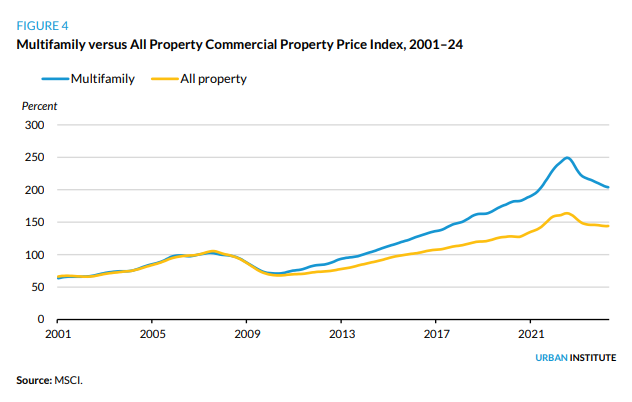

- The total value of US multifamily housing stock has grown from $600B in 1990 to over $6T today.

- Since the 1980s, the multifamily capital markets evolved through four key periods, marked by more liquidity, institutional investment, and government-sponsored enterprises (GSEs).

- Despite challenges, multifamily housing continues to deliver significant supply, outpacing single-family construction and playing a vital role in addressing the US housing shortage.

- Policy efforts to boost capital flows, particularly for affordable and workforce housing, can strengthen multifamily production to combat housing affordability issues.

The multifamily housing market has undergone an incredible transformation over the past 40 years, and is now a cornerstone of the US housing sector.

The total value of US multifamily assets has surged from $600B in 1990 to over $6T today, driven by strong capital markets, higher institutional investment, and flexible rental policies, according to urban.org.

Historical Perspective

The evolution of the US multifamily market occurred across four major periods:

- Late 1980s–Early 1990s: Multifamily markets were regionally fragmented, with small property owners dominating and financing primarily provided by banks and life insurance companies. Liquidity was limited, and institutional investment was scarce.

- Late 1990s–2007: The market consolidated into a national platform, boosted by rising institutional investment, private equity participation, and the growth of CMBS. Multifamily struggled to compete with booming single-family housing but began attracting new capital.

- 2007–2019: Following the GFC, multifamily rebounded. The combo of tighter credit for single-family homes, re-urbanization, and demographic shifts fueled rental demand. GSEs expanded, providing liquidity through innovative programs like Freddie Mac’s K-Deal.

- 2020–Present: The pandemic disrupted multifamily markets briefly, but demand quickly rebounded. Prolonged low interest rates led to skyrocketing property values, while recent rising interest rates have cooled valuations and stressed cash flows.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Multifamily Momentum

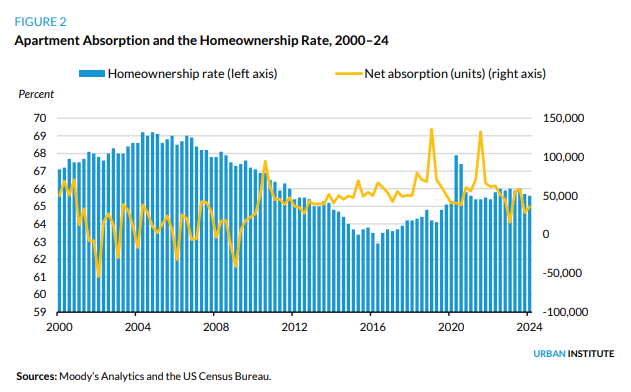

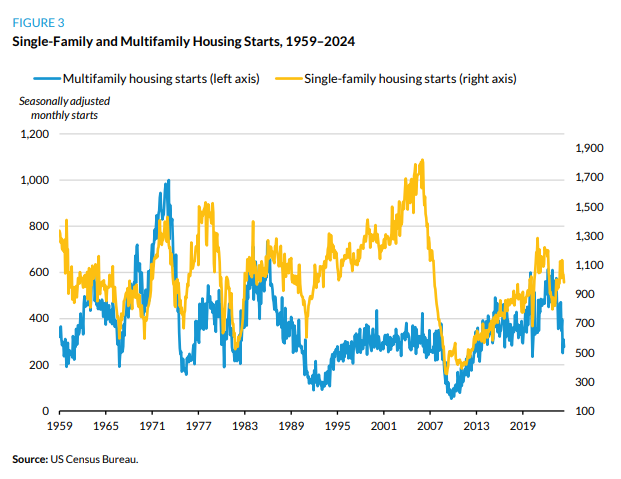

While single-family housing has struggled to recover, multifamily markets have consistently delivered new supply.

In 2022, multifamily housing starts peaked at 530K units annually, representing 1.5% of the multifamily stock—far outpacing single-family growth.

This success stems from three key factors:

- GSE Expansion: Government-sponsored enterprises have played a critical role by providing low-cost, stable financing and building market infrastructure, such as standardized credit terms and data transparency.

- Private Equity Growth: The rise of large-scale private equity real estate funds has boosted liquidity, innovation, and investor participation in the multifamily sector.

- Absence of Rent Regulation: Unlike single-family or global rental markets, the US multifamily sector remains largely free of restrictive rent controls. Regions with minimal regulation, such as the Southeast and Southwest, have seen robust supply growth and rent moderation.

Policy Considerations

The multifamily market is a key driver in addressing the housing affordability crisis by delivering new supply, particularly in high-growth markets.

Recent trends highlight its effectiveness: in 8 of the 10 fastest-growing metro areas, significant multifamily deliveries have pushed rents down, with Class C rents declining by as much as 13.5% in Fort Walton Beach, FL.

However, challenges remain. Rising operating costs, interest rates, and construction financing constraints are slowing new development. To address these barriers, policymakers can strengthen the multifamily sector through targeted interventions:

- Encourage Affordable and Workforce Housing:

- Allow GSEs to offer higher leverage loans or mezzanine debt for workforce and affordable housing projects.

- Integrate federal programs with state and local incentives to support housing preservation and construction.

- Expand Construction Financing:

- Permit GSEs to provide construction-to-permanent loans or noncontingent forward commitments to lower the risk for developers.

- Address current bank lending constraints to ensure capital flows for new multifamily supply.

- Leverage State and Local Programs:

- Support innovative financing programs like Florida’s Live Local Act and other state housing funds for workforce housing.

Looking Ahead

The US multifamily market is a rare success story in addressing the housing shortage, driven by efficient capital markets, institutional investment, and a largely unconstrained rental environment.

While it cannot solve all affordability challenges, the multifamily sector continues to stabilize rents, provide significant new supply, and deliver innovative solutions.

To sustain and build upon this success, policymakers should prioritize measures that enhance capital flows, support affordable housing initiatives, and address development bottlenecks.

A strengthened multifamily market holds the potential to alleviate housing pressures in the US and serve as a model for addressing global housing challenges.