- CPI rose 0.3% in June, while Core CPI increased 0.2%, driven by tariff-affected categories like appliances and apparel; vehicle and airfare prices declined.

- Shelter inflation continues to cool, down to 3.8% year-over-year, supporting affordability and acting as a counterweight to other inflationary pressures.

- Rate cut expectations for July declined further, with futures markets now pricing just a 2.6% chance of Fed action this month.

- Rental demand remains resilient, sustained by high mortgage rates and declining homebuilder confidence, but growing affordability concerns are emerging.

A Mixed Bag on Inflation

Chandan Economics reports that in June 2025, US consumer prices edged up by 0.3%, pushing the annual inflation rate to 2.7%, according to the latest Consumer Price Index (CPI) report. Core CPI, which excludes food and energy, rose 0.2% monthly and 2.9% annually—modest, but signaling renewed pricing pressures, even as rent inflation continues to cool.

Key drivers included a 1.9% monthly jump in appliance prices and a 0.4% rise in apparel—categories closely linked to recently enacted tariffs. Conversely, prices for vehicles and airfares moved lower.

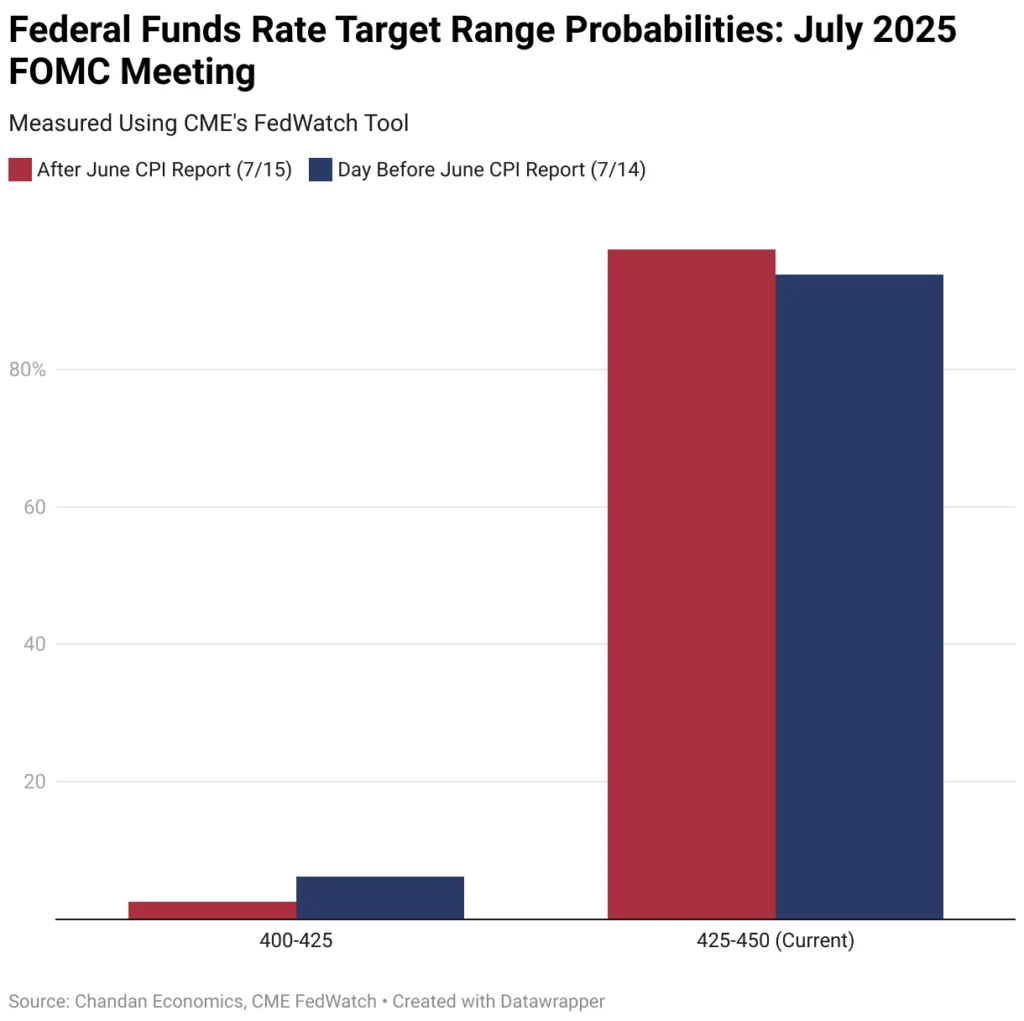

Interest Rates: Little Movement, Growing Divergence

Despite the modest inflation uptick, the market’s rate expectations remain largely unchanged. Futures data from the CME Fed Watch Tool showed a 93.8% chance of no change in rates before the CPI release. Post-report, that probability inched even higher to 97.4%, virtually eliminating hopes for a July cut.

Longer-term expectations did shift slightly. The likelihood of two or more cuts by year-end fell from 71.2% to 62.8%, reflecting the market’s cautious outlook and mixed signals from the Federal Open Market Committee (FOMC). Policymaker views are splitting—some see tariff-related inflation as temporary, while others want more data before acting.

Rental Housing Outlook: Demand Stable, Affordability at Risk

Shelter inflation, a major component of CPI, continued to decelerate in June—now at 3.8% year-over-year, down from a post-COVID peak of 8.8% in March 2023. This marks the 25th monthly decline in the past 27 months, thanks to a historic surge in apartment and build-to-rent (BTR) completions.

While CPI’s methodology (which lags and overrepresents renewals) shows moderate rent inflation, private sector data suggests even cooler conditions in new lease rates—indicating that CPI’s shelter measure should continue easing.

The cooling shelter index is significant: it comprises nearly one-third of CPI’s total weighting, and its ongoing moderation may help offset broader inflation risks, including tariffs.

At the same time, homebuying remains stalled. Builders, constrained by costs and market uncertainty, are offering more incentives and slowing land acquisition. The result: prolonged rental demand and potential income stability for multifamily investors.

However, affordability challenges are growing. On-time rent payments have dropped four percentage points since April 2023, according to the Chandan Economics-RentRedi Rent Collections Report. If wage or employment growth slows, these issues could worsen—potentially spilling over into housing and dampening renter stability.

The Bottom Line

The June 2025 CPI report reinforces the current “wait-and-see” stance from the Fed, while offering encouraging signs for multifamily investors as rent inflation cools and rental demand remains firm. But with affordability tightening and economic headwinds growing, the rental housing sector may soon be navigating a more complex landscape—especially if interest rate relief arrives slower than expected.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes