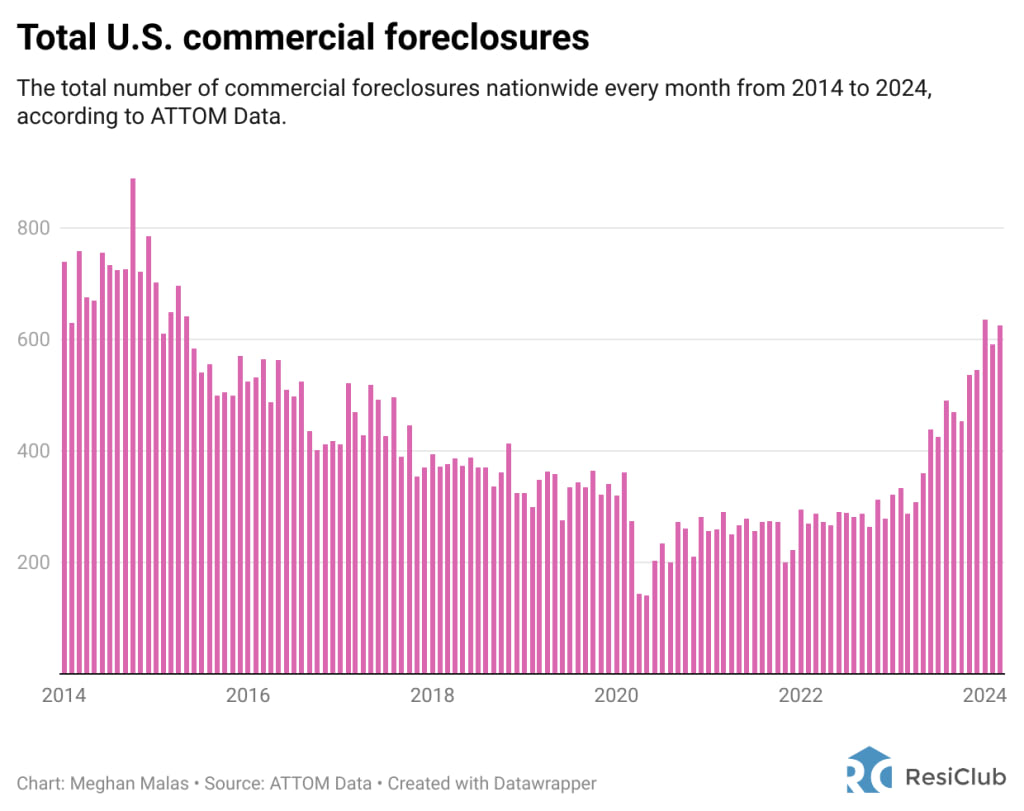

- Commercial property foreclosures rose a staggering 117% between March 2023 and 2024, reflecting mounting distress.

- March 2024 saw 625 commercial foreclosures, the highest number since March 2015 9 years ago.

- The top foreclosure states in Q1 included California, New York, and Florida, showcasing significant distress across major U.S. regions.

Blackstone (BX) believes that cre prices may be stabilizing amid rising vacancy rates. But concerns persist over the unknown impact of impending interest rate changes.

Prices Bottoming Out

Blackstone Group’s Jon Gray suggests that U.S. CRE is at a crucial juncture. While vacancy rates are rising, fundamentals are fortunately looking a bit better. However, the whole sector is still trying to figure out if we’ve actually hit rock bottom with CRE prices yet.

Foreclosure Surge

Commercial property foreclosure figures from ATTOM Data Solutions reveal an eye-popping 117% spike in foreclosures since last March, which is probably what Jerome Powell wanted to happen.

In March alone there were 625 commercial foreclosures, the highest figure since March 2015 (649 foreclosures). Notably, there were only 288 CRE foreclosures 12 months ago.

Top States for Foreclosures

The top 10 states with the most commercial foreclosures in March 2024 include California, New York, and Florida:

- CA: 187 foreclosures

- NY: 61

- FL: 60

- TX: 55

- NJ: 42

California’s rogue wave of foreclosures clocked in at nearly 30% of all foreclosures nationwide for the month.

As a sign of the times, the 52-story downtown LA Gas Company Tower, appraised at $632M in 2020, is now worth just $200M and is also facing foreclosure.

The Silver Lining

Despite Blackstone’s hope for stabilization, a 117% rise in foreclosures since March 2023 signals distress. March 2024 hit a 9-year high, with CA, NY, and FL leading. While CRE faces uncertainty, single-family housing remains resilient, offering a silver lining.

The good news is that the looming wall of CRE debt, which is tied in with increasing foreclosures, is at odds with single-family housing and BTR portfolios, where national median prices have remained resilient thanks in part to fixed mortgages, a lack of distress, and a dearth of supply.