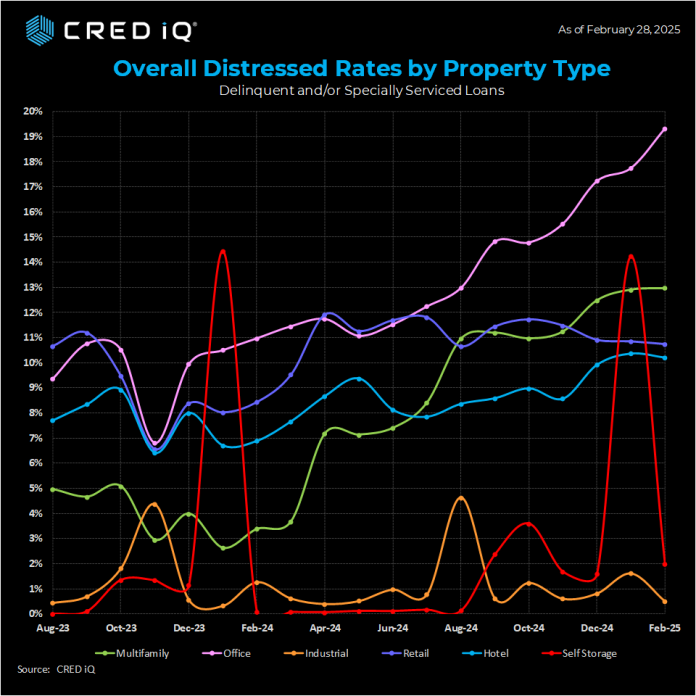

- Loan distress for most property types fell for the first time in five months, dropping by 70 bps to 10.8%.

- Distress in office properties reached a new high of 19.3%, continuing the ongoing downtrend.

- Multifamily, retail, hotel, and industrial reported slightly lower distress, while self-storage saw a sharp drop after a major portfolio deal.

- Factors like varying property classes (A, B, C) and incomplete loan data complicate assessing stress for the overall office sector.

Loan distress across most commercial property types has seen a rare decline in recent months, marking a shift in the cre market, per GlobeSt.

By The Numbers

According to a report from CRED iQ, distress across conduit and single-borrower large loan deal types dropped by 70 bps to 10.8%, the first decrease in five months, which also broke a streak of consecutive record highs.

However, the office sector continues to struggle, with distress hitting a new high of 19.3%.

The term “distress” in this context combines delinquency and specially serviced loan rates. This includes loans at least 30 days delinquent or that have been transferred to special servicers due to financial difficulties.

Sector-Wide Breakdown

Although overall distress was down, not all property types followed the same trend. multifamily distress saw a modest rise, up 40 bps in January and another 10 bps in February, reaching 13.0%.

On the other hand, the retail and hotel sectors saw distress rates drop. Retail fell by 10 bps to 10.7%, while hotel distress dropped 20 bps to 10.2%.

Meanwhile, industrial distress saw a notable decline of 110 bps, falling from 1.6% in January to just 0.5% in February. self-storage also saw a big drop, down from 14.2% in January to just 2% in February. This was largely due to the maturity of a large $2B, 16-property portfolio.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Persistent Problem

Despite the overall decline in distress, offices remain a significant concern. Office distress surged to 19.3%, surpassing previous highs and reflecting the ongoing difficulties in this sector.

Office distress also remains a tale of two asset classes. Data from CBRE on leasing activity in 12 major metro areas shows that Class A and A+ office properties saw rent growth from 2023 to 2024, while Class B and C properties reported rent drops.