- Payroll growth slowed in November, with 64,000 jobs added and the unemployment rate rising to 4.6%, the highest since 2021.

- Muted wage growth and labor market softness may dampen renter demand and slow rent growth, particularly in pricier markets.

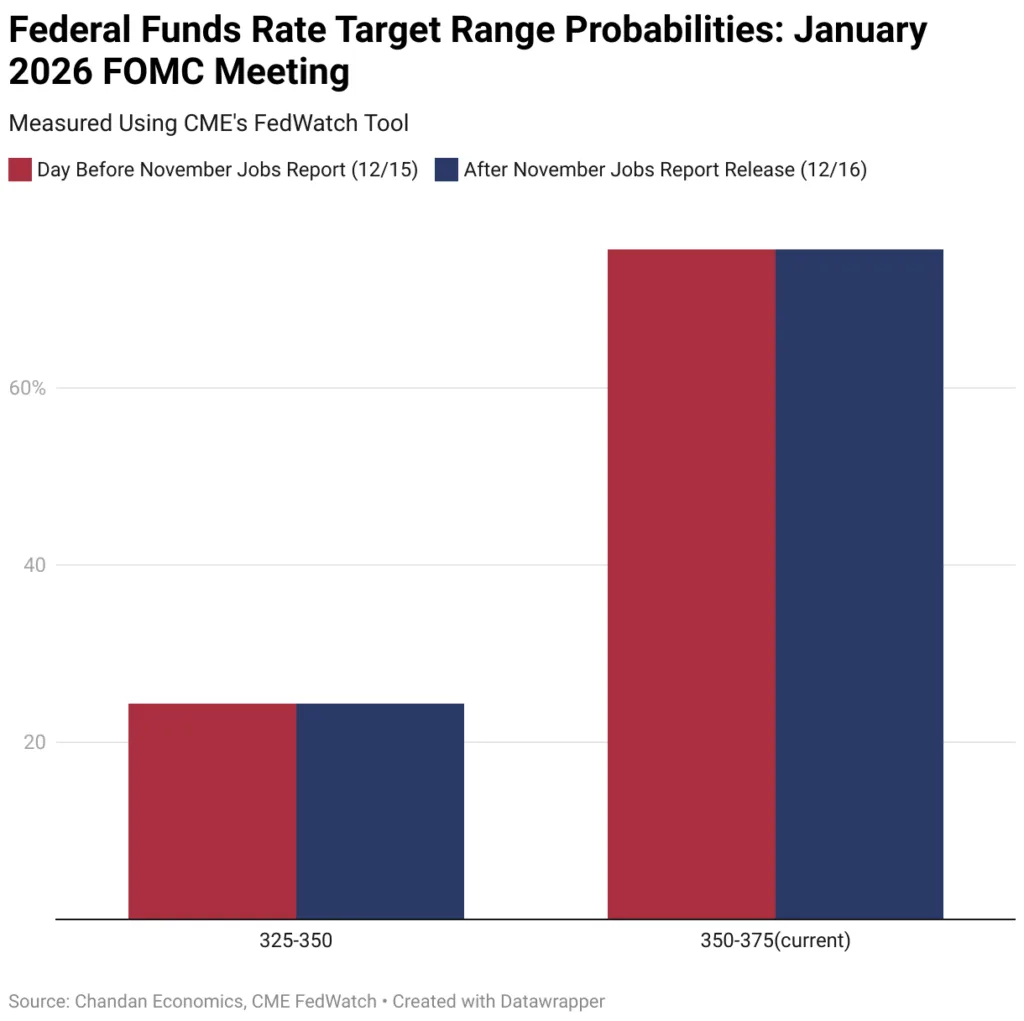

- Fed rate policy remains uncertain, with futures markets showing little confidence in a January cut and no clear consensus on cuts before April 2026.

- Rental housing operators face a mixed outlook, balancing weaker demand with the long-term benefits of prior interest rate cuts still working through the economy.

A Cooling Jobs Market

Chandan Economics reports that the November employment report from the Bureau of Labor Statistics showed that job growth is losing momentum. Employers added 64,000 positions—slightly above forecasts but well below recent monthly averages. The unemployment rate ticked up to 4.6%, and downward revisions to October’s numbers revealed a 105,000 job loss, mainly from government payrolls.

Fed Policy on Pause

Despite the weak jobs data, the futures markets remain cautious. The CME Fed Watch Tool showed no change in expectations for a rate cut in January, holding at a 24.4% probability. Officials at the Federal Reserve appear split between combating persistent inflation and addressing the slowing economy. Markets are currently projecting the next cut no sooner than April 2026, following a trend of slower hiring momentum observed in previous months.

Impact on Rentals

For the rental housing sector, the implications are nuanced. A softening labor market and stagnant wages could limit renters’ ability to move up the quality ladder or absorb higher rents, slowing overall rent growth. While multifamily demand tends to be less sensitive to labor swings than other sectors, continued slack in the labor market could weigh on occupancy and leasing velocity in higher-cost areas.

Looking Ahead

Further rate cuts could eventually ease borrowing costs for both operators and renters, but with no cuts expected in the near term, the industry will likely need to manage through a period of weaker economic tailwinds. All eyes now turn to Thursday’s CPI release, which will help clarify inflation’s direction—and, potentially, the Fed’s next move.

Bottom Line

The November jobs report reinforces a cautious outlook for rental housing as we approach 2026. With labor markets softening and monetary policy on hold, operators should prepare for slower rent growth and heightened renter sensitivity to price in the months ahead.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes