- Higher borrowing costs have significantly increased consumer debt, particularly for mortgages, credit cards, and auto loans.

- Credit card balances have surged, with average interest rates and payments hitting record highs.

- Many Americans struggle to keep up with debt payments, leading to higher delinquencies and financial instability.

Despite the U.S. economy’s resilience against higher inflation and interest rates, individual borrowers are finding themselves on shakier financial ground.

As the Federal Reserve’s rate hikes take effect, borrowing costs have surged, leaving many consumers mired in debt, according to the Wall Street Journal.

Mired in Debt

The Federal Reserve’s rate hikes have pushed borrowing costs for homes, cars, and credit cards to their highest levels in decades.

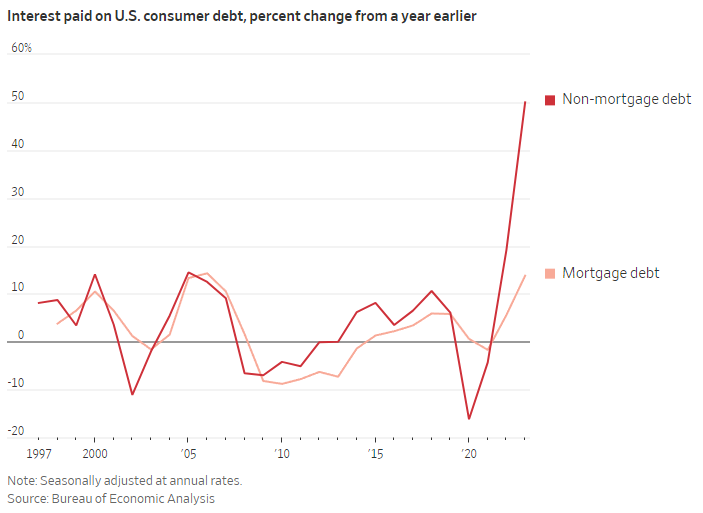

According to data from the Bureau of Economic Analysis, the total interest paid on mortgages rose by 14% in 2023 from the previous year, while interest on other types of consumer debt, such as credit cards and auto loans, jumped up 50%.

Country of Credit Cards

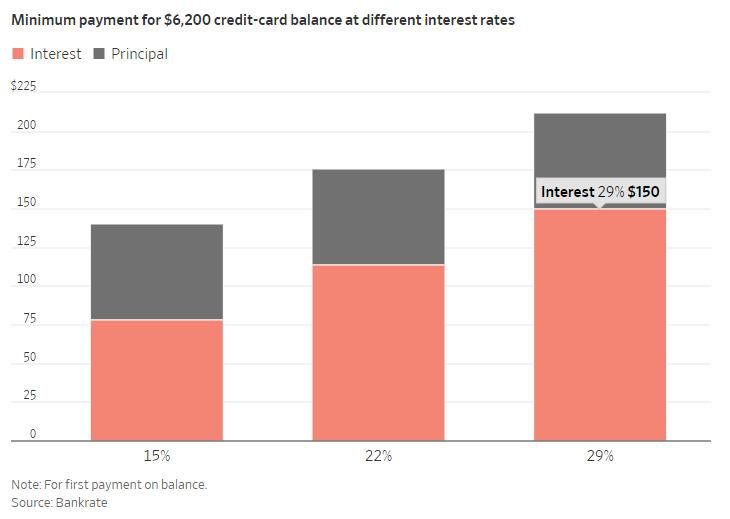

Americans are also relying on credit cards more than ever before, with balances rising to over $1.1T in Q1, nearly 33% higher than in 2022, according to New York Fed data.

The average credit card balance has also surpassed $6K, with interest rates hovering around 22%, the highest levels on record since 1996.

Naturally, monthly debt payments and delinquency rates have both soared, particularly for hard-pressed borrowers with lower credit scores.

Homeownership Challenges

Soaring mortgage rates have made homeownership unattractive (or unattainable) for millions of Americans.

Potential home sellers, especially those who bought in 2020–2022, are reluctant to give up their ‘locked-in’ low mortgage rates, limiting inventory and keeping prices high.

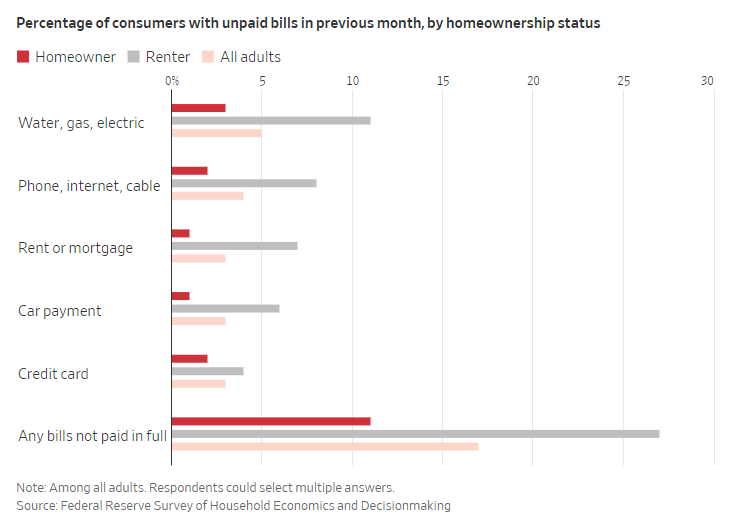

Meanwhile, renters are facing higher rents and higher monthly debt payments, which has resulted in more delinquencies compared to homeowners.

Rising Tide Lifts All Debts

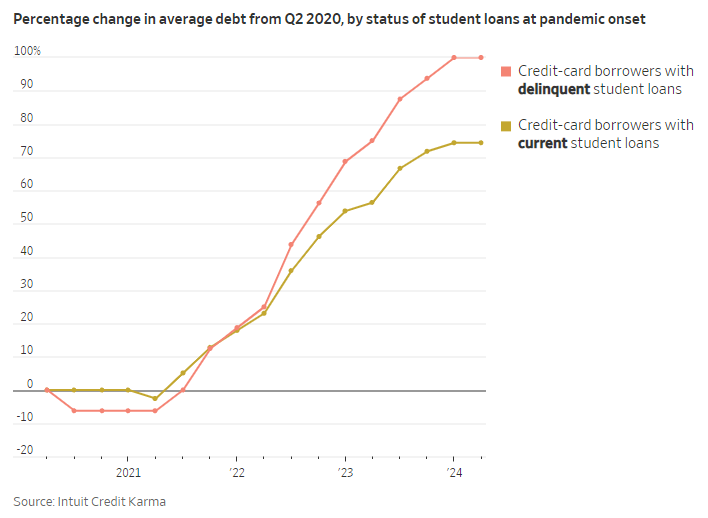

The resumption of federal student loan payments has also further strained borrowers, with around 40% missing their first required payment.

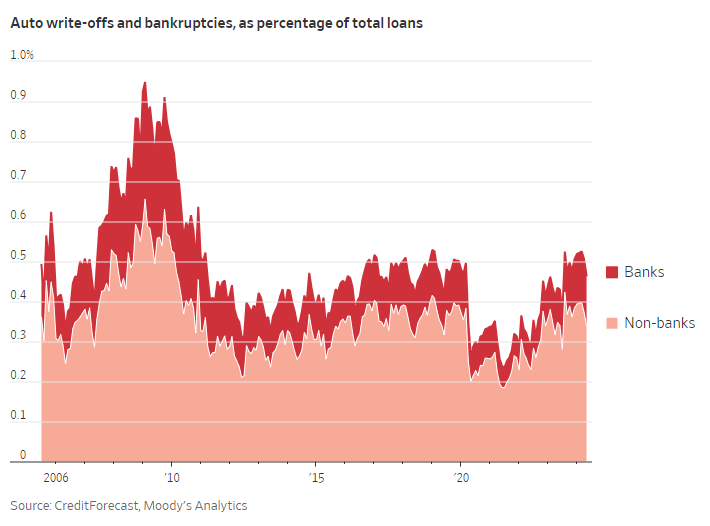

Auto loans have also grown burdensome, with write-offs at banks reaching their highest levels since 2011.

The rising costs of vehicle insurance, maintenance, and repairs, coupled with high loan interest rates, have left many borrowers owing more than their cars are worth, resulting in more repossessions.

Why It Matters

As borrowing costs stay high, American consumers continue to grapple with higher debt loads and more financial instability than ever before.

So, while the overall U.S. economy remains robust on a big-picture level, the strain on individual borrowers highlights the broader, longer-term impact of high inflation and interest rates on personal finances.