- The TPPI shows slight quarterly declines across most CRE sectors, signaling stalled momentum following early-year optimism.rn

- Industrial remains the strongest performer, buoyed by data center growth and logistics demand, while lodging continues to underperform.rn

- Tariffs and policy uncertainty are now central risks alongside high borrowing costs, with investors watching closely for the Fed’s next move.rnrnrn

A Pause in the Recovery

After a hopeful start to 2025, commercial real estate prices lost momentum in Q2, according to Trepp’s latest Property Price Index (TPPI). While the Q1 data hinted at the beginning of a recovery, the most recent figures show a cre market largely treading water, with prices dipping slightly across many asset classes.

Two key headwinds—lingering tariffs and elevated borrowing costs—are clouding investor sentiment and transaction volumes, as the Fed’s next rate decision and ongoing trade talks loom large over the sector.

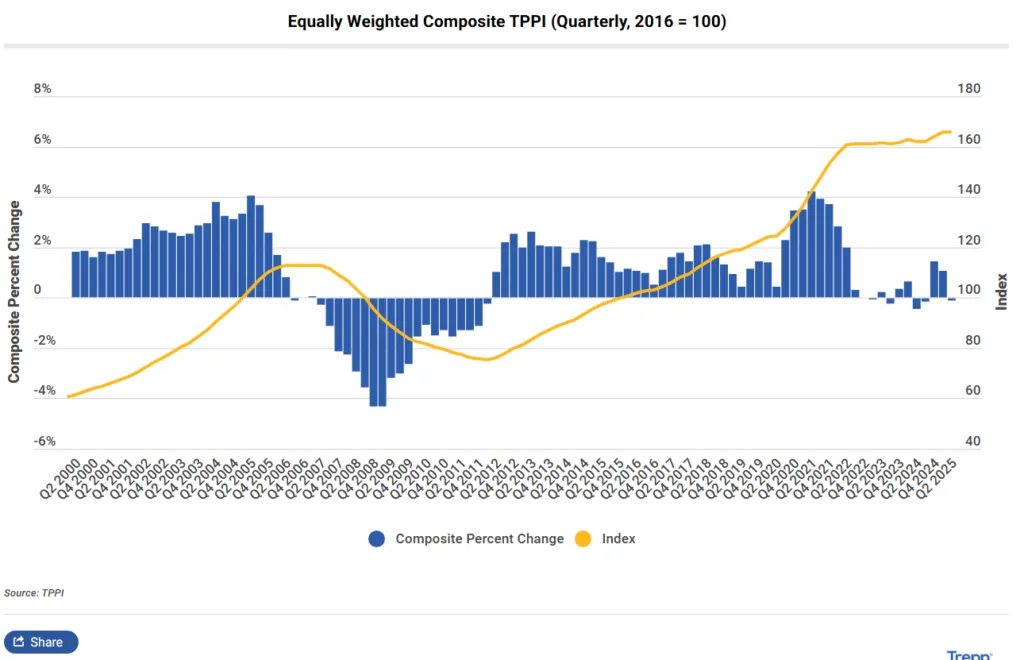

Pricing Metrics Show a Sideways Market

The composite TPPI was relatively flat this quarter. The equally weighted (EW) index fell 0.08% QoQ but is up 2.32% YoY, while the value-weighted (VW) index declined 0.44% QoQ and gained just 1.01% YoY.

The discrepancy between EW and VW indexes signals ongoing bifurcation: smaller and mid-sized assets are seeing more stability, while large, capital-intensive deals continue to struggle under current financing conditions.

Sector-Level Performance

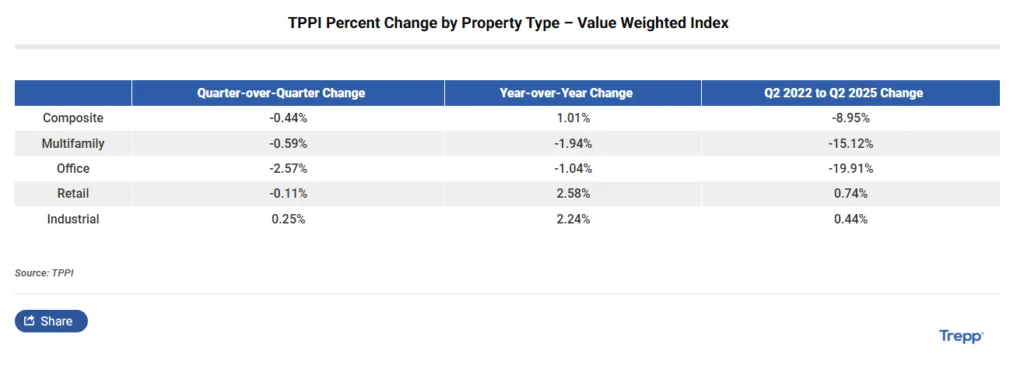

- Multifamily: EW up 1.55% YoY, VW down 1.94% YoY. Elevated supply, soft rent growth, and rising expenses are suppressing valuations, especially in Sun Belt metros.

