- Open-air neighborhood shopping centers, particularly those with grocery stores as main tenants, are seeing rising occupancy and investor interest.

- Institutional investors like Blackstone are spending billions on shopping center portfolios, capitalizing on the scarcity of retail space and rising demand.

- Despite the retail revival, building new shopping centers remains limited due to rising construction costs, leading to higher rents.

- The focus for now is on u0022unflashyu0022 retail hubs, rather than high-end malls, with investors wary of the continued threat of online competition.

After a decade of being overshadowed by e-commerce and warehouse real estate, neighborhood shopping centers are back on the radar of institutional investors.

This recent trend, fueled by rising foot traffic and a supply shortage, marks a shift away from the glitzy, high-end malls of the past and toward more modest, everyday retail hubs.

National Retail Revival

As e-commerce grew, many retail properties—especially regional malls—struggled to survive. The pandemic further disrupted shopping habits, pushing shoppers online and leaving many old-school brands in the dust.

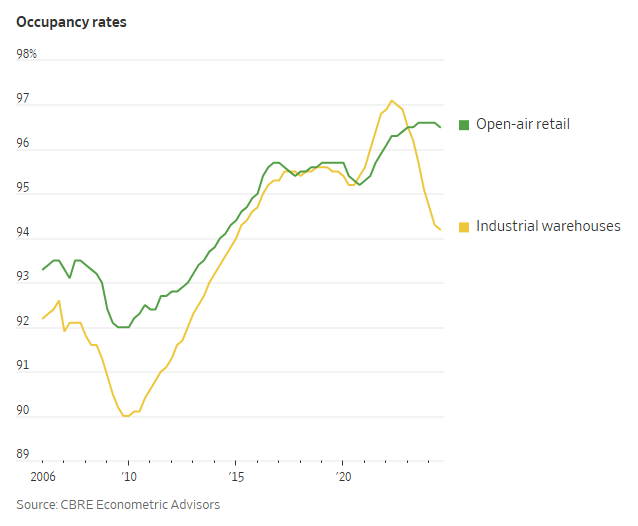

But in recent years, open-air neighborhood centers have quietly emerged as the unexpected winners. These local shopping hubs, many anchored by grocery stores and small businesses, are seeing rising occupancy rates—higher than industrial warehouses, according to CBRE. And they’re attracting attention from major players like Blackstone (BX).

Grocery stores, in particular, have seen a notable uptick in foot traffic. In fact, grocery store visits in Q3 were 12% higher compared to the same period in 2019.

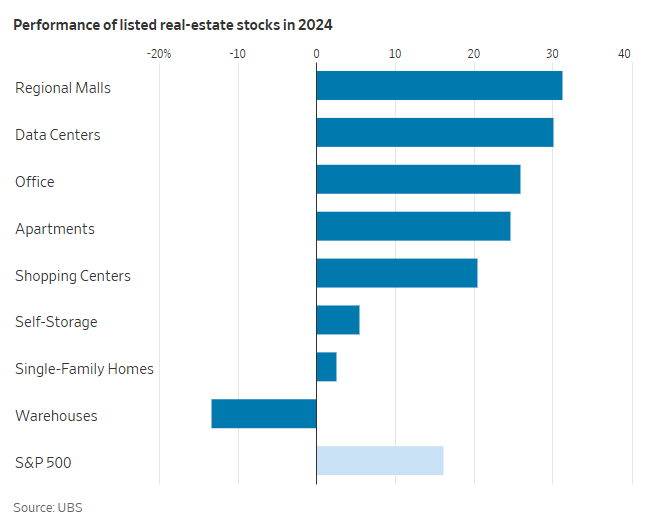

Not to mention that, as a whole, publicly traded regional mall stocks outperformed even data centers, delivering over 30% returns in 2024.

Unsurprisingly, this rebound has caught the attention of many institutional investors.

In November, Blackstone made its largest US retail purchase in more than a decade, spending $4B to acquire shopping center owner Retail Opportunity Investments. Other firms like Bain Capital are also showing interest, signaling a return of confidence in US retail.

Limited Supply Squeeze

One reason for the renewed interest in open-air centers is the lack of new supply. Over the past decade, construction of retail centers has slowed dramatically, with new supply up by just 0.5% annually—far below the historic average of 2.5%.

Meanwhile, demand has stayed strong, making existing properties even more valuable. The rise in construction costs, driven by inflation and supply chain snarls, makes building new centers far less appealing.

For investors, buying existing retail properties has become the more cost-effective option. As a result, open-air shopping centers are in a prime position to benefit from rising rents and stable, long-term leases.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

All in The Neighborhood

The appeal of these retail hubs lies in their mix of tenants and lifestyle-driven demand. Grocery stores serve as anchors, attracting consistent foot traffic.

But coffee shops, nail salons, yoga studios, and medical centers will also always have customers. These types of businesses are either immune to e-commerce competition or simply more difficult to replicate online.

Flexible work schedules have also made local shopping more convenient. With more white-collar workers spending part of their week at home, visits to local centers during lunch breaks or after work have become routine.

As James Corl from Cohen & Steers notes, “This is where America shops now.” For investors, the combination of steady demand, limited supply, and rising rents makes these neighborhood shopping centers a safe bet.

Future of Retail

Despite the bullish outlook for open-air shopping centers, the overall retail real estate market is not without risks.

High-end enclosed malls, still struggling with online competition, remain off-limits for most institutional investors. Their continued reliance on costly overheads like air conditioning and high tenant incentives makes them a less attractive option.

It’s estimated that at least $10B worth of open-air retail portfolios will change hands in 2025, and lending conditions have recently improved, fueling momentum.

With modest rent increases projected (3% to 4% annually), neighborhood shopping centers will remain a steady, income-generating option for investors seeking stability. With a new administration potentially taking office in 2025, some experts express concern that higher tariffs and tax cuts could reignite inflationary pressures.

For instance, proposals for tariffs on goods from Canada, Mexico, and China could drive up construction costs, further contributing to inflation.

Not Out of The Woods Yet

While the Fed’s rate cuts signal that inflation is under control, the persistence of high long-term yields and concerns over future inflationary pressures make it clear that CRE professionals will face ongoing challenges this year.

The relationship between the 10-year Treasury yield, the Fed’s actions, and real estate valuations will continue to shape the market, with uncertainty and volatility likely to persist.

Although the tariff landscape may change, they’re betting that the broader forces of nearshoring, cross-border trade agreements, and improved infrastructure will continue to outweigh the risks.