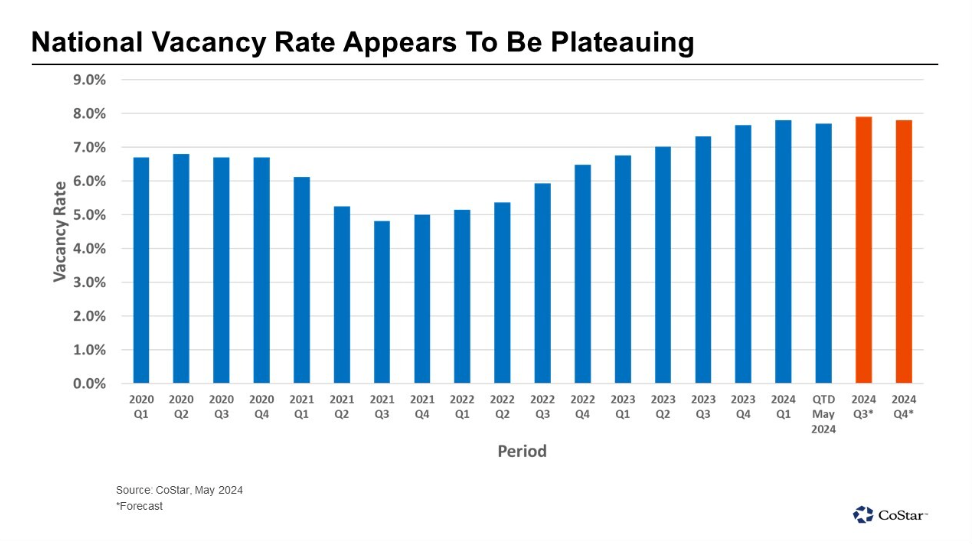

- The U.S. apartment vacancy rate fell slightly to 7.7% in May, showing signs of stability.

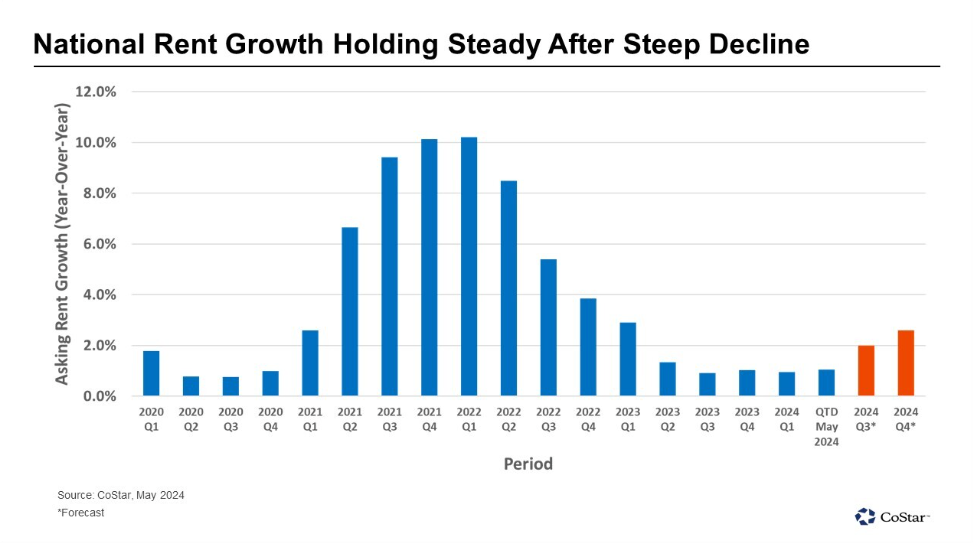

- Rent growth hovers around 1.0% after plummeting from its peak in early 2022.

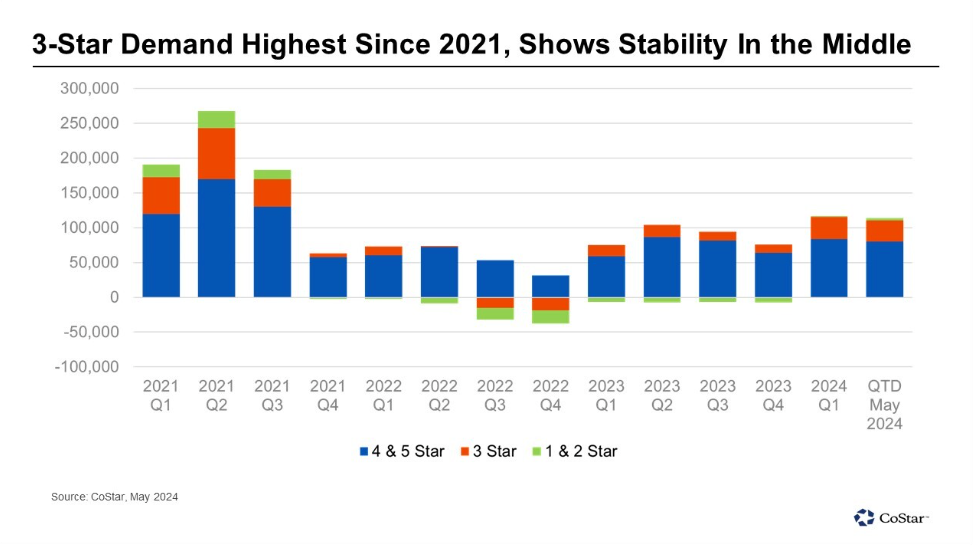

- More demand for 3-star apartments and limited new supply contributed to the sector’s recovery.

Recent data from CoStar indicates multifamily housing is slowly stabilizing after two years of challenges, characterized by record new supply and reduced renter demand. Key indicators, like vacancy rates and rent growth, are beginning to signal a potential recovery.

By The Numbers

At the end of May 2024, the U.S. apartment vacancy rate stood at 7.7%, a hair less than the 7.8% reported in 1Q24. This marginal decrease contrasts with the average 30 bps quarterly increases observed last year.

The apartment vacancy rate rose 10 bps in Q1 and then dropped 10 bps over the next two months. Projections indicate an end-of-year rate of 7.8%.

Limited new supply is also helping. After reaching a 40-year high of 589K units in 2023, apartment supply projections for 2024 are around 528K units, or 10% less. Fewer deliveries should help alleviate the oversupply issue, particularly in Sun Belt markets.

Rent Growth

Apartment rent growth appears to be stabilizing as well. After peaking at an annual growth rate of 10.2% in 1Q22, rent growth slumped over six consecutive quarters, reaching a low of 0.9% in 3Q23. However, rent growth has remained steady since then at 1.1% by the end of May.

Demand Trends

Multifamily demand fell drastically from 700K units in 2021 to 150K in 2022, thanks to deflating consumer confidence, high inflation, recession fears, and geopolitical tensions in Europe.

However, 2023 saw a resurgence in consumer sentiment, bumping multifamily demand up to 325K units. While this wasn’t enough to offset last year’s record-high supply levels, it did mitigate the overall impact of new supply.

Demand for mid-level three-star-rated properties notably contributed to the sector’s recovery, with a turnaround from a negative absorption of 22K units in 2022 to a positive absorption of 57K units in 2023.

This positive trend continued into 2024, with three-star properties accounting for 31K units absorbed in Q1 and an additional 30.5K units in the first two months of Q2, surpassing last year’s total absorption within just five months.

What’s Next?

With consumer confidence on the rise and the pace of new supply additions slowing, these trends suggest a turning point for the multifamily market. Stabilizing rents, lower vacancy rates, and balanced demand and supply signal a potential shift to sustained growth.