- Office: EW up 0.47% QoQ, VW down 2.57% QoQ. High vacancy and weak demand persist, with larger assets trading at steep discounts. Some activity in conversions (e.g., 255 West Julian Street in San Jose) points to adaptive reuse opportunities.

- Retail: EW down 0.63% QoQ, VW up 2.58% YoY. Grocery-anchored retail remains stable, but higher import costs could pose future risks as tariffs filter into consumer spending.

- Industrial: EW up 0.30% QoQ, VW up 0.25% QoQ. Remains the market leader due to demand for logistics and data centers. Tariff impacts could shift supply chain strategies and regional distribution needs.

- Lodging: EW down 2.69% QoQ, VW down 9.82% YoY. The weakest sector, still suffering from low business travel and deferred capital improvements. A drop in tourism to Las Vegas highlights affordability pressures even in destination markets.

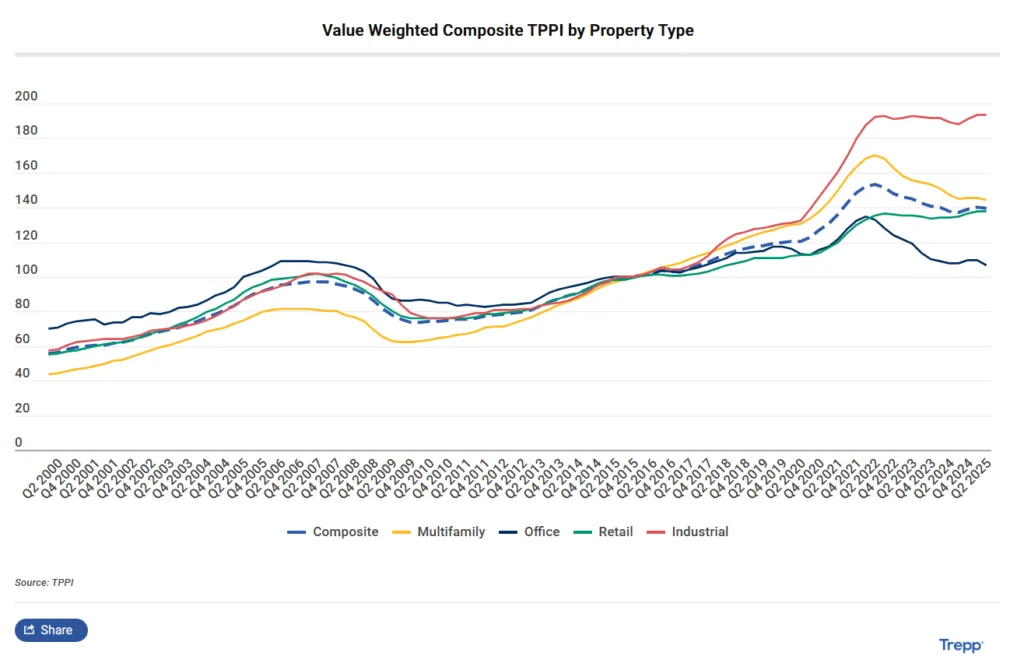

cre sectors from Q2 2022 to Q2 2025, while office and multifamily lag” class=”wp-image-209574″/>

cre sectors from Q2 2022 to Q2 2025, while office and multifamily lag” class=”wp-image-209574″/>Tariffs & Rates: The Dual Threat

Tariffs have joined interest rates as a top-tier risk factor in CRE. Investors and lenders alike are struggling to price deals amid growing policy uncertainty. The expected September rate decision from the Federal Reserve, along with developments in tariff negotiations, could significantly alter the market’s trajectory heading into Q4.

Why It Matters

The TPPI’s Q2 performance signals a CRE market in wait-and-see mode. While some sectors like industrial and retail are holding ground, broader market movement remains muted. With capital costs still high and transaction volume subdued, price discovery remains a challenge.

What’s Next

Looking ahead, the CRE market is highly sensitive to macro developments. If the Fed delivers a rate cut and tariff tensions ease, price momentum could return in late 2025. Until then, investors are likely to remain cautious, with sector-level fundamentals—particularly in office and lodging—continuing to diverge.

Trepp expects future TPPI reports to provide a clearer picture as more transactions are logged and market sentiment adjusts to the next wave of economic and policy shifts.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes