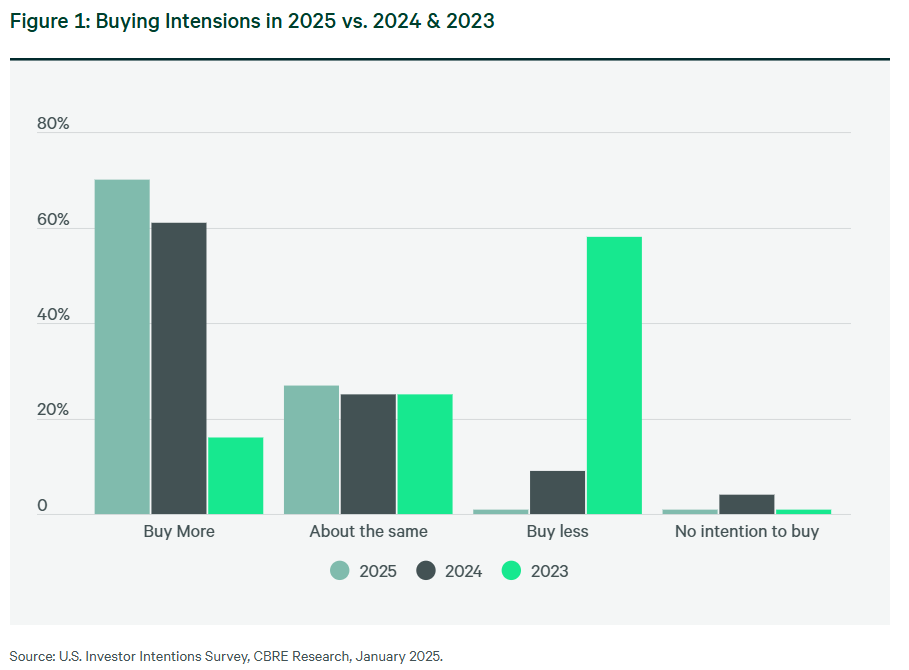

- 70% of investors plan to buy more CRE assets in 2025, with 75% expecting their investment activity to recover by the first half of the year.

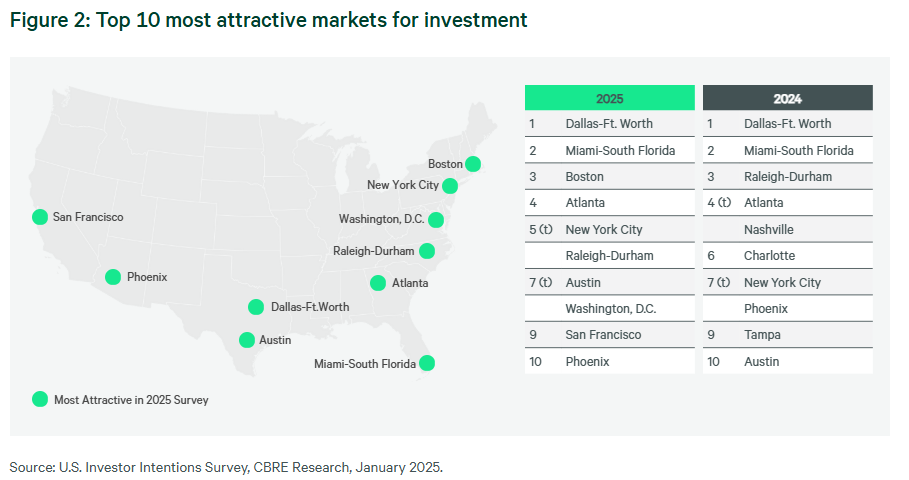

- Dallas, Miami, and Boston lead the list of preferred markets, with San Francisco and New York City reentering the top 10.

