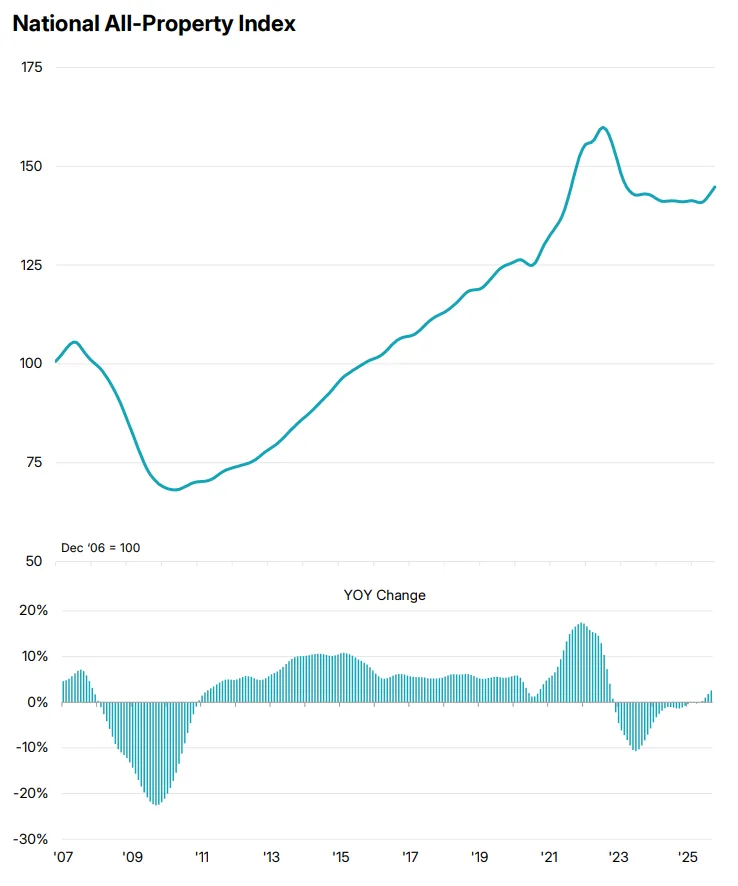

- US commercial property prices rose 2.6% year-over-year and 0.7% month-over-month in September, with five of six major sectors posting annual gains.

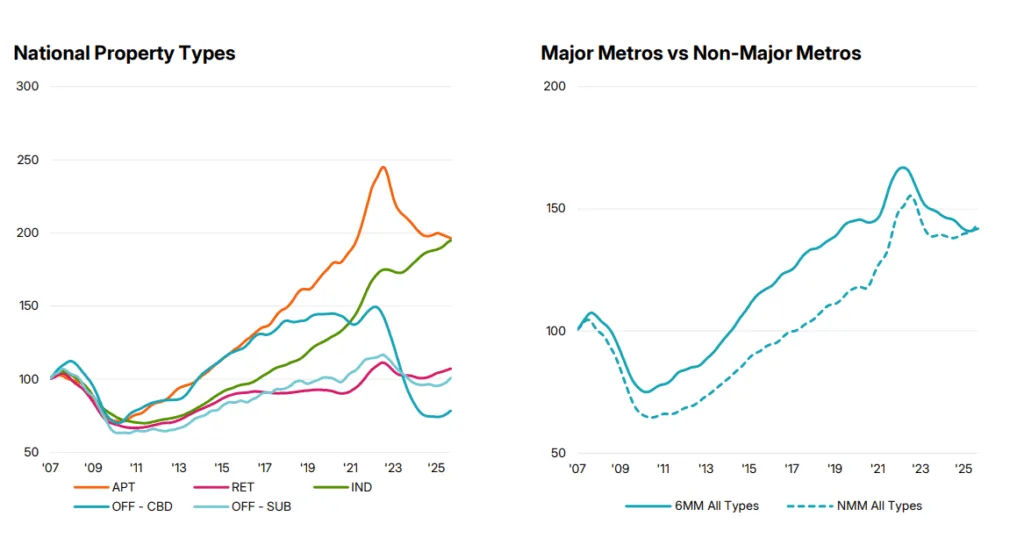

- Retail led all sectors with a 5.5% annual price increase, while apartments were the only category to decline, down 0.8% from a year earlier.

- Investor activity picked up for the sixth consecutive quarter, bolstered by expectations of further Fed rate cuts after the 25-basis-point drop in September.

- CBD office prices outpaced suburban office for the first time since early 2022, rising 5.1% year-over-year.

Market Rebounds, Led by Retail and Industrial

Commercial real estate prices showed solid momentum in Q3 2025, according to MSCI’s RCA CPPI report. The National All-Property Index rose 2.6% annually and 2.2% quarter-over-quarter, translating to an annualized pace of 9% — the strongest growth rate in over a year.

Retail stood out, posting a 5.5% annual increase — its 17th consecutive month of gains — while industrial prices rose 4.0% year-over-year and remain 14% above pre-rate-hike levels from early 2022. These gains suggest continued investor appetite for logistics and consumer-facing assets.

Apartment Sector Continues to Struggle

Apartments remain the laggard in commercial pricing. The sector posted a 0.8% year-over-year decline in September and fell at an annualized rate of 3.3% from Q2. Multifamily prices are now 20% below their July 2022 peak, reflecting sustained softness in the sector despite broader market improvement.

Office Sees Tentative Turnaround

Office prices showed unexpected strength, especially in central business districts. CBD office prices rose 5.1% YoY, outpacing suburban office (4.5%) for the first time since early 2022. On a shorter-term basis, both CBD and suburban offices posted even stronger momentum.

Despite this, CBD office prices are still 43% below their March 2022 levels, underscoring how far the sector remains from a full recovery.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Regional Divergence: Non-Major Metros Outperform

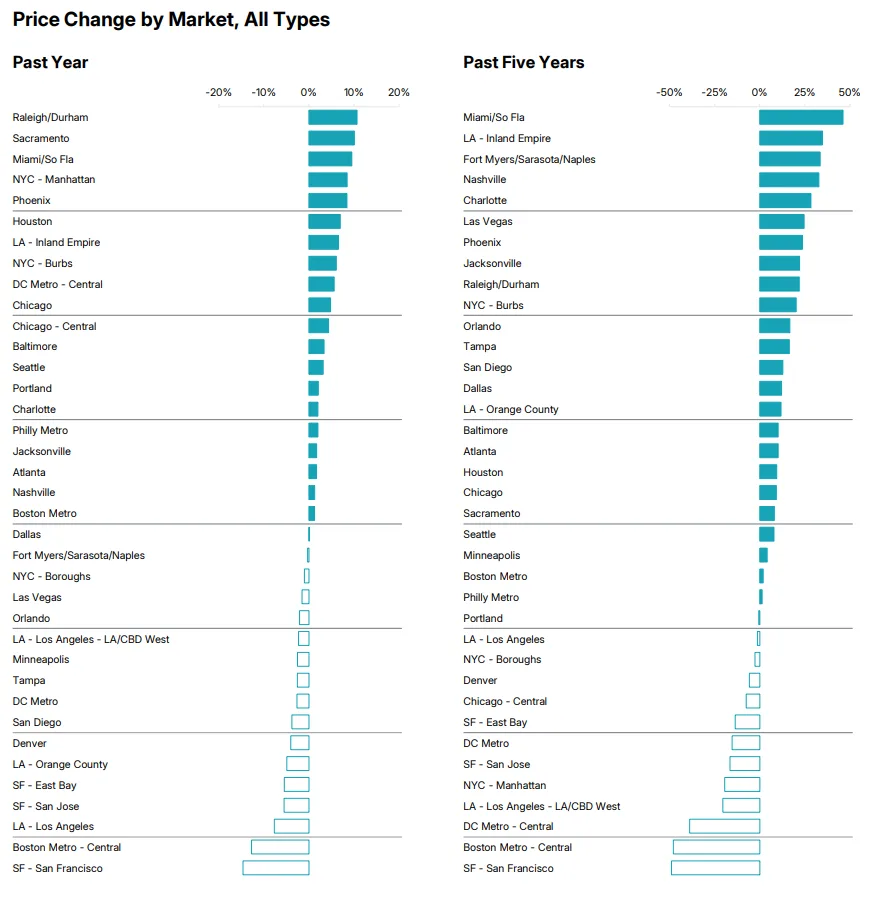

While major metros like New York and San Francisco continued to lag, secondary and tertiary markets fared better. Non-major metros posted a 4.0% annual gain, compared to a 1.8% decline in the six major metros. Over the past five years, non-major metros have outperformed significantly, driven by affordability and population migration trends.

Outlook: Investors Lean Into Rate-Cut Hopes

The Q3 report highlights a cautiously optimistic investment environment. Transaction volumes rose at a double-digit pace year-over-year, marking six consecutive quarters of growth. Expectations of additional Federal Reserve rate cuts in late 2025 are fueling buyer confidence.

While uncertainty remains, particularly in multifamily and urban office segments, price gains across most sectors and regions point to an inflection point — especially if rates continue to fall.

What’s Next?

The ongoing recovery in CRE pricing suggests we may be entering a new phase of the market cycle. Watch for more transactional momentum and pricing clarity in early 2026, especially as capital conditions ease and the Fed signals further direction.