- CRE Activity Index fell 13% in December, typical for year-end but far less than 2024’s sharp drop.

- Index closed December 49% higher than the prior year, reflecting enduring recovery.

- Large property deals ($100M+) rose 44% over November, signaling continued investor engagement.

- Lending conditions improved, with more refinancing and increased capital availability entering 2026.

Seasonal Pause, But Improved Momentum

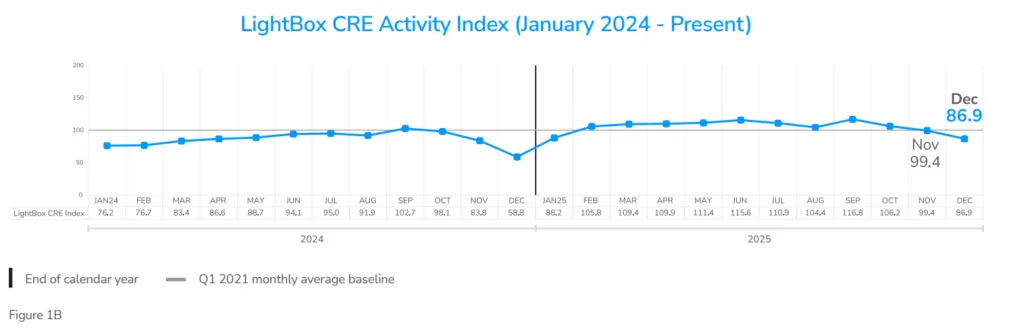

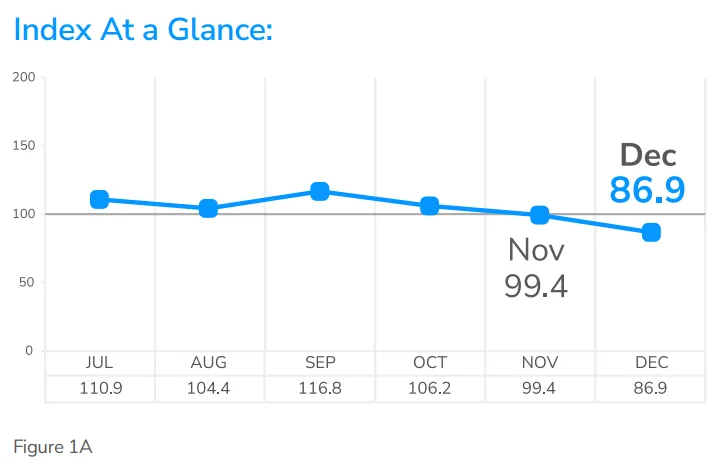

The LightBox CRE Activity Index marked a 13% decline in December 2025, settling at 86.9. This pullback was consistent with historical year-end slowdowns, but notably less severe than the 30% drop seen after the 2024 election. Key components—commercial listings, appraisals, and environmental due diligence activity—remained robust year-over-year despite the seasonal pause.

Compared to December 2024, listing volume ran 55% higher and Phase I ESA activity increased by 48%. Appraisals also saw a 41% year-over-year jump. These metrics point to greater seller and lender engagement and underline that the market is materially stronger entering 2026.

Why It Matters

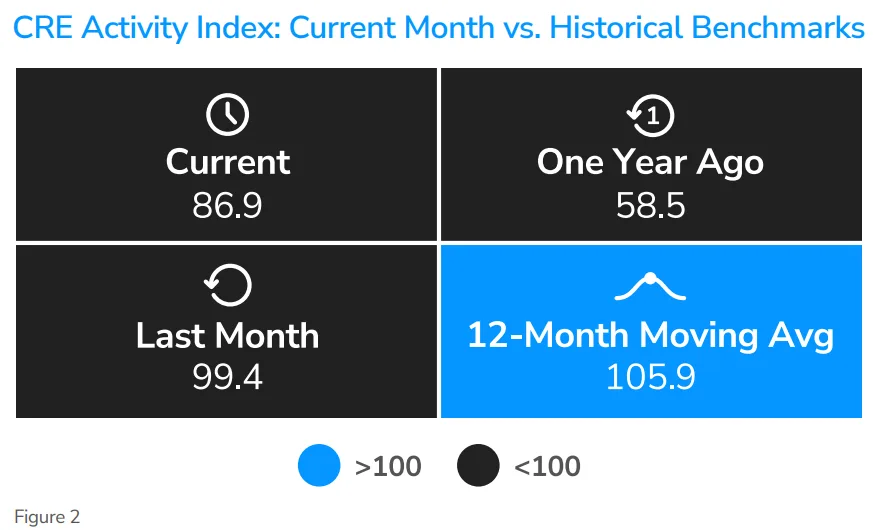

December’s decrease in the CRE Activity Index is attributed mostly to calendar effects, not underlying stress. Contrasting last year’s policy-driven pullback, this year’s dip reflects typical holiday seasonality. The Index’s year-end level, 49% above the previous December, signals the sector’s ongoing recovery.

This backdrop is supported by improved credit conditions. Banks reported solid Q4 footing, with JPMorgan Chase and others highlighting resilient balance sheets and a steady stream of refinancing activity. CMBS issuance stayed near multi-year highs and interest rate cuts in 2025 unlocked further capital, positioning the CRE market for incremental improvement.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Transaction and Lending Trends

Deal flow showed surprising strength. The volume of nine-figure CRE deals climbed 44% from November, reflecting lagged effects of September’s surge in listings. Investors pushed through major deals across asset classes, from multifamily portfolios to land for data centers. Office transactions rebounded as well—often at recalibrated pricing—helped by a willingness to close out deals before year-end.

Lenders maintained a disciplined, case-by-case approach, reassured by more stabilized pricing and aligned buyer–seller expectations. Both debt and equity capital were more available, especially for refinancing and select construction or conversion projects.

Broader Economic Signals

CRE activity remained strong, but broader macro data showed mixed signals. The US labor market slowed in December, adding just 50,000 jobs. That capped 2025 as one of the weakest hiring years outside of a recession. Ongoing tariff uncertainty, geopolitical risks, and a Fed leadership transition all contributed to investor caution. Policymaker divisions over the direction of rate cuts further added to market hesitancy, reinforcing expectations that interest rates will hold steady into early 2026. Still, most expect interest rates to hold steady into early 2026.

What’s Next

With election-driven uncertainty in the past and capital supply improving, the December 2025 CRE Index looks more like a typical seasonal pause. January usually brings a 40–50% rebound, making next month a key test for Q1 deal flow. The market enters 2026 in a stronger position, with modest, selective gains likely. Capital deployment is expected to continue as loan maturities and pricing resets bring more assets to market.