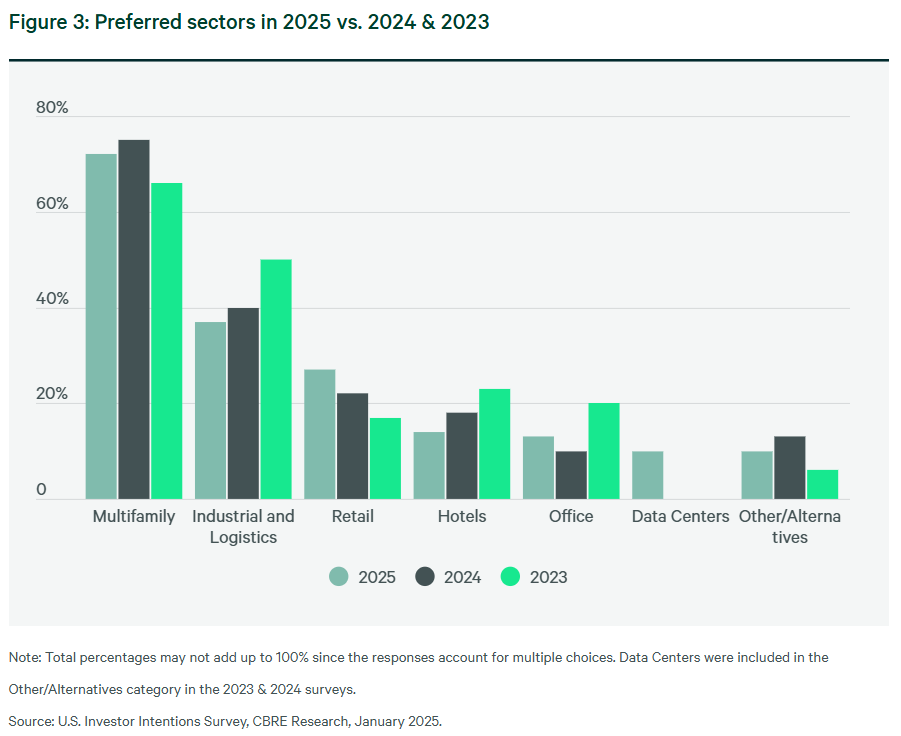

- Multifamily remains the top choice, followed by industrial/logistics and retail, which saw increased investor interest.

- Elevated interest rates and higher borrowing costs remain the biggest challenges, with most investors maintaining their debt-to-equity ratios.

According to CBRE’s 2025 U.S. Investor Intentions Survey, commercial real estate investors are increasingly optimistic about market recovery this year, with 70% planning to acquire more assets than in 2024. While challenges such as volatile long-term interest rates persist, investors are capitalizing on favorable pricing and repositioning strategies for growth.

CBRE predicts the 10-year Treasury yield will stay above 4% throughout 2025, which could slow activity in the first half of the year. However, 75% of investors anticipate their portfolios will recover faster than the broader market, signaling a readiness to secure a first-mover advantage as pricing stabilizes.

Top Markets: Gateway Cities Regain Favor

For the fourth consecutive year, Dallas remains the top market for CRE investment, with Miami/South Florida ranking second. Gateway cities such as Boston, San Francisco, and New York City reentered the top 10 this year, reflecting renewed investor confidence in major urban markets.

The Sun Belt remains a key focus for growth-driven investments, with cities like Atlanta, Austin, Raleigh-Durham, and Phoenix maintaining strong appeal. Investors are also seizing discounted opportunities in gateway markets, balancing their portfolios with high-growth secondary markets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Preferred Property Types: Multifamily Leads, Retail Rebounds

- Multifamily continues to dominate, with nearly three-quarters of investors prioritizing this asset class for its stability and demand.

- Industrial and logistics assets are the second most favored, targeted by 37% of respondents.

- Retail gained investor interest this year, reflecting its post-pandemic recovery and improving fundamentals.

- Office assets also saw a slight uptick in demand as utilization rates stabilized and pricing adjustments made the sector more attractive.

Investors are primarily focused on high-quality assets in traditional sectors, moving away from alternatives like data centers, self-storage, and life sciences. Over half of respondents reported no interest in alternatives, prioritizing repriced opportunities in the core property types instead.

Evolving Strategies: Focus on Value-Add and Core-Plus

Nearly two-thirds of investors are pursuing value-add and core-plus strategies to balance risk and returns. Opportunistic, distressed, and core strategies have seen declines, indicating a preference for moderate risk profiles amid current market conditions.

The shift toward traditional real estate and repriced assets highlights the need to recalibrate strategies as the market enters a new cycle.

Debt Trends: Managing Higher Rates and Leverage

Debt remains a key concern for investors navigating elevated borrowing costs. Key findings include:

- 70% of investors plan to maintain their current debt-to-equity ratios, while 56% are prepared to endure one year of negative leverage.

- Despite challenges, investor interest in mortgage and mezzanine financing remains strong, though slightly lower than in 2024.

- Direct real estate equity investments have become more appealing, driven by favorable pricing and long-term growth potential.

Interest rate volatility and higher borrowing costs continue to weigh on sentiment, making market and asset selection more critical than ever.

Top Challenges in 2025

- Volatile Interest Rates: Elevated rates are the most cited challenge impacting acquisition and debt financing strategies.

- Higher Operating Costs: Inflationary pressures are affecting operating expenses, particularly in multifamily and retail sectors.

- Economic Uncertainty: Despite improved sentiment, uncertainty around interest rate movements remains a concern.

Fewer investors expressed concerns about a potential recession or a disconnect between buyer and seller expectations, signaling increased confidence in the market’s recovery trajectory.

Why It Matters: A Pivotal Year for CRE Recovery

The results of CBRE’s survey illustrate the CRE market’s resilience and investor adaptability. The renewed focus on traditional assets, gateway markets, and value-add strategies signals a stabilization of market fundamentals. Investors are preparing to capitalize on favorable pricing, leveraging a combination of debt, equity, and strategic positioning to take advantage of the ongoing recovery.

2025 marks a critical turning point in the real estate cycle, where disciplined strategy and smart asset selection will separate leaders from laggards.