing and investment sales.

He noted lenders will likely leverage loan sales to create liquidity for strategic assets and asset management-intensive properties nearing maturity extensions.

cbre lending momentum index“/>

cbre lending momentum index“/>Banks Take The Lead

Banks emerged as the most active non-agency lenders, increasing their share of loan closings to 43% in Q4, up from 18% in Q3. This sharp rise was driven by payoffs, an improving regulatory landscape, and efforts to strengthen balance sheets.

Life insurance companies followed, accounting for 33% of loan originations, while debt funds and mortgage REITs captured 23%—a drop from 2023 but still up 72% in origination volume. The CMBS conduit sector, meanwhile, continued to shrink, making up just 1.5% of originations, down 3% YoY.

Multifamily Moves

Multifamily lending experienced a major boost, with government-backed agency loan originations reaching $53B in Q4, up 87% from Q3. For the full year, volume rose 19% to $120B, driven by declining interest rates and sustained demand for multifamily housing.

CBRE’s Agency Pricing Index, which tracks average fixed agency mortgage rates for 7-to-10-year permanent loans, fell to 5.4% in Q4, its lowest level since mid-2023.

Favorable Lending Conditions

Lenders continued to offer competitive terms, with the average spread on closed commercial mortgage loans tightening to 184 bps, a 49-bps YoY decline. Multifamily loan spreads narrowed even more, down to 156 bps, the tightest level since early 2022.

Underwritten cap rates fell to 5.9%, while debt yields dropped to 9.4%. The average Loan-to-Value (LTV) ratio rose to 64.1%, up from 62.8% in Q3, showing greater confidence among borrowers.

The Bottom Line

With a wave of maturing debt approaching in 2025, lending activity is expected to stay strong. Banks, life insurers, and debt funds will likely maintain their momentum, while agency-backed multifamily lending should continue benefiting from lower borrowing costs and resilient fundamentals.

The market is also expected to see more refinancing activity as investors reposition capital and lenders explore strategic loan sales to manage liquidity and risk.