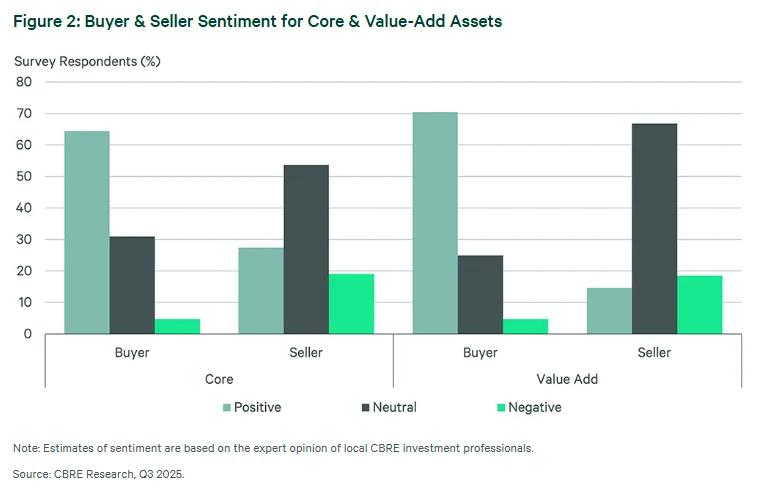

- Buyer sentiment improved in Q3, with 64% of core investors and 70% of value-add investors reporting a positive outlook—up significantly from Q2.

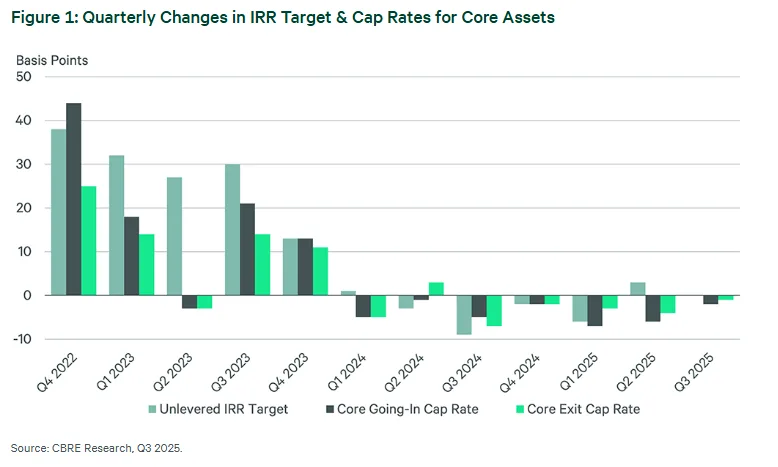

- Cap rates remained relatively stable, with core going-in cap rates down 2 bps to 4.73% and value-add up 3 bps to 5.23%.

- Underwriting assumptions held steady, reflecting cautious optimism despite limited transaction activity.

- Investment volume is expected to rise, supported by easing bond yields, tighter bid-ask spreads, and improving debt liquidity.

Fed’s First Rate Cut Sparks Confidence Shift

Investor sentiment for multifamily acquisitions improved in Q3 following the Fed’s first interest rate cut of the year in September, reports CBRE. While not enough to jumpstart deal flow, the move signaled a potential shift in market conditions and fueled expectations for additional rate reductions in the months ahead.

Core And Value-Add Buyers Turn Bullish

Positive sentiment rose across the board, with core asset buyers reporting a 64% positive outlook, up from 57% in Q2. Value-add sentiment saw an even sharper uptick, climbing to 70% from 62%. Sellers, however, remained more neutral—especially on value-add deals—highlighting an environment still dominated by cautious listing strategies.

The strongest sentiment gains came in Sun Belt markets like Atlanta, Miami, and Nashville, where investor appetite is rebounding amid demographic and job growth tailwinds.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Cap Rates, IRRs Hold Firm

Despite the improving outlook, cap rate movements were modest. Core going-in cap rates declined slightly to 4.73%, while value-add cap rates ticked up to 5.23%. Exit cap rates remained largely flat, and core unlevered IRR targets held at 7.70%.

The spread between going-in and exit cap rates for core assets increased slightly to 22 bps, with CBRE forecasting further widening through 2027—though still below the typical 50-60 bps range.

IRR targets remained stable in most markets, with notable shifts in a few metros:

- Chicago and Nashville saw modest IRR declines.

- Austin and Dallas recorded slight increases.

What’s Next

Underwriting assumptions largely held steady in Q3. Annual rent growth estimates remained at 2.8% for core assets and dipped to 3.2% for value-add. Despite this, investors appear more willing to pursue deals heading into Q4. The combination of lower interest rates, more aggressive bidding, and a narrowing bid-ask spread could push more multifamily assets onto the market in late 2025 and early 2026.

As financing conditions improve, CBRE anticipates a pickup in transaction volume, particularly for well-located properties in high-growth markets.

Bottom Line

Multifamily investors are regaining confidence as macroeconomic conditions begin to shift. While many underwriting fundamentals remain unchanged, a more optimistic buyer pool and improving capital markets could finally catalyze the long-anticipated thaw in deal activity.