- High-dollar commercial real estate prices are rising again in major metros, while lower-cost property values in smaller markets are falling.

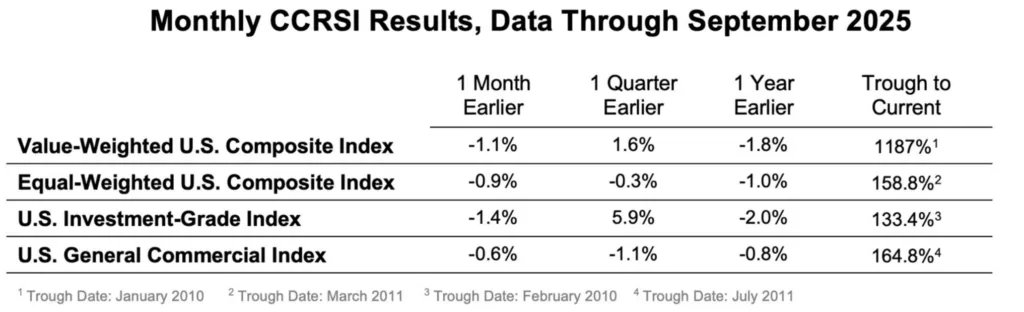

- Value-weighted prices for large deals gained 1.6% in Q3 2025, driven by rising investor confidence and interest rate cuts.

- Equal-weighted prices, tied to smaller assets, declined for the third time in four quarters — their first annual drop in over a decade.

- Industrial and multifamily sectors led pricing gains, while office and retail assets in secondary markets continued to lose value.

Institutional Investors Drive a Market Rebound — But Only at the Top

The latest data from CoStar’s Commercial Repeat Sale Indices (CCRSI) shows a growing divide in US commercial property pricing. While large, high-value deals are regaining ground, smaller assets in regional markets are faltering.

In Q3 2025, the value-weighted US Composite Index, which tracks institutional-grade, high-priced sales, rose 1.6% quarter-over-quarter — marking the second straight quarterly increase. Meanwhile, the equal-weighted US Composite Index, reflecting more numerous, smaller-dollar trades, fell 0.3% and is down 1% year-over-year — its first annual decline since 2012.

The return of big money comes as the Federal Reserve has cut rates twice since September, easing borrowing costs and pushing large investors back into the market. However, activity in smaller markets is cooling, as individual investors grow more cautious in the face of uncertain fundamentals.

“The private capital segment appears to be losing its multiyear outperformance over institutionally sized deals,” said Chad Littell, CoStar’s national director of capital markets analytics.

Winners and Losers: Sector Performance Splits

- Industrial assets remained the top performer in both indices. Equal-weighted industrial prices rose 1.3% quarterly and 2.4% year-over-year.

- Multifamily followed closely, gaining 1.2% quarterly and 2.2% annually, with smaller properties leading the growth.

- Retail prices in lower-tier markets struggled the most, down 2.1% quarter-over-quarter and 2.6% year-over-year in the equal-weighted index. However, value-weighted retail prices ticked up 1.7% quarterly.

- Office remains bifurcated: value-weighted office pricing rose 1.8% in Q3 — the first annual gain since Q2 2022 — but equal-weighted office prices declined 1.8% quarterly and 2% annually.

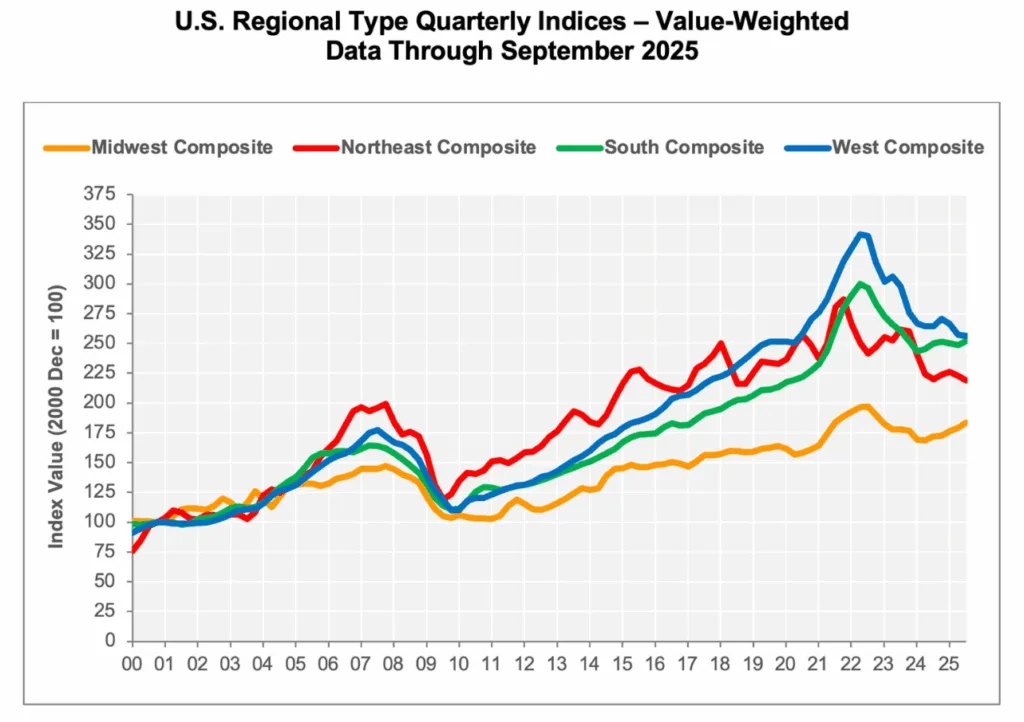

Regional Breakdown: Midwest and West Lead Declines

Smaller property values slid across most US regions, particularly in the Midwest, where the equal-weighted index fell 2.3% quarterly and annually. In the West, equal-weighted prices dropped 1.3%, and value-weighted fell 0.4%, signaling broader weakness.

In contrast, the South offered some balance: equal-weighted prices dipped 1.4%, but property types like office (+2.1%), industrial (+1.2%), and multifamily (+0.6%) posted quarterly gains. Retail, however, declined 2% in the region.

Why It Matters: A Decoupled Market Creates Opportunity and Risk

The widening price gap underscores a structural shift in the CRE market. With large deals once again commanding attention — and premiums — smaller properties are losing momentum. While this decoupling may be temporary, it reflects a risk-reward recalibration among buyers and lenders alike.

Equal-weighted indices, often a proxy for regional economic activity and private investment sentiment, now show their first annual dip in 12+ years. That’s a warning sign for smaller investors and markets reliant on local capital.

What’s Next: Rate Cuts Fuel Hope, But Recovery Is Uneven

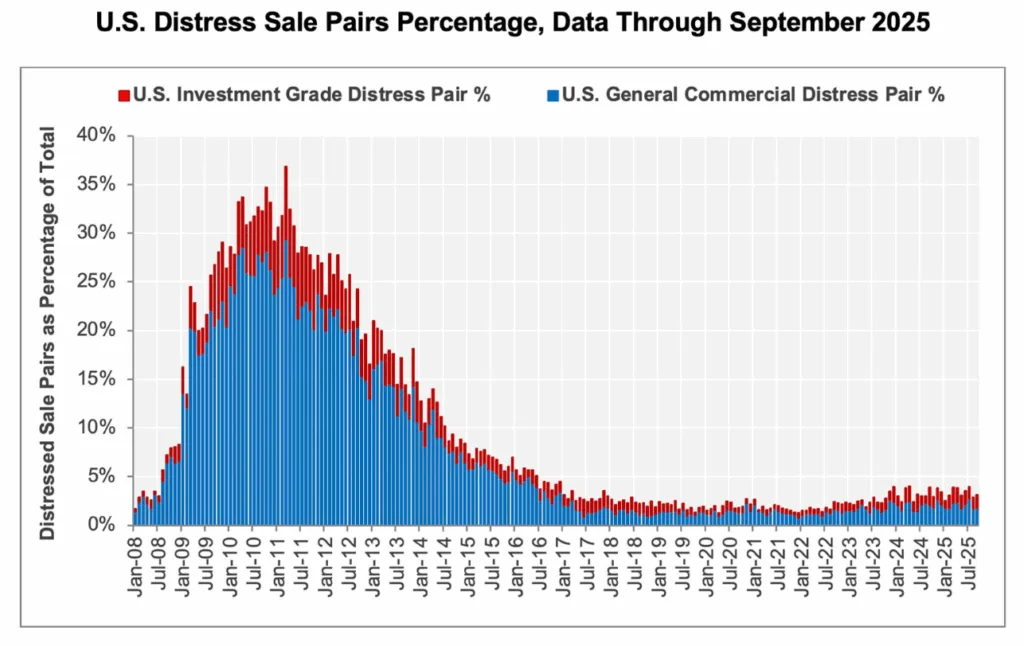

Repeat sales volume is still down year-over-year by 6.9%. However, total transaction volume rose 25.4% over the past 12 months. The increase was driven largely by institutional-grade deals, signaling that big players are preparing for a rebound.

As borrowing costs ease and fundamentals stabilize, more buyers may return to the sidelines. But for now, the decoupling between big and small assets looks set to continue, with investor appetite focused squarely on stabilized, high-quality properties in core markets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes