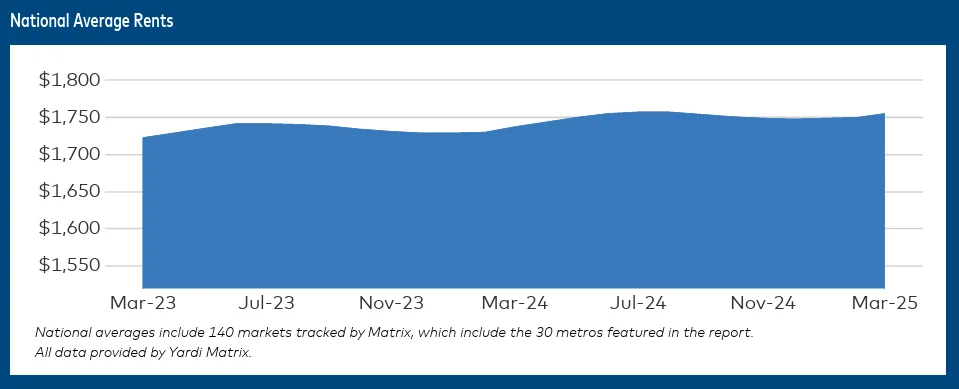

- National multifamily rents rose $5 to $1,755 in March, with annual rent growth easing to 1.0%.

- Renter-by-Necessity (RBN) demand drove performance, up 2.3% YoY, while Lifestyle segment growth lagged.

- Single-family rental (SFR) rates also climbed $5 to $2,169, though YoY rent growth was flat.

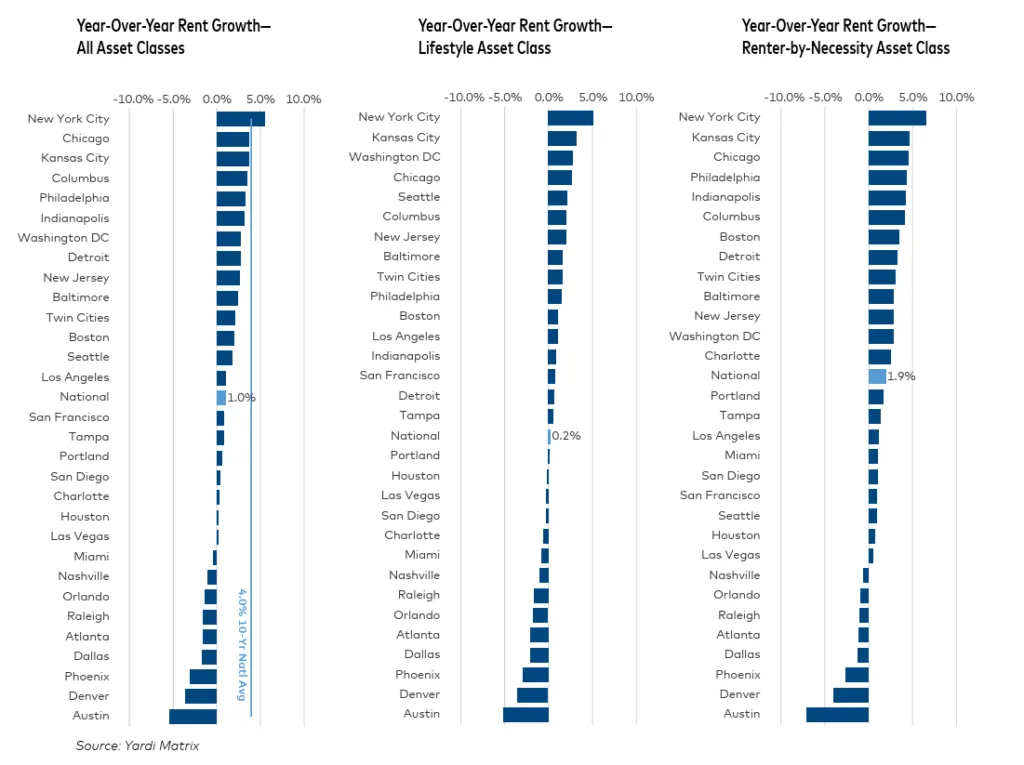

- Gateway markets like New York and Chicago lead the nation in rent growth, while high-supply metros like Austin and Phoenix posted annual rent declines.

- Occupancy held firm at 94.5%, unchanged for three straight months.

- Policy shifts under the Trump administration present both development opportunities and challenges, including cuts to affordable housing programs and potential GSE privatization.

Spring Leasing Kicks Off with Solid Momentum

Multifamily fundamentals remained stable in March, with advertised asking rents climbing $5 nationally, according to Yardi’s National Multifamily Report. Although YoY growth slipped slightly to 1.0%, the market entered the spring leasing season with encouraging signs of resilience. The Renter-by-Necessity (RBN) asset class led performance, up 2.3% YoY, while Lifestyle asset growth came in at just 0.2%.

The SFR sector mirrored multifamily trends, with March rents up $5 to $2,169. Occupancy remained stable at 94.7%, indicating ongoing renter demand amid elevated homeownership costs.

Gateway and Midwest Markets Outperform

Markets like New York City (+5.5%), Chicago (+3.7%), and Kansas City (+3.7%) led annual rent gains, with Northeast and Midwest metros seeing broad-based strength. Conversely, high-supply sun belt markets continued to underperform. Austin (-5.4%), Denver (-3.6%), and Phoenix (-3.0%) all posted notable declines due to aggressive new supply, despite strong absorption metrics.

On the occupancy side, West Coast metros like San Francisco, Los Angeles, and San Diego saw modest YoY increases, aided by low completions and, in some cases, regional disruptions such as wildfires.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Short-Term Momentum Shows Promise

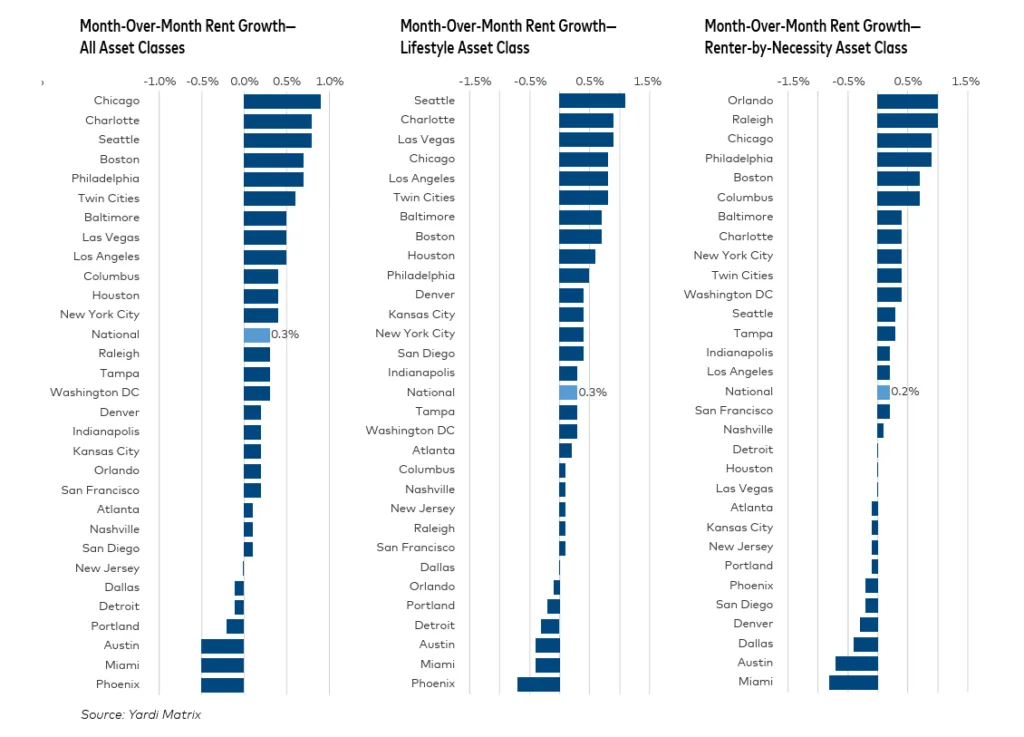

Several metros posted month-over-month rent gains in March, with Charlotte (+0.8%), Chicago (+0.9%), and Seattle (+0.8%) among the top performers. Seattle’s gain is particularly notable, as rents there had stagnated post-pandemic. The rise may reflect major employers tightening return-to-office policies.

However, high-supply metros like Phoenix, Miami, and Austin saw rents fall by 0.5% MoM, highlighting ongoing supply overhangs.

Capital Markets & Policy: New Challenges, New Openings

Although capital remains accessible, a wave of multifamily loan maturities in 2025—many previously extended—could lead to tougher lender stances. This may open opportunities for opportunistic investors to acquire distressed assets or provide refinancing.

Meanwhile, the Trump administration has introduced aggressive housing policy changes. Key initiatives include:

- Proposals to build housing on federal land by streamlining environmental reviews.

- A potential expansion or permanent extension of the Opportunity Zone program.

- Cuts to affordable housing funding, including termination of key hud contracts and a freeze on $1B in Green and Resilient Housing loans.

- Intentions to privatize Fannie Mae and Freddie Mac, raising concerns over multifamily financing stability.

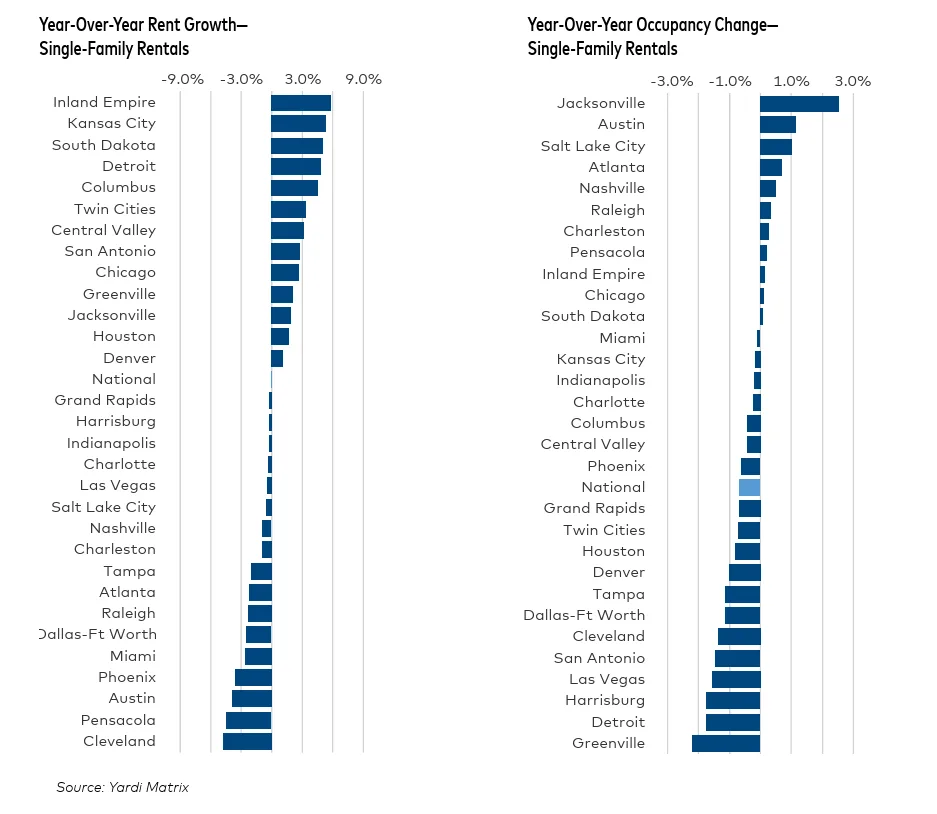

SFR Snapshot: Midwest Leads the Way

Single-family build-to-rent (SFR-BTR) fundamentals remain solid despite a slowdown in rent growth. After peaking at 15% in early 2022, YoY rent growth was flat in March 2025, though average advertised rents rose to $2,169. Occupancy rates stayed stable at 94.7%, with demand holding strong due to the high cost of homeownership.

The Midwest continues to lead SFR rent growth, with over half of the top 10 performing metros located in the region. Notable YoY increases include Kansas City (+5.4%), South Dakota (+5.1%), Detroit (+4.9%), Columbus (+4.5%), Twin Cities (+3.4%), and Chicago (+2.7%).

Why It Matters

Despite economic headwinds—rising layoffs, tariffs, and diminished consumer confidence—the U.S. rental housing market is displaying early resilience in 2025. While short-term rent growth is modest, steady occupancy and continued renter demand, particularly in necessity-driven segments, offer cautious optimism.

However, much depends on how supply-demand dynamics evolve and whether recent federal policy changes accelerate development—or create new hurdles.

What’s Next

- Rent trends are expected to remain stable but vary widely by market, with high-supply metros likely to see continued pressure.

- Policy watchers will monitor the fate of Opportunity Zones, affordable housing programs, and GSE reform for long-term sector implications.

- As loan maturities pick up and capital conditions tighten, 2025 could become a pivotal year for multifamily investment opportunities.