- Rent growth is expected to remain modest at 1.2% nationally in 2026, with Sun Belt markets under the most pressure from oversupply.

- Demand recovery depends on improved job growth, consumer confidence, and immigration policy, all of which remain uncertain.

- New supply is slowing, with 450,000 units forecast to deliver in 2026—a decline, but still elevated compared to historical norms.

- Capital markets are regaining strength as interest rates fall, with investors and lenders returning, though pricing remains cautious.

2026 Begins with Economic Uncertainty

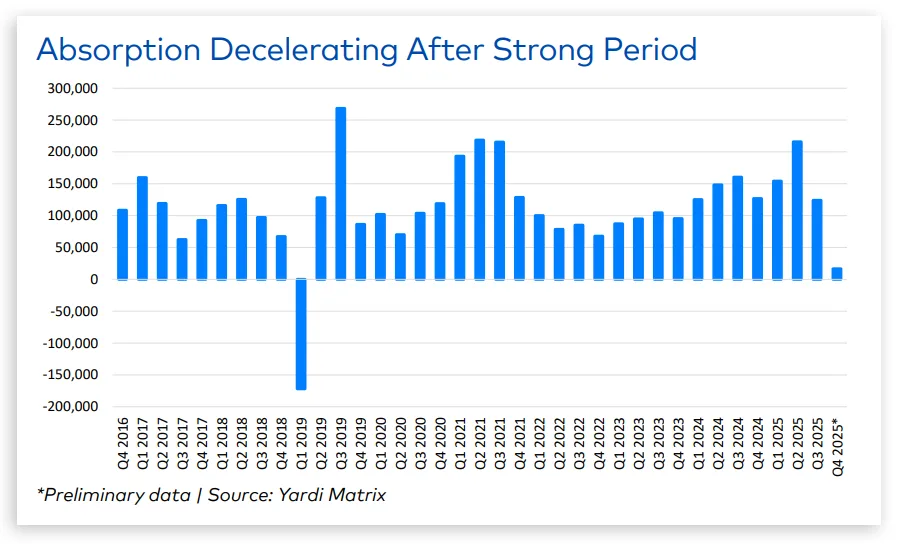

According to Yardi Matrix’s Winter 2026 report, multifamily enters the new year with signs of softening demand. After record absorption in early 2025, momentum slowed dramatically by Q3, with Q4 numbers pointing to further cooling. Job growth has also waned—dropping from an average of 160,000 monthly in 2024 to just 60,000 through most of 2025—leading to concerns about household formation and renter confidence.

While inflation remains above the Fed’s 2% target and policy uncertainty lingers, a new Federal Reserve chair is expected to pursue aggressive rate cuts in 2026. The Fed lowered rates to 3.5% in December 2025, with another 50 basis point cut likely in the new year. However, long-term mortgage rates remain elevated due to federal deficit concerns, limiting the potential for renters to transition to homeownership.

Rents Stay Flat in Oversupplied Markets

Advertised rents were nearly flat in 2025, rising just 0.2% year-over-year through November. Rent growth in 2026 is forecast at 1.2% nationally, held back by ongoing lease-up pressures and softening consumer confidence.

Markets with the steepest rent declines since early 2023:

- Austin: -14.2%

- Phoenix: -9.0%

- Orlando: -5.3%

- Atlanta and Raleigh–Durham: -5.2%

In contrast, cities with constrained supply—such as New York (13.0%), Chicago (10.2%), and Kansas City (9.3%)—led rent gains.

Deliveries to Decline, But Remain Elevated

Construction starts have declined sharply since 2023, following several years of record-setting development activity that brought unprecedented levels of new supply to key metros. Yardi Matrix forecasts 450,000 units will deliver in 2026, down from 595,000 in 2025. While this marks progress toward rebalancing, deliveries remain elevated versus pre-pandemic levels. Key metros with the highest delivery volumes include:

- Dallas: 28,800 units (3.0% of stock)

- Phoenix: 19,900 (4.8%)

- Charlotte: 16,100 (6.4%)

- Austin: 14,600 (4.2%)

- Orlando: 12,350 (4.1%)

New construction starts have declined sharply since 2023. Starts peaked at nearly 708,000 units in 2022, but are projected to finish 2025 closer to 311,000 units. Completions will continue to decline into 2027–2028.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Investor and Lender Appetite Returning

Multifamily investment activity gained momentum in late 2025, with transaction volume up 7.2% year-over-year, totaling $76.1B through November. Capitalization rates have remained stable at 5.7%, and average pricing per unit rose 7.1% to $208,490.

Top metros for deal volume included:

- Phoenix & Dallas: $3.5B each

- Seattle & Miami: $3.4B each

- Atlanta: $3.0B

- Chicago, Boston, LA, NYC, DC, SF: $2.2–$3.1B range

On the debt side, the GSEs are back in force. Fannie Mae and Freddie Mac saw their annual loan caps raised to $88B each for 2026, while life companies, CMBS lenders, and banks are also stepping up loan originations. Delinquencies remain a concern in CMBS (7.1%), but are far lower among banks and agencies.

Looking Ahead: Stability Amid Challenges

Despite weaker fundamentals to start the year, the multifamily sector remains well-positioned for recovery, bolstered by investor confidence, robust debt availability, and declining new construction.

National rent growth is projected to climb back to 2.0% in 2027, and 3.4%–3.8% by 2028.

The sector’s resilience and liquidity continue to make it a favored asset class, particularly in an environment where economic volatility persists.

Bottom Line

While the Sun Belt continues to work through oversupply and national rent growth is restrained, multifamily’s long-term outlook remains favorable. As capital markets thaw and new deliveries taper off, developers and investors should see improving fundamentals by 2027 and beyond.