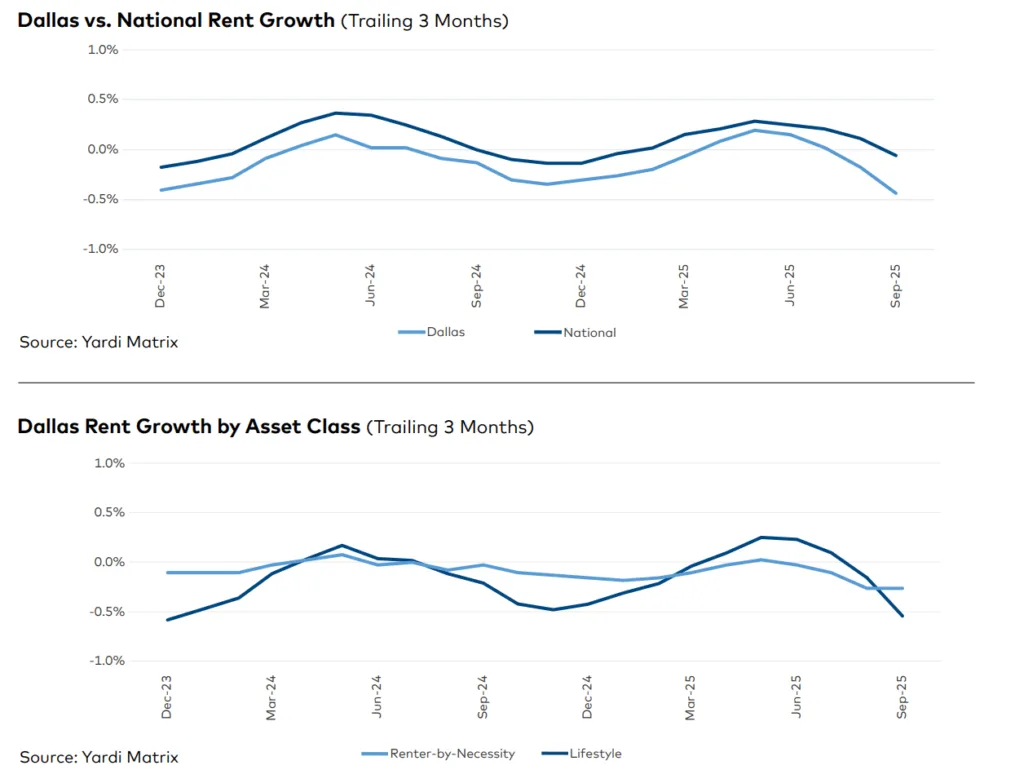

- Average asking rents in DFW dipped 0.4% through September 2025, underperforming the national average.

- Despite elevated supply, stabilized occupancy edged up to 93.1%, though it remains below the US benchmark.

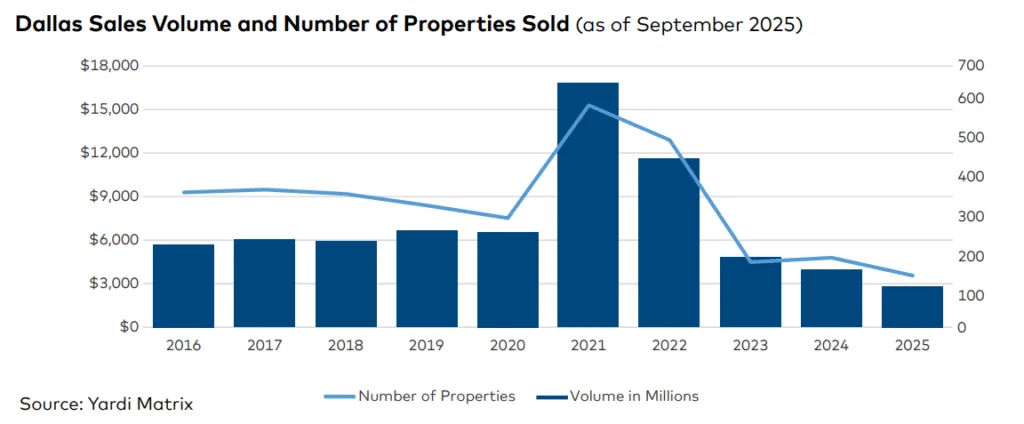

- Investment activity is muted, totaling $2.9B year-to-date—less than half the metro’s 10-year average.

- Deliveries fell 25% year-over-year, with developers reining in new projects amid economic headwinds.

Market Overview: Steady Demand, Slowing Rents

Dallas–Fort Worth’s multifamily market remained fundamentally stable through the first three quarters of 2025, despite facing challenges from elevated supply and shifting macroeconomic conditions, according to a recent Yardi Matrix report highlighted by Multi-Housing News.

Average advertised asking rents slipped 0.4% on a trailing three-month basis through September, settling at $1,518—below the national average of $1,750. Year-over-year, rents contracted by 1.9%, placing DFW among the five metros with the largest rent declines in Yardi Matrix’s top 30 markets.

The Lifestyle segment saw rents drop 0.5% to $1,700, while Renter-by-Necessity units dipped 0.3% to $1,263—marking the 16th straight month of negative rent movement for the latter.

Occupancy Holds Firm Amid New Supply

Stabilized occupancy inched up 10 basis points year-over-year to 93.1% in August, despite the influx of new units. Lifestyle properties led the trend with a 50-basis-point improvement to 94.1%, offsetting a 50-basis-point dip in RBN properties (91.7%).

While several high-end submarkets saw rent declines—Highland Park (-6.0%) and University Park (-2.8%) among them—others like Fort Worth–Central (6.2%) and Grapevine (0.3%) registered gains.

Development Slows, but Pipeline Remains Deep

Deliveries slowed significantly, with 20,312 units completed through September—a 25.1% drop from the same period in 2024. Still, construction remains active, with 50,270 units underway and another 147,000 units in planning or permitting stages.

The bulk of activity is concentrated in North Dallas, which accounts for nearly half of all units under construction, a trend consistent with recent permitting surges across the metro. Notably, the region also led recent completions, delivering 10,928 units in 2025 through Q3.

Construction starts fell nearly 20% year-over-year to 14,723 units as developers pull back amid tepid rent growth and capital market uncertainty.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Transaction Volume Dips Below Historical Norms

DFW’s multifamily investment activity totaled $2.9B through September 2025, significantly below the metro’s 10-year average of $7B. Sales were fairly evenly distributed across the year, though North Dallas alone accounted for more than half of the year-to-date volume ($1.5B).

The average price per unit rose 4.1% year-to-date to $166,783 but remains well below the national average of $209,188.

Notable recent transactions include:

- The Fairmount at Oak Lawn (Dallas): $95M | $258,261/unit | Buyer: KKR

- The Ownsby (Celina): $88M | $237,771/unit | Buyer: BSR Trust

- Ovation at Galatyn Park (Richardson): $70M | $192,665/unit | Buyer: MG Properties.

Job Growth Supports Long-Term Fundamentals

Employment in DFW expanded 1.1% year-over-year through July—above the national rate of 0.8%. The metro added 44,000 jobs, with education and health services (+17,000) and government (+12,200) leading gains.

However, unemployment rose to 4.4%, slightly above both state and national levels.

Major infrastructure investments are bolstering long-term economic prospects. DART’s Silver Line commuter rail and Wells Fargo’s new 850,000 SF campus in Irving signal continued confidence in the region’s growth trajectory.

Why It Matters: Fundamentals Still Strong, But Market is Resetting

DFW remains one of the nation’s most active multifamily markets, but it’s entering a phase of correction. While long-term population and employment growth support demand, rent stagnation, high supply, and capital market constraints are cooling near-term activity.

Investor sentiment is improving modestly due to lower interest rates and signs of national stabilization, but developers are cautious. This rebalancing phase may help the market absorb excess supply heading into 2026.

What’s Next: Eyes on Absorption and Leasing Velocity

With 50,000+ units under construction and demand moderating, absorption and leasing velocity will be key metrics to watch in 2026. Developers and investors alike will be monitoring occupancy rates closely, especially in high-supply submarkets like North Dallas and Fort Worth.

Expect continued investor focus on well-located, stabilized assets and a cautious approach to ground-up development as the market works through its current inventory.