- Office distress is accelerating, with 25M SF in distress in 2024 — a 39% increase over the prior three-year average.rn

- Vacancy rates climbed to 19.8% nationally, with office utilization stuck at 54%, underscoring the long-term impact of remote work.rn

- Large urban properties and CBD assets are leading distress metrics, while suburban markets remain more stable.rn

- Construction has plummeted, with starts down 50% year-over-year in 2024, giving the market time to recalibrate.

Distress Accelerates as Office Demand Stagnates

The long-anticipated wave of office market distress is taking shape. According to Yardi Matrix, 2024 saw 25M SF of office properties hit distress, up sharply from the previous three-year average of 18M. Nearly 11% of all office transactions were classified as distressed last year, and average asset size in these deals climbed above 200,000 SF — pointing to a crisis disproportionately impacting large office assets in dense urban centers.

Central business districts saw distressed deals triple year-over-year, while urban properties nearly doubled. Suburban properties remained more resilient, making up half of all distress, but with less growth in volume.

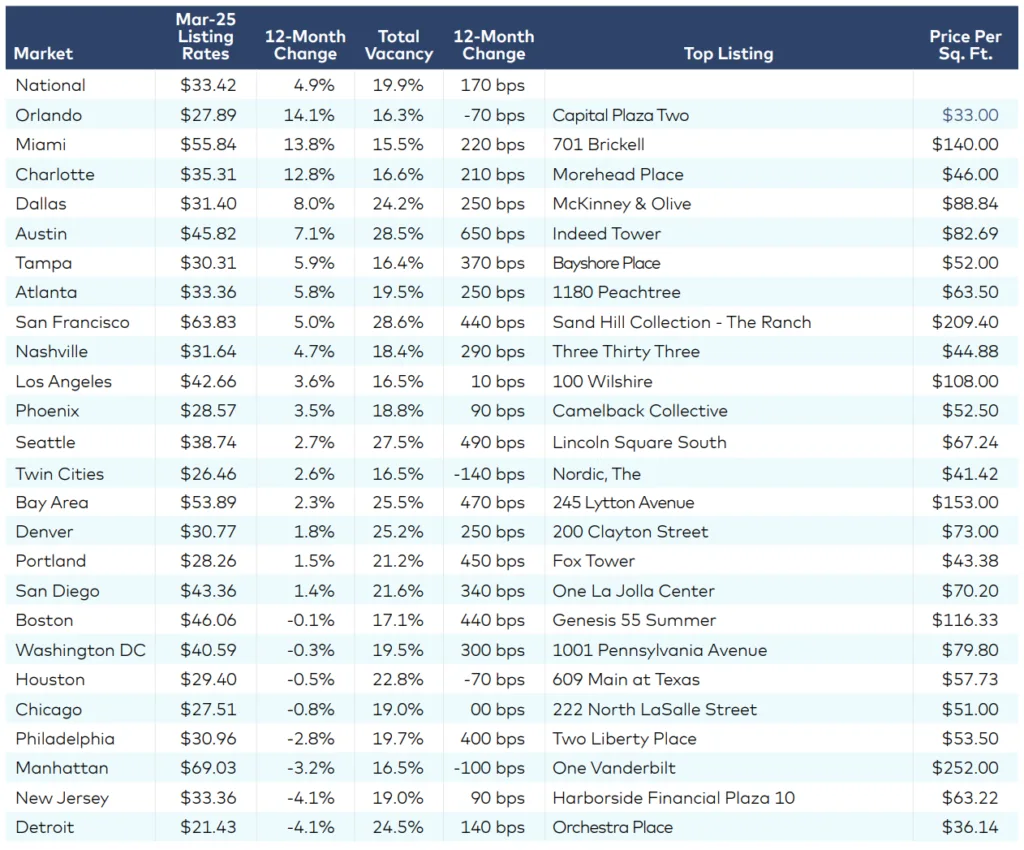

Office Attendance and Vacancy Stagnate

Utilization continues to lag. According to Kastle’s Back to Work Barometer, office attendance has flatlined at 54% since 2023. The national vacancy rate rose by 150 basis points in 2024 to 19.8%, and ticked up again in March to 19.9%. The remote and hybrid work culture that surged during the pandemic appears firmly entrenched.

This stagnation feeds directly into rising office distress, particularly in tech-heavy markets. Cities like San Francisco (28.6%), Austin (28.5%), and Seattle (27.5%) face outsized challenges as remote-friendly tech firms continue to downsize.

Schaumburg Towers: A Case Study in Decline

Chicago saw the most office distress transactions in 2024, with 26 recorded. One of the largest, Schaumburg Towers, exemplifies the market’s current turmoil. The 882,071 SF suburban office complex sold at auction for $74M— 15% below its 2018 price.

This distressed sale, following foreclosure by Prime Finance, highlights how office distress is eroding asset values, even for sizable suburban properties. Chicago’s trend of growing property size in distressed deals is consistent with national patterns.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Silver Linings and Sector Reset

Despite near-term struggles, a longer-term correction may offer opportunity. Office starts fell to 12M SF in 2024, down from 25M in 2023, offering some relief by slowing new supply. As under-construction volume drops, owners and investors may find firmer footing.

One bright spot is the Financial Activities sector, which added 9,000 jobs in March and has seen modest growth over the past two years. However, this is offset by continued losses in Professional and Business Services and Information sectors.

West Palm Beach: A Rare Growth Market

While national supply contracts, West Palm Beach stands out. The city leads the nation in office starts in 2025, accounting for more than half of new development to date. Related Ross broke ground on two new towers in March, together adding nearly 1M SF to the downtown core, reflecting Florida’s ongoing business migration trend.

Transaction Activity: Sales Rebound in Select Markets

Office sales totaled $10.3B through Q1 2025. While the national average price per square foot was $183, premium assets in markets like San Diego ($665 PSF) and Manhattan ($439PSF) skew the average. Washington, D.C. logged $767M in sales, the second-highest nationally, including the $153M sale of The Victor, which traded below its 2005 valuation despite being priced well above the market average.

What’s Next

Office distress isn’t likely to disappear in 2025. Structural shifts in how we work are redefining demand for office space, especially for large, centralized assets. With construction at historic lows and vacancy still climbing in many metros, the sector faces a long road to recovery.

Still, this period of realignment could open the door to creative repositioning, conversions, and investor opportunity as prices reset and outdated assets are reimagined for new uses.