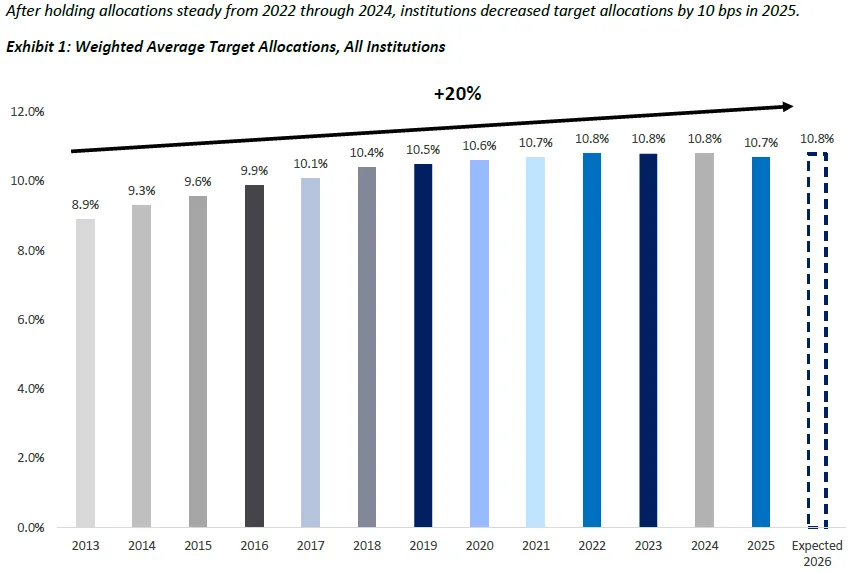

- Institutional investors trimmed target allocations to real estate in 2025 by 10 basis points to 10.7%, ending a decade-long trend of steady or rising commitments to the sector.

- Market uncertainty and increased competition from infrastructure and private credit are prompting capital to shift toward other asset classes.

- Despite the pullback, conviction is rising, and allocations are expected to rebound in 2026, signaling cautious optimism for CRE’s long-term role in institutional portfolios.

A Historic First

For the first time in its 13-year history, the Hodes Weill & Cornell University Institutional Real Estate Allocations Monitor recorded a decrease in institutional investors’ target allocations to real estate.

After three years of stability at 10.8%, the average target slipped to 10.7% in 2025—a modest 10 basis point dip, but a symbolic break from a decade-long growth trend.

What’s Driving the Shift?

The dip stems from two main pressures: macroeconomic uncertainty and asset class competition. Institutional investors cited continued volatility in valuations, interest rates, and transaction volumes as reasons to be cautious about further CRE commitments. Meanwhile, private credit and infrastructure are gaining favor. Target allocations to infrastructure rose 40 basis points to 5.9% in 2025—marking a significant rebalancing trend in institutional portfolios.

Who’s Cutting—and Who’s Not

Allocation moves varied across institutions. Notable increases came from the New York State Common Retirement Fund (+300 bps to 12%) and Ohio’s Teachers’ Retirement System (+200 bps to 10%). But others, like Maryland and Oklahoma’s pension systems, trimmed their allocations by 100 to 200 bps. On balance, small institutions reduced exposure more significantly than large ones.

Underallocated and Waiting

Institutions are also underweight real estate relative to their own targets. Actual allocations fell to 9.8% in 2025, creating a 90 basis point gap from the 10.7% target—the widest underallocation margin in a decade. This shortfall, driven by muted returns, limited distributions, and rising public equity values, signals potential pent-up demand once capital market conditions stabilize.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Looking Ahead

Despite the pullback, sentiment toward CRE is stabilizing. The 2025 Conviction Index rose slightly to 6.4, near its all-time high. With clearer expectations on rate cuts and easing inflation, 21% of institutions plan to raise real estate targets in 2026—up from just 13% last year. That would bring the average back to 10.8%.

Investors are favoring core and core-plus strategies, signaling a flight to quality and a belief that asset values may have bottomed.

Why It Matters

The CRE sector is facing both a moment of caution and a potential inflection point. While current allocations may be under pressure from competing sectors, real estate remains a key part of the institutional portfolio playbook. The 2025 report notes that “real estate remains a key ballast,” offering income, diversification, and long-term inflation protection.

What’s Next

Expect institutions to approach real estate with a “slow but steady” strategy. If macro conditions continue to improve and distributions pick up, capital deployment may accelerate again in 2026, particularly into sectors like housing, logistics, and digital infrastructure that align with broader real asset themes.