- Fit-out costs continue to rise globally due to labor shortages, material price volatility, and trade policy impacts.

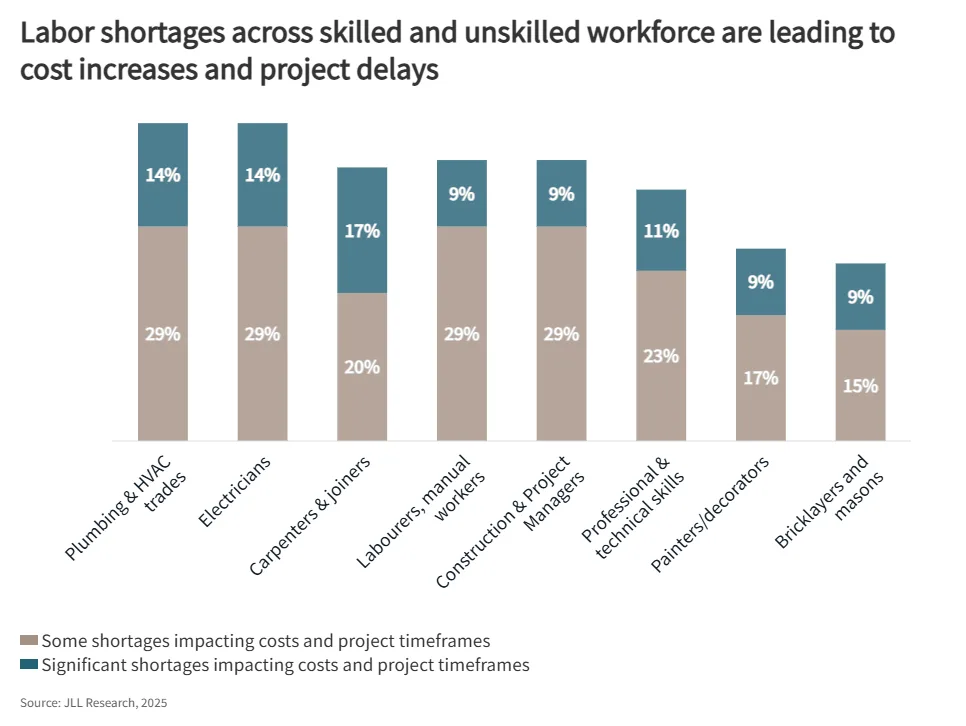

- Skilled labor remains scarce, especially in M&E trades, driving up wages and project delays across key markets.

- Sustainability demands are adding complexity, with higher specifications for energy efficiency and employee wellbeing.

- Technology integration is increasing costs, as AI adoption drives demand for smart systems and future-proof infrastructure.

Global Pressures, Local Impacts

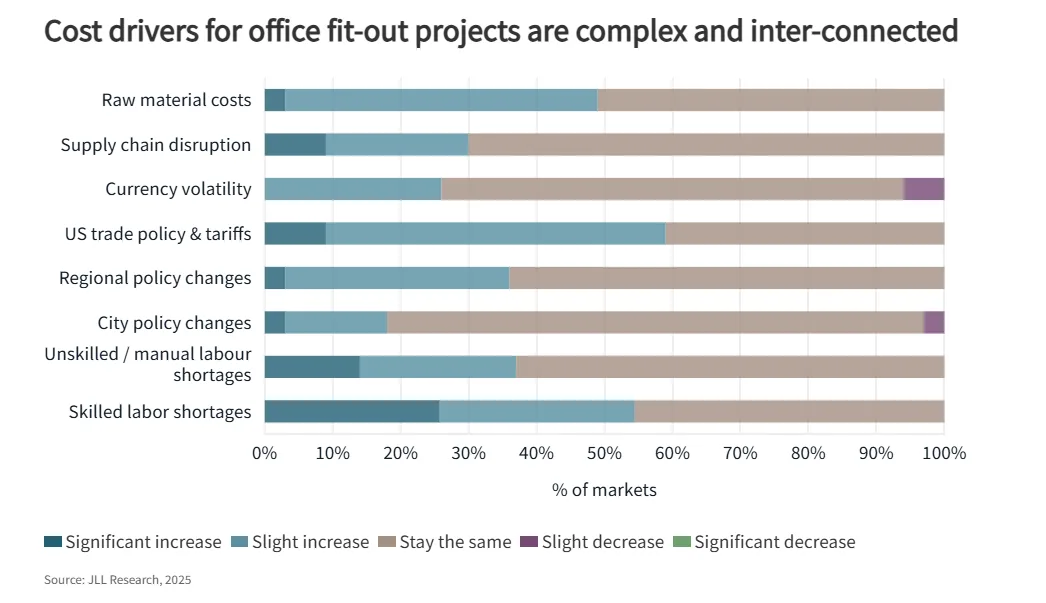

Office fit-out costs in 2025 are being shaped by a complex interplay of global and local forces, reports JLL. While post-pandemic inflation has moderated in many areas, key cost drivers—like raw material pricing, trade dynamics, and workforce shortages—continue to challenge project delivery. In particular, US trade policies and tariffs have emerged as the most cited global factor, impacting 62% of markets surveyed by JLL. These effects are felt most strongly in North America and Asia-Pacific.

Labor shortages follow closely behind, affecting both skilled and unskilled workers in over half of markets reviewed. Specialized trades like M&E technicians and HVAC specialists are scarce, with the worst shortages reported in Central and Western Europe. In APAC, aging populations and infrastructure projects strain labor, while North America faces shortages due to restrictive immigration policies.

Meanwhile, raw material costs—especially for steel and metals—remain high in the US and continue to influence global pricing. Although prices for some commodities have stabilized since pandemic-era peaks, volatility persists due to fluctuating global demand and supply chain disruptions.

Breaking Down Cost Categories

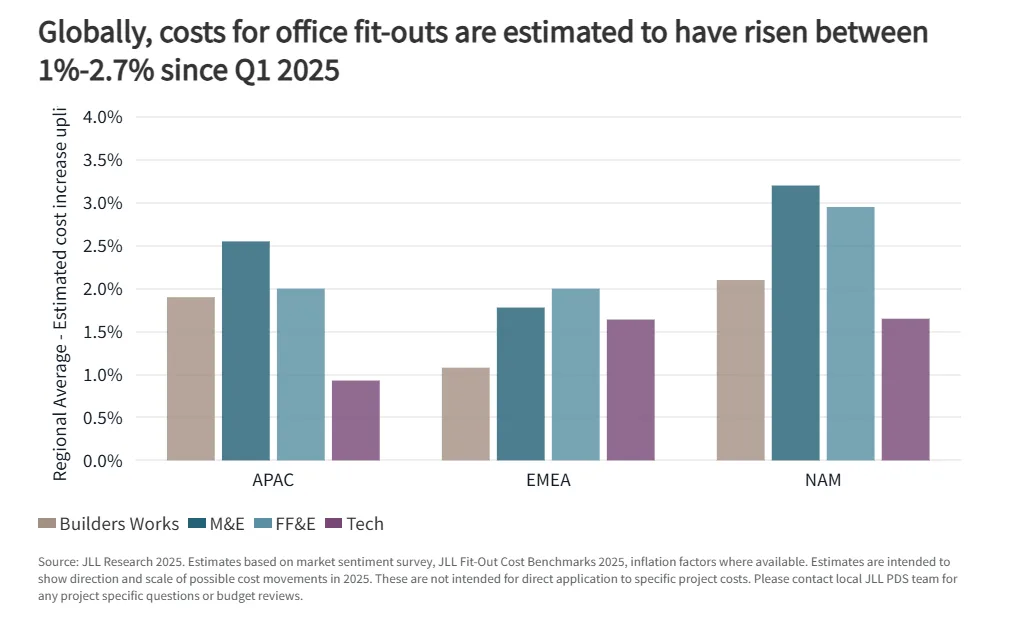

JLL’s Global Office Fit-Out Cost Benchmarks show varied trends across the four primary cost components in 2025:

- Builder Works (partitions, flooring, etc.): Prices have largely stabilized, though still influenced by raw input and regional trade policies.

- M&E Systems: This category faces the most significant increases, driven by HVAC equipment shortages, rising installation costs, and sustainability-linked specifications.

- Technology Systems: Smart building features and AI-driven infrastructure have driven costs higher, especially in EMEA. APAC, however, is benefiting from closer access to manufacturing and fewer import costs.

- FFE (Furniture, Fixtures & Equipment): Costs rose modestly (1.8–3.0%), largely in response to material and logistics factors.

Labor: A Persistent Pressure Point

Workforce limitations are now a defining factor in project planning. As building systems become more complex and ESG-driven retrofits gain ground, the need for specialized labor grows. Construction for industrial facilities and data centers is further intensifying the competition for talent, particularly in HVAC and BMS (Building Management Systems) roles.

In 2026, project timelines and delivery outcomes will increasingly depend on local labor strategies and contractor vetting. Early engagement with talent pipelines will also be critical. These factors are especially important in Europe and North America, where wage premiums are rising rapidly.

Sustainability Is Non-Negotiable

Sustainability is no longer an optional premium—it’s a core expectation. With 71% of global markets now reporting increased demand for sustainable fit-outs—up from 60% in Q1—demand is clearly growing. Organizations are prioritizing low-carbon, energy-efficient solutions that meet regulatory standards and support corporate ESG mandates.

In EMEA and APAC, demand is highest, fueled by policy support and employee expectations. Fit-outs are now expected to include advanced HVAC, better air quality systems, and low-emission materials, often tied to building certifications. These features, while cost-intensive upfront, are viewed as long-term value drivers.

Tech Complexity Raises The Stakes

As AI and automation reshape the modern workplace, technology integration is altering the baseline for fit-out projects. According to JLL, 63% of global markets are seeing higher tech specifications, including demand for:

- Predictive occupancy and energy systems

- Enhanced AV and video conferencing

- VR/AR-enabled collaboration spaces

- Scalable BMS platforms

Markets like North America, Singapore, Australia, and the UK are leading the charge. However, rising tech costs, chip shortages, and longer lead times are likely to keep upward pressure on budgets in 2026, especially for future-proofed, high-spec projects.

Looking Ahead To 2026

The path forward for office fit-outs hinges on managing cost complexity and strategic planning:

- Labor strategy will be critical, especially as shortages persist in key skilled trades.

- Supply chain resilience must be strengthened through vendor relationships and localized sourcing where possible.

- Technology readiness—including adaptable infrastructure—will be essential for supporting evolving business needs and AI-driven workplace transformation.

The convergence of labor scarcity, sustainability imperatives, and tech transformation means that costs will remain elevated and variable, but strategic planning, early risk assessment, and flexible design will be key to unlocking value in fit-out investments.