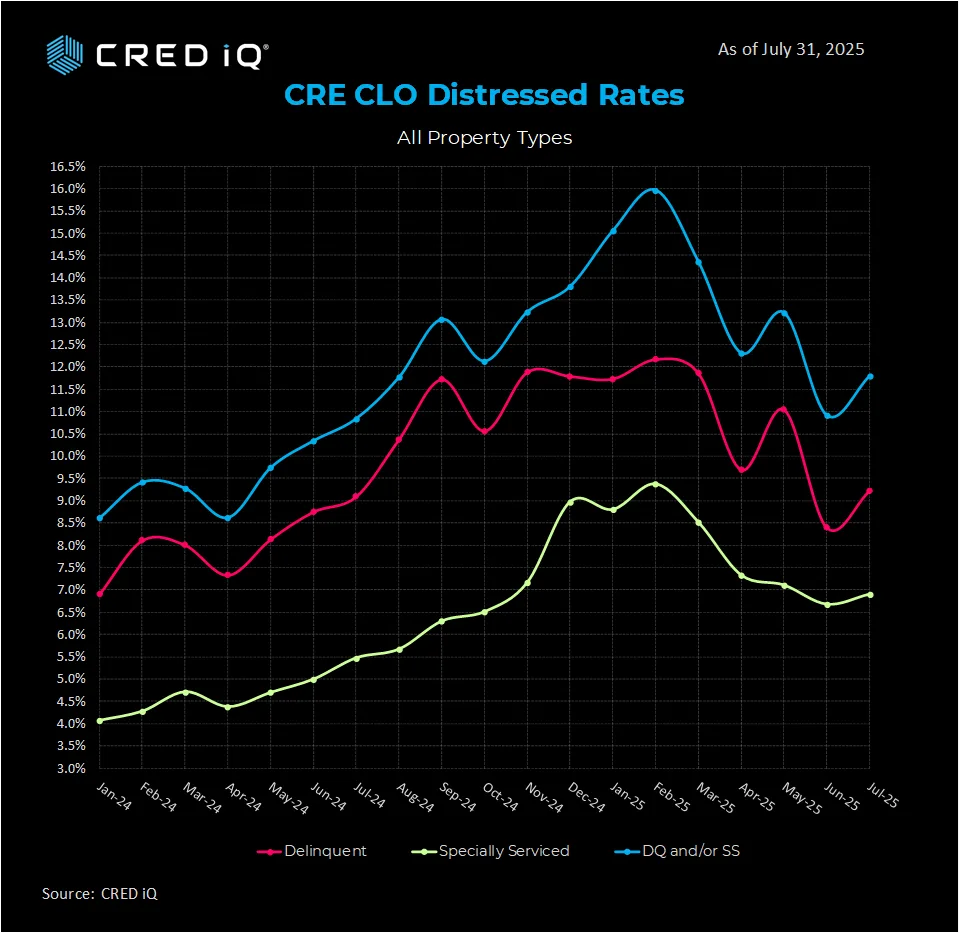

- The CRE CLO distress rate climbed 88 BPS in July to 11.8%, partly reversing June’s sharp 230 BPS drop.

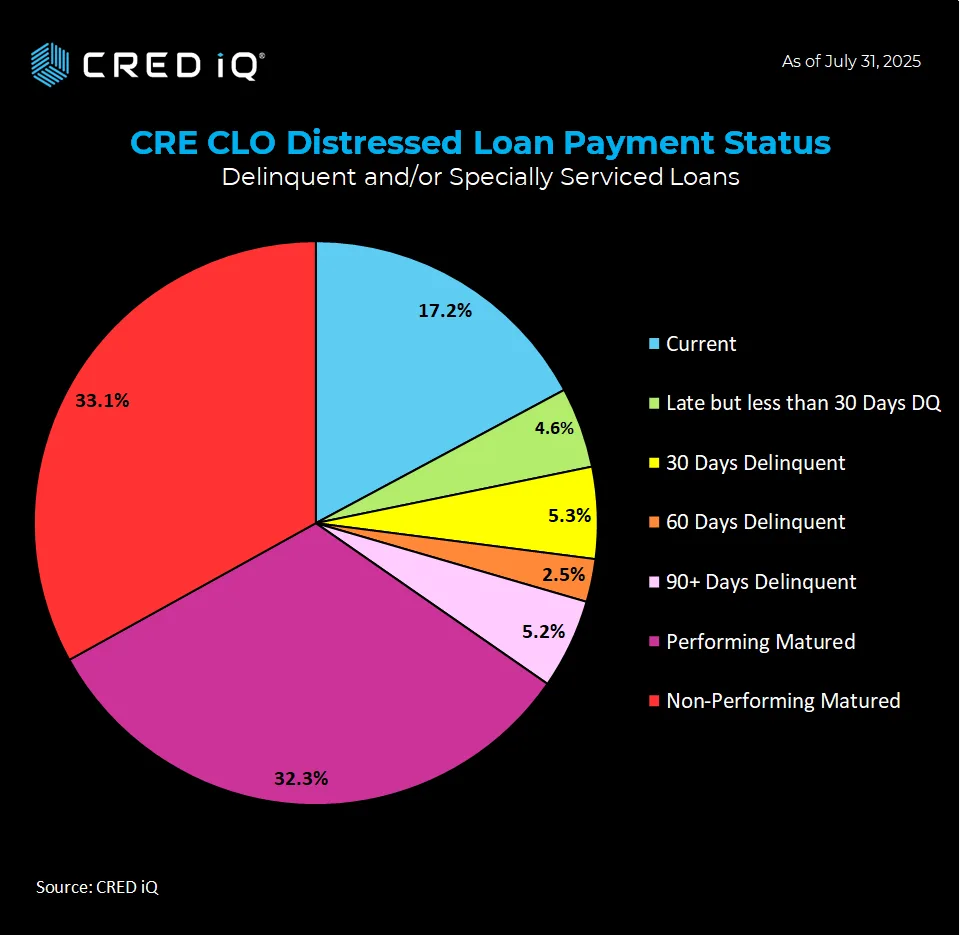

- Delinquency rose to 9.2%, special servicing ticked up to 6.9%, and more than 65% of loans are now past maturity.

- Pre-maturity delinquencies fell to 12.9%, hinting at some short-term stability despite maturity pressures.

The CRE CLO market saw fresh stress in July as more loans reached maturity. CRED iQ’s latest report shows the distress rate—which covers loans 30+ days late, past maturity, or in special servicing—rose to 11.8% from 10.9% in June. The 88-basis-point increase erased part of June’s 230-basis-point improvement. Overall, the trend has eased since peaking in March, but the month-to-month shifts remain choppy.

Loan Performance Shifts

Delinquency rates, a key measure of loan health, grew by 82 BPS to 9.2% in July. The special servicing rate also moved up, adding 23 BPS to reach 6.9%.

About $1.2B in CRE CLO loans remain current. This share dropped 377 BPS to 17.2% after a large gain the month before.

Maturities Dominate the Risk Profile

Loans past maturity now make up 65.3% of the CRE CLO pool. Of these, 32.3% are “performing matured,” up from 26.5%. Another 33.1% are “non-performing matured,” up from 32.8%. This shows many borrowers are paying despite maturity defaults, though a large share are not.

Bright Spot in Pre-Maturity Performance

Pre-maturity delinquencies fell by 478 BPS to 12.9%. This means fewer loans are late before their due dates, which could help support near-term performance.

Why It Matters

For lenders and investors, July’s data highlights the need to watch maturity risk closely. Tools like CRED iQ give market players detailed insights into loan health. These help them manage risk in a market where high refinancing hurdles and uneven performance keep volatility high.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes