- CRE valuations are now less expensive than US equities, a first in two decades.

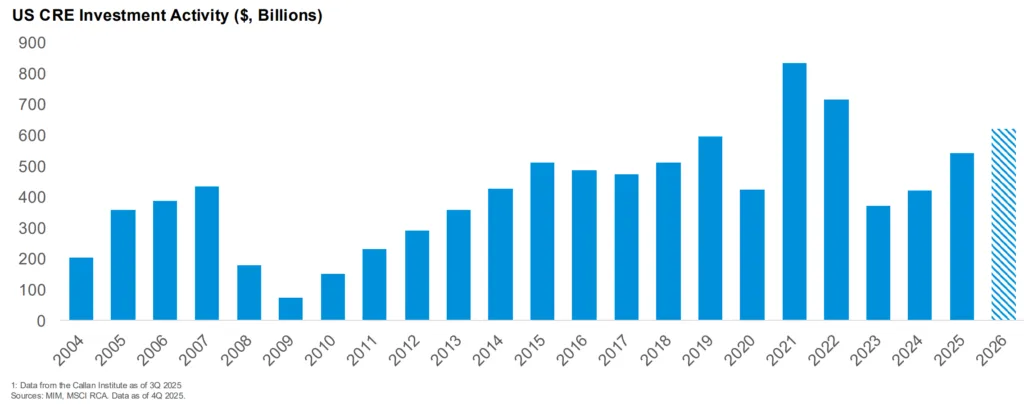

- Investment activity in CRE is rebounding as price discovery improves and distressed sales decline.

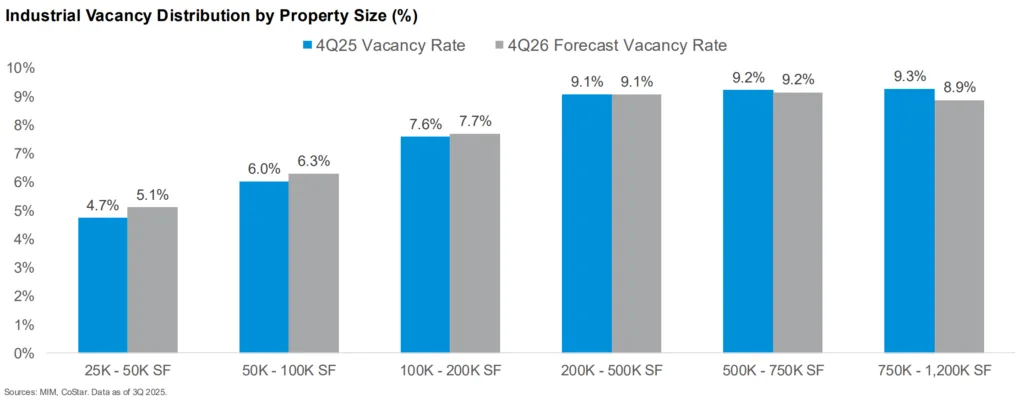

- Asset classes like senior housing, infill industrial, and medical office show strong fundamentals and recovery potential.

- Office remains the most distressed sector, but top-tier assets in growth markets are stabilizing.

CRE Valuations Fall Below Equities

Globe St reports that for the first time in nearly 20 years, commercial real estate (CRE) valuations have fallen beneath those of US equities, according to MetLife Investment Management’s latest Chartbook. The shift, led by the underperforming office sector, signals CRE is now “cheap” relative to the broader stock market and may present fresh opportunity for investors.

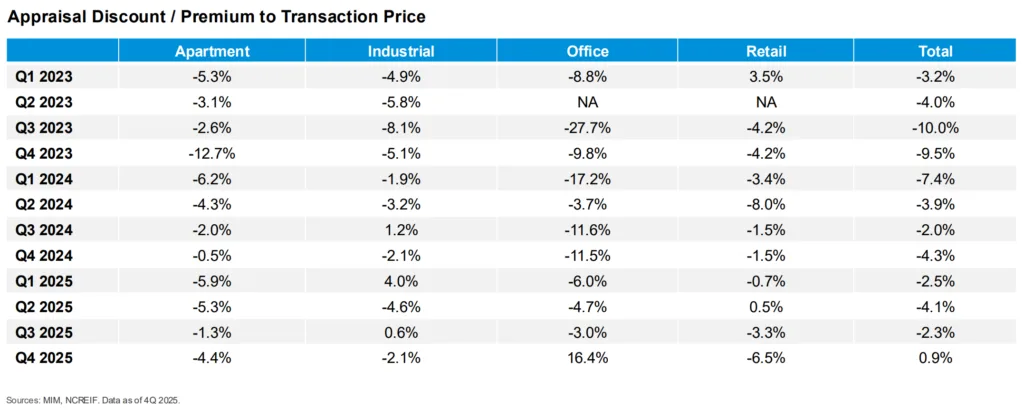

The valuation gap is measured using the inverse of cap rates—a property market equivalent to stocks’ price-earnings (P/E) ratio—which now favors CRE. Stable appraised values and a narrowing difference between appraisals and transaction prices are fostering renewed investor confidence.

Investor Momentum Builds

Commercial real estate transaction volumes have started to recover from the lows of 2023 as redemption pressures subside. The NFI-ODCE redemption queue, a proxy for investor withdrawal demand, fell from 19% of NAV in 2023 to 12% in early 2026, indicating improved fund liquidity and sentiment within the sector.

Investment managers expect private CRE values—which bottomed in late 2024—to post nearly 5% price growth in 2026. The broad opportunity set includes sectors aligned with national trends like AI expansion, demographics, and housing shortages, with data centers, seniors housing, and manufactured housing already surfacing as outperformers in institutional indexes. That relative repricing between public and private markets has also prompted some listed real estate vehicles to pursue alternative capital strategies to close persistent valuation gaps.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Assets and Markets to Watch

Sectors including seniors housing, infill industrial, medical office, and net-lease retail currently screen as having the most compelling risk-adjusted returns, according to MetLife’s sector analysis. Each offers either stable fundamentals or meaningful value resets, while supply constraints remain critical in select gateway cities.

Despite lingering distress, the office market is showing the first signs of stabilization. Net absorption turned positive, and national vacancy retreated slightly to 18.8%. Markets such as Miami, Tampa, and Fort Lauderdale have fully recovered post-pandemic, particularly for Class A office product. However, weaker Class B and C assets may continue to experience downward pressure.

What’s Next

With CRE valuations lagging equities and inflation, institutional capital is expected to return as price transparency and fundamentals improve. Tight supply pipelines and demographic demand, especially for senior housing and industrial, support a positive outlook for price appreciation in 2026. As CRE valuations screen as attractive relative to both corporate bonds and stocks, investor attention is likely to shift toward sectors and markets demonstrating solid recovery momentum.