- Shelter inflation, CPI’s largest component, is slowing rapidly as rent growth drops below 3%

- A historic apartment supply boom is suppressing rents, with effects lagging into CPI

- Rent’s CPI impact will likely prevent a major inflation rebound until at least 2027

The Real Story Behind the CPI Drop

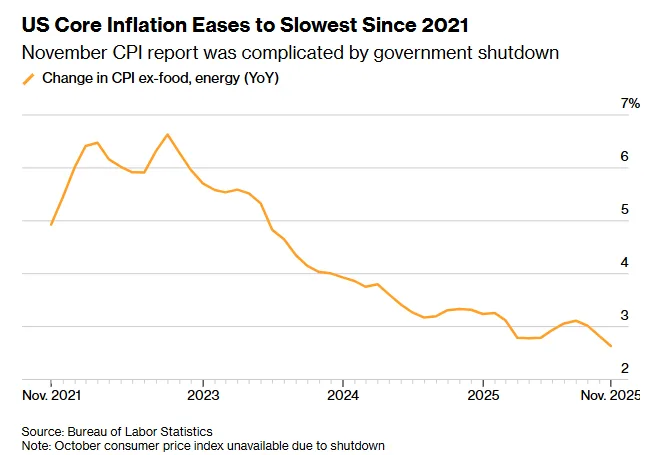

Thursday’s inflation report surprised markets: core CPI fell to 2.6%, and overall CPI eased to 2.7%—its slowest annual rise since early 2021. Much of the media attention has focused on short-term data complications due to the October government shutdown, but that’s obscuring a bigger, more structural story.

The real reason inflation is easing—and staying lower—is shelter, specifically rent.

Why Shelter Matters So Much in CPI

Shelter accounts for roughly one-third of the CPI index, making it the most influential category in the inflation calculation