- Industrial sector rent growth averaged 5.1% year-over-year, led by Atlanta and key Sun Belt markets.

- Data center construction surged, with development heavily concentrated in just five major metros.

- Supply chain volatility continues as trade policy shifts and legal rulings reshape market certainty.

- Los Angeles remains a top market for industrial investment despite recent price declines.

Market Rents and Occupancy

Yardi Matrix data shows industrial fundamentals remained resilient into early 2026. National in-place rents reached $8.94 per square foot in January. That marked a 5.1% increase year over year. Atlanta led the country with rents rising 8.0% annually. Miami and Tampa followed closely, each posting 7.4% growth. Meanwhile, national vacancy climbed to 9.6%.

Even so, demand for high-quality industrial space remains strong. Sun Belt markets continue to drive above-average rent growth. Tampa recorded one of the widest spreads between new leases and market averages. That gap signals sustained tenant demand for newly delivered space.

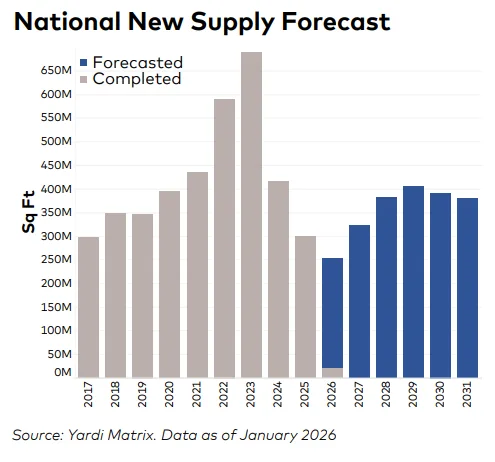

Data Center Boom Concentrated

The industrial sector’s supply boom is being fueled by record data center development, driven by ongoing investments in generative AI. In 2025 alone, 30.8M KSF of data center starts were recorded—well above previous periods—with nearly 57% happening in five metros: Washington, D.C., Dallas, Phoenix, Atlanta, and Columbus. The rapid expansion is also reshaping local labor markets, as contractors compete for electricians, engineers, and other skilled trades to meet aggressive construction timelines. While investor caution is rising over potential AI bubble risks, demand from hyperscale users is keeping construction at elevated levels in these core markets. Nationally, projects under construction total 355.7M KSF, or 1.7% of overall stock.

Policy Shifts and Economic Pressure

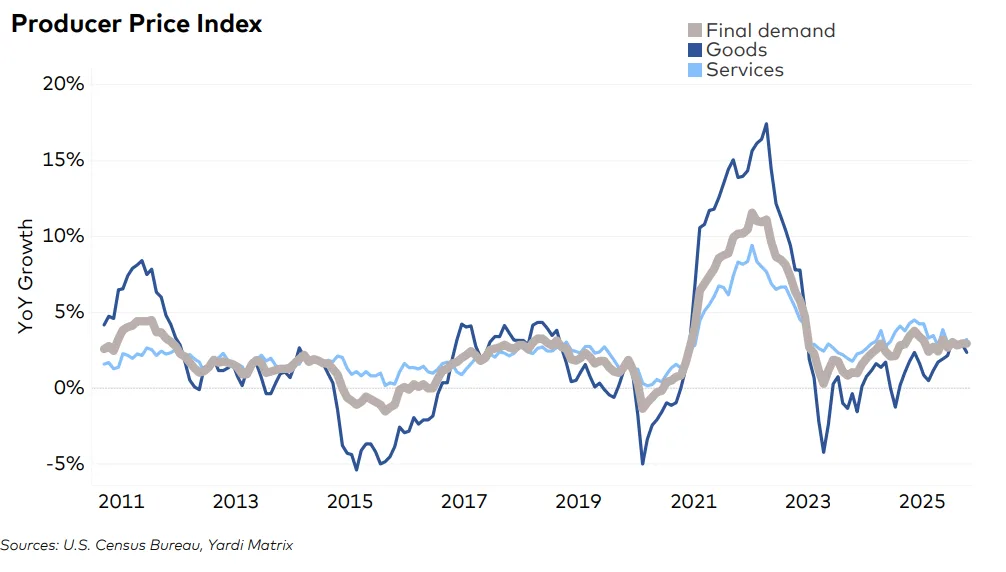

Global trade policy disruptions and legal decisions are creating lasting uncertainty at US ports and across the industrial sector. The Supreme Court’s recent decision limiting unilateral tariffs offered short-term relief to ports but coincided with new global tariffs and unresolved crane upgrade concerns. Rising producer prices, including a 6% year-over-year increase for truck transport, are adding cost pressure to industrial tenants and supporting demand for modern, efficient logistics facilities as users seek to manage margins and supply chain resilience.

Investor Demand Holds in Major Markets

Industrial sector investment showed continued resilience, with $4.1B in deal volume nationally in January at an average price of $166 PSF. Los Angeles reported strong activity, with $356M in transactions, including a notable South Bay sale for $123M. While average pricing in Los Angeles declined 13% from 2023 to 2025, it remains up nearly 50% over 2019, underscoring investor confidence in markets with chronic supply constraints and robust distribution demand.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes