- More small regional banks are modifying their CRE loans. Modifications jumped from 0.1% in early 2024 to 0.32% by Q3.

- Regional banks are particularly vulnerable due to lower down payments on office loans, leaving them with thin buffers amid falling property values.

- Approximately $500B in CRE mortgages will mature in 2025, with a significant portion expected to default, fueling fire sales and further price drops.

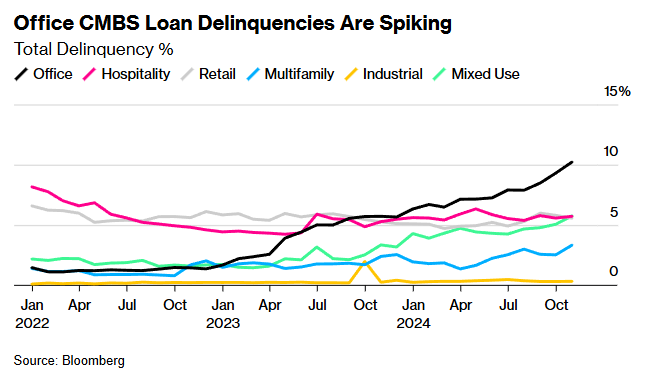

- Smaller bank stock underperformance and rising CRE loan delinquencies point to prolonged challenges, compounded by high borrowing costs despite Fed rate cuts.

Falling office property values are creating ripple effects in the banking sector, with more small regional lenders resorting to CRE loan modifications.

These modifications, often sought by struggling landlords seeking payment extensions, signal rising distress as a wave of loans comes due for refinancing, as reported by Bloomberg.

By The Numbers

While medium and large banks modified 1.93% and 0.79% of their loans respectively, smaller banks lagged at 0.32%.

Moody’s Ratings suggests that this discrepancy highlights a slower adjustment to declining asset values rather than superior lending practices.

Regional Banking Risks

Regional banks are more exposed due to their history of issuing loans with lower down payments, which offer less protection against declining office property values. Office and apartment complex values have fallen over 20% from their peak, eroding the buffer many lenders rely on.

Adding to the strain, smaller banks are not subject to the same rigorous stress tests as their larger counterparts. Consequently, they have set aside fewer reserves for potential loan losses.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Refinancing Wave

Over $500B in CRE mortgages will mature in the coming year, with a significant share expected to default. This impending wave of defaults is likely to trigger fire sales of commercial properties, driving prices even lower.

As FDIC Chairman Martin Gruenberg warned, weaknesses in office and multifamily loan portfolios warrant close monitoring, especially at smaller institutions.

Persistent Headwinds

Rising office loan delinquencies and stagnant long-term borrowing costs are squeezing landlords’ ability to refinance debt. This dynamic is forcing some lenders to avoid taking ownership of distressed properties to sidestep further markdowns.

“Borrowers who aren’t making payments can’t extend forever,” said Robin Potts, Chief Investment Officer at Canyon Partners’ real estate unit.

Looking Ahead

As CRE enters 2025, the pressure on regional banks and public mortgage REITs is expected to intensify.

Industry experts predict that falling asset prices and maturing loans will lead to a prolonged period of defaults and fire sales, with smaller banks bearing the brunt of the crisis.