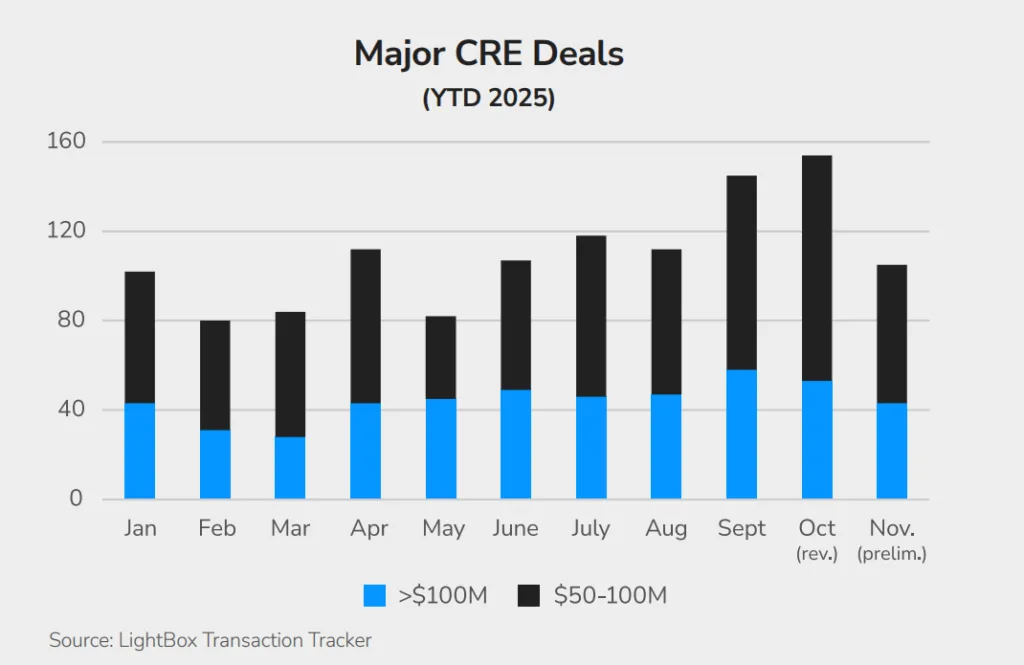

- November recorded 1,214 transactions totaling $23.8B, down slightly from October but typical for a holiday-shortened month.

- Multifamily, retail, office, and industrial each captured roughly one-fifth of deal volume, signaling balanced sector activity.

- High-profile trades in senior housing, student housing, and data center land pushed pricing benchmarks and reinforced demand in niche asset classes.

- Distressed office assets dominated November’s largest discounts, while data center deals in Northern Virginia broke new price records.

Deal Flow Remains Solid Despite Disruptions

Even with a federal government shutdown extending into mid-month and the Thanksgiving holiday truncating the calendar, November delivered a healthy $23.8B in CRE transactions, per LightBox’s latest Transaction Tracker. While volume eased from October’s high, the slowdown aligns with seasonal expectations rather than market fundamentals.

“November’s dip looks like nothing more than a seasonal blip,” said Manus Clancy, Head of Data Strategy at LightBox. “This reflects timing more than any measurable shift in momentum.”

CRE Sector Breakdown: A Near Four-Way Split

In a rare show of balance, multifamily (21.9%), retail (20.4%), office (≈20%), and industrial (≈19%) were nearly tied in transaction share:

- Multifamily remains the most liquid sector, with elevated rental demand and softening prices presenting value opportunities for investors, especially in Sunbelt metros.

- Retail is benefitting from limited new construction and strong consumer spending, which keeps vacancies tight and investor interest high.

- Office continues to bifurcate. Trophy assets with amenities are still attracting capital, while distressed assets face steep discounts.

- Industrial demand remains steady from logistics and manufacturing tenants, even as vacancy nudges upward due to new supply.

Combined, these four property types accounted for 81% of all November deals.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Discounts and Data Center Premiums Highlight Market Extremes

Among transactions with known historical pricing, 62% sold at a gain, while 38% traded at a discount. Notably, six of the ten largest losses occurred in the office sector, underscoring its volatility.

- The largest price drop was the $133M foreclosure of the San Francisco Centre, marking an 89% decrease from its 2016 value.

- On the flip side, Amazon Data Services paid $700M for a data center site in Northern Virginia—over 12x the original land basis.

- SDC Capital followed with a record $615M land acquisition in Leesburg, setting a new high watermark at over $6M per acre.

Mega-Deals Lead November Headlines

Three portfolio sales topped the billion-dollar mark:

- Sonida Senior Living closed a $1.8B acquisition of CNL Healthcare Properties’ senior housing portfolio.

- VICI Properties completed a $1.16B sale-leaseback with Golden Entertainment, enhancing its experiential and gaming real estate footprint.

- Morgan Stanley Real Estate and GSA paid $1B for an eight-property student housing portfolio, reaffirming interest in education-linked assets. Steady pre-leasing performance in the student housing space continues to reinforce investor confidence in the sector’s resilience.

Private equity and institutional players were active across asset classes, while firms like Prologis, Bridge Logistics, and Pantzer Properties remained dominant in industrial and multifamily deals.

Market Signals Point to a Strong 2026 Start

While closings dipped 6% month-over-month, the LightBox CRE Activity Index stayed above 99, suggesting seasonal softening, not structural weakness. Several early-stage indicators support optimism heading into Q1 2026:

- Listings surged 37% YoY, as sellers returned to the market.

- Environmental due diligence (ESA) volume climbed 12%, with strength in multifamily, manufacturing, and data centers.

- Appraisal activity held steady for the 11th straight month, signaling lender re-engagement.

“We’re beginning to see the kind of alignment in listings, diligence, and lender engagement that supports real liquidity,” Clancy noted.

Why It Matters

The November data reveals a CRE market adjusting to macro pressures without derailing. Balanced sector participation, record-setting trades, and a narrowing gap between buyers and sellers all point to a healthier transaction environment as the market prepares for a more active 2026.