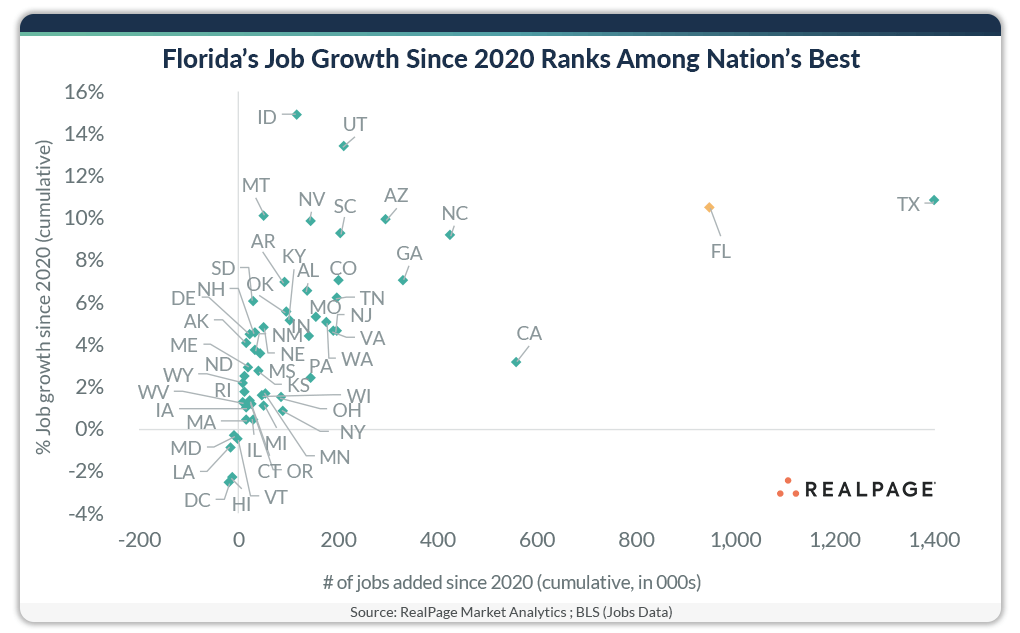

- Florida added 950K jobs from 2020–2024, second only to Texas in total job growth.

- Despite strong employment gains, Florida’s apartment market faces supply-driven challenges.

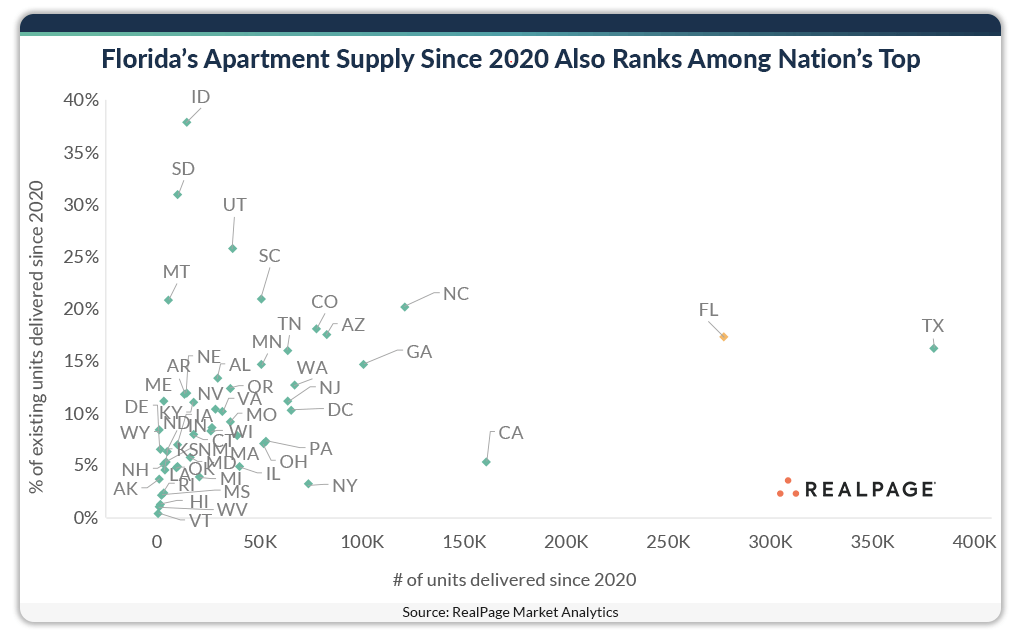

- 285K new market-rate apartments have been delivered in Florida over the past four years.

- Orlando led the state with 50.2K new apartment units, followed by Miami and Tampa (~40K each).

- Jacksonville’s apartment stock grew by nearly 20% as 30K units were added.

According to the Bureau of Labor Statistics, Florida has been one of the top states in the nation pumping out new jobs over the past four years.

Supply Boom Offsets Demand

Specifically, the Sunshine State added 950K jobs between 2020 and 2024, per Bloomberg, trailing only Texas in total job gains over the same period.

Meanwhile, Florida’s employment growth rate surpassed most states, except for smaller and historically underappreciated pre-pandemic markets like Utah and Idaho.

While job growth typically does translate to stronger apartment demand, Florida’s rental market is facing sudden headwinds due to record-high supply levels.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Supply Boom Lowers Demand

Over the past four years, developers have delivered 285K market-rate apartments across Florida, also ranking second behind Texas (395K units), but well ahead of California (170K units). Notably, Florida’s population of 23M is nearly half that of CA, making the new supply even more significant.

Among Florida’s metro areas, Orlando saw the biggest influx of new apartment units, with 50.2K deliveries since 2020. Miami and Tampa followed, each adding around 40K units, while Jacksonville saw 30K new completions.

Jacksonville, a much smaller market with just over 148K existing units, saw its total apartment inventory grow by nearly 20%. By comparison, Tampa and Orlando have nearly 300K units each, while Miami’s rental stock is even larger at 340K units.

Too Good To Be True?

While the Sunshine State’s multifamily market is in a great place right now, nothing good lasts forever, and there are already signs that a slowdown is on the horizon.

Despite robust job growth, the sheer volume of new apartment deliveries has softened statewide rent growth and occupancy rates.

As supply continues to hit the market, multifamily performance challenges may soon spring up like daisies, even as employment fundamentals remain strong.