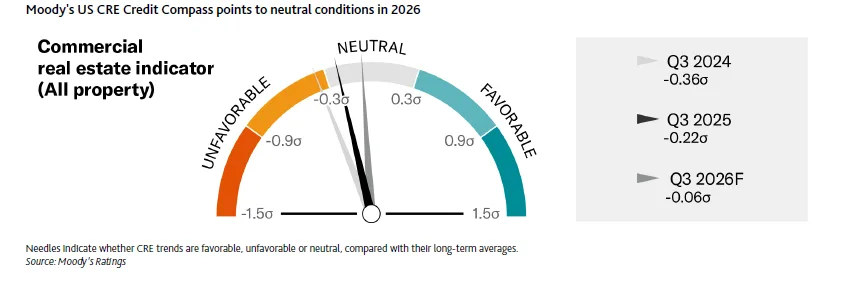

- Moody’s expects neutral US CRE credit conditions in 2026, with mild economic growth and lower short-term rates helping the market stabilize.

- Rising leverage will increase risk in large and single-asset CMBS and CRE CLO deals unless credit protections improve.

- Office and data centers will keep driving SASB issuance, though weak office demand may push conduit delinquencies higher.

Outlook Overview

According to the Commercial Property Executive, Moody’s 2026 outlook for US commercial real estate (CRE) finance shows a mixed picture. Lower short-term interest rates and slow but steady growth will support refinancing. However, rising leverage and continued stress in some property types, especially office, still pose major risks.

The outlook expects improvements in securitization performance, but warns that weak-performing properties will still face high default risk.

Property Fundamentals Show Slight Gains

Moody’s predicts 1.8% US GDP growth in 2026. Lower short-term and steady long-term interest rates will ease borrowing costs and help support real estate values.

Still, the forecast includes job losses in the coming months, which will reduce demand for space. As a result, property fundamentals may improve slightly by Q3 2026, but will remain neutral overall.

New Deal Volume Will Shift Toward Data Centers and Offices

Lower interest rates will encourage more borrowing, and Moody’s expects new deals to carry more leverage.

SASB (single-asset, single-borrower) issuance will likely stay mostly floating rate as borrowers wait for more rate cuts. Office properties led the SASB market in 2025 with $25.7B in new deals—$17.2B of that came from Manhattan alone.

Data centers are growing fast in this space too. In 2025, SASB issuance for data centers hit $10.7B, more than triple the $3B seen in 2024. Moody’s expects this trend to continue, although some investors may hold back due to limits on property and tenant concentration.

CRE CLOs are also poised for growth in 2026. Lower rates will allow borrowers with past refinancing delays to return to the market, especially through private lenders.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Existing Deals Face Ongoing Pressure

Conduit loan refinancing should increase in 2026 but stay below normal levels. Office loans, in particular, will continue to struggle due to high vacancies and expiring leases.

Office delinquencies rose by 150 basis points over the past year and now sit at nearly 18%. Moody’s identifies Chicago, Los Angeles, and Washington, D.C. as cities where demand won’t recover enough to reduce vacancy. These markets are already dealing with worsening office dynamics, which could continue into 2025 and beyond, making refinancing even harder.

Retail may also see rising stress. A slowdown in consumer spending could lower mall cash flows, especially for marginal properties. Weak mall loans have been part of recent conduit deals, and Moody’s warns they may default if sales drop.

Why This Matters

Even with some market improvements, the road ahead looks uneven. Borrowers in stronger markets and property types will benefit from lower rates, while others will face challenges refinancing or avoiding losses.

Investors and lenders will need to stay cautious—especially in sectors like office and retail—where weak fundamentals still dominate.

Looking Ahead

Refinancing activity should pick up in 2026 as rates ease, giving some borrowers a second chance. Data centers and offices will continue to shape the securitization market, but deal structures will need stronger protections.

While the market may not fully recover, the coming year offers a clearer path forward for both lenders and investors who stay selective and informed.