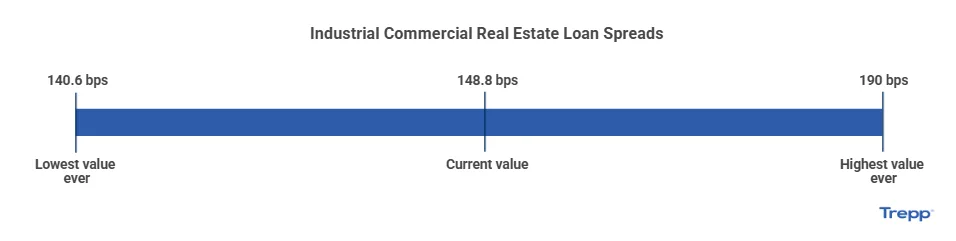

- Industrial spreads have tightened to a 2025 low of 148.89 basis points, reflecting increased lender confidence.

- Lenders are showing strong appetite for low-leverage industrial loans, even amid broader economic uncertainty.

- Spreads have been declining by an average of 2.13 bps per month since May, signaling a stable credit outlook.

- Limited room remains for further compression, suggesting margins on high-quality loans may have peaked.

Industrial Spreads Reflect Resilient Lending Conditions

Spreads on industrial commercial real estate (CRE) loans have continued to narrow in 2025, reports Trepp. Lenders are showing increasing willingness to issue loans even as broader economic uncertainty lingers. According to Trepp’s Trepp-i Weekly Survey, low-leverage industrial loan spreads (50–59% LTV) have compressed each month since May. They now sit at 148.89 basis points over the 10-year Treasury—a new 2025 low.

This level was last seen in early March 2022, just before the Federal Reserve kicked off its aggressive rate-hiking campaign. The recovery in spread levels suggests that lenders are once again comfortable taking on industrial credit risk. It reflects greater market stability and optimism about the sector’s future performance.

A Closer Look At Lending Sentiment

Unlike CMBS spreads, which are more transparent and frequently priced, CRE loan spreads are private, offering fewer benchmarks. Trepp’s weekly survey fills that gap, providing real-time insight into lender behavior.

The recent tightening in industrial spreads—averaging 2.13 basis points in monthly decline—signals a deliberate shift in lender strategy. While the narrowing points to robust capital availability and competitive underwriting, it also suggests pricing for top-tier industrial assets may be nearing a floor. This is especially true given the thin margins on high-quality credit.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Why It Matters

The industrial sector continues to be a bright spot in CRE, supported by persistent demand for logistics, warehousing, and distribution space. Tightening spreads show lender confidence in industrial CRE fundamentals, despite ongoing uncertainty in the broader economic environment.

For balance sheet lenders, this environment presents a favorable opportunity: competitive loan pricing, reduced perceived risk, and continued investor interest in industrial assets. Limited spread headroom for prime deals may push lenders to take on more risk or diversify into other asset classes.

What’s Next

If current trends continue, lenders may need to balance yield compression against growing loan volumes and stable credit performance. With little room left for further spread tightening in low-leverage, high-quality industrial deals, increased activity in moderate or higher LTV lending could emerge. Lenders may shift strategies to maintain returns.

As interest rates stay elevated but relatively stable, spread movement in the coming quarters will be a key indicator of capital market sentiment. It may also signal potential CRE investment momentum heading into 2026.