- GSAM targets “special properties” in sectors like offices and warehouses, where the value remains strong despite market-wide concerns.

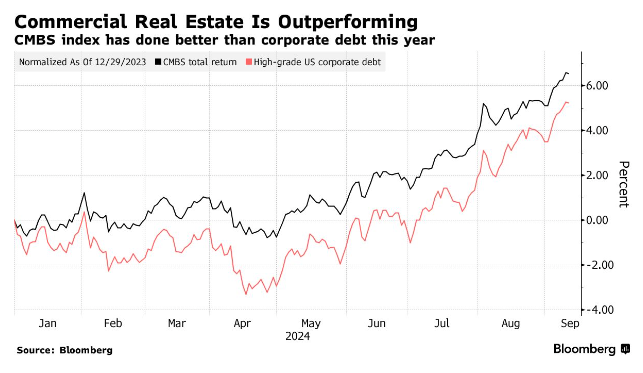

- GSAM prefers CMBS over corporate bonds due to its stronger performance this year, despite broader economic uncertainties.

- Rosner remains optimistic about the overall credit markets, emphasizing the value in BBB-rated companies and shorter-term Treasuries.

According to Bloomberg, Goldman Sachs Asset Management (GSAM) is seeing opportunities in commercial real estate debt, a sector many investors are still cautious about thanks to high vacancies and financing challenges.

According to Lindsay Rosner, head of multisector investing at GSAM, the firm is focusing on commercial mortgage-backed securities (CMBS), specifically tied to high-quality properties.

Picky Approach

While many investors are shying away from CRE debt due to rising vacancies, Rosner argues that the entire asset class is not under threat.

She told the Bloomberg Intelligence Credit Edge podcast that GSAM focuses on “super desirable” properties, where demand remains robust, and is carefully selecting assets within the CMBS space.

Rosner points out that, despite fears, commercial property debt has outperformed investment-grade corporate debt this year, which positions CMBS as a core part of the firm’s portfolio.

Mixed Outlook

The firm sees value in industrial warehouses used for logistics, driven by continued e-commerce growth. In contrast, offices present more challenges due to the persistence of remote work.

Rosner suggests that a full recovery in the office market is unlikely in the short term, but there are still select opportunities for high-quality office buildings in prime locations.

Optimistic About Credit

Goldman Sachs is maintaining a positive stance on credit markets overall. Rosner expects yields to remain attractive, and she estimates the chance of a U.S. recession is just 15–20%.

This means investors still have a lot of value left to find, particularly in financial sector issuers and BBB-rated companies that have maintained their cash reserves.

Balanced Debt Portfolio

Beyond CRE debt, GSAM is also focusing on bank bonds, especially those from European institutions like French banks, which offered opportunities for post-election uncertainty.

Meanwhile, the firm is steering clear of utility-sector bonds due to the financial pressures created by the green transition. Finally, GSAM favors shorter-term Treasury bonds (3- to 5-year maturities are the most attractive), anticipating a steepening yield curve after the U.S. election.