- Multifamily rent growth was positive in February 2026, but gains were below average for the season.

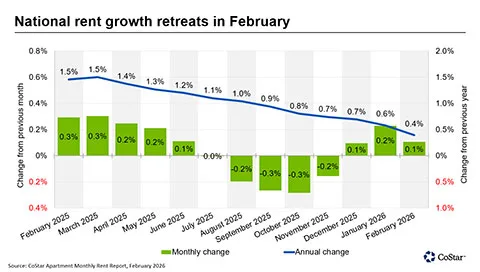

- National average rent increased to $1,716, up 0.1% from December but annual growth eased to 0.4%.

- 38 of the top 50 US metros recorded rent increases; performance varied by region and supply levels.

- Oversupply and soft demand kept growth slow, especially in Sun Belt and select West Coast markets.

National Rent Growth Patterns

According to Apartments.com, US multifamily rent growth continued in February 2026 with a national average increase to $1,716, a 0.1% uptick from December’s revised figure. While positive, this month’s gain is below the February average growth of 0.3% seen from 2010 to 2025. Annual rent growth also slipped to 0.4%, down from 0.6% in January and below the 1.5% rate a year ago.

Market Performance Varies by Metro

Of the 50 largest US metro areas, 38 saw rent increases in February, marking a slight decline from January’s count. Leading month-over-month rent growth were Richmond (+0.8%), San Jose (+0.6%), and Louisville (+0.6%). In contrast, prominent Sun Belt markets such as Nashville (-0.2%), Charlotte, Tampa, Houston, Austin, Orlando, Seattle, and Orange County (all -0.1%) posted declines, reflecting local oversupply and elevated vacancy rates.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Supply and Demand Pressures Continue

Sun Belt and high-construction metros struggled with declining or flat rents as new supply exceeds demand. Meanwhile, San Francisco led on annual growth (+5.7%), with Norfolk, San Jose, and Chicago notching strong gains. Markets like Austin (-5.1% YoY), Denver (-3.4%), and Phoenix (-3.3%) underscore the drag from new construction outpacing leasing activity, even as national data show occupancy levels holding relatively steady in recent months.

What’s Next

February’s uneven rent growth signals a slower pace ahead for multifamily landlords. Elevated inventory and shifting demand continue to weigh on pricing.

Markets with limited new supply should outperform in the coming months. Meanwhile, metros with higher vacancy rates may see rents soften into spring.