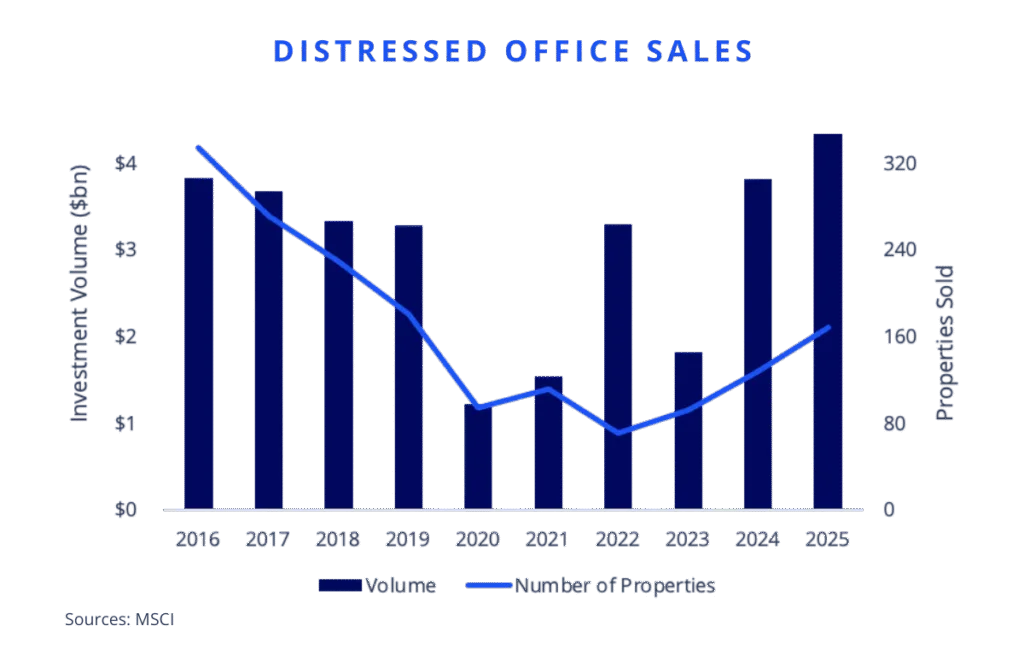

- Distressed office investment volume reached $4.3B in 2025, the highest level since 2016, with 168 properties trading hands—a 31% year-over-year increase.

- Private buyers dominated the market, accounting for 55.3% of all transactions.

- The New York City metro led the way with $1.1B in distressed office deals as investors bet on leasing market recovery.

- A post-pandemic shift toward hybrid work and falling valuations accelerated defaults and lender takebacks, creating buying opportunities.

Market Recap

Distressed office investment volumes surged in 2025, totaling more than $4.3B—marking the sector’s busiest year in a decade and surpassing previous highs seen in both 2016 and 2024. According to Colliers, the total number of office buildings sold under distress jumped 31.3% from the prior year to 168 assets, aligning with the 10-year average.

Leading The Way

Private capital drove the bulk of acquisitions, representing 55.3% of all deals. Investors were particularly active in the New York City metro area, which notched $1.1B in distressed sales as buyers sought upside in a recovering leasing environment. However, investor hesitation remains in parts of the office market. Net lease segments, in particular, continue to see slowed transaction volume due to uncertainty over long-term occupancy.

From Pandemic Lows To Repositioning Plays

Office demand collapsed between 2020 and 2021, as remote-first work models became entrenched and occupancy dropped to historic lows. By 2024, companies reevaluated the productivity of remote work. Many saw limits to collaboration and culture in remote-only setups. As a result, more employers issued return-to-office mandates. Office attendance began to climb, especially in premium Class A-plus buildings. These top-tier spaces reached 78% of pre-pandemic occupancy, outpacing the broader market.

The Opportunity In Distress

As office values declined and debt burdens grew heavier, mortgage defaults and lender takebacks became more common. Buyers capitalized on discounted pricing, with many seeing upside in repositioning efforts—from cosmetic upgrades to full-scale conversions of obsolete space.

What’s Next

With distressed sales now setting new pricing benchmarks, investors and developers are deploying capital not just to stabilize assets, but to reimagine them for a more flexible and hybrid future. Expect this trend to continue as cities and investors adapt to post-pandemic demand realities.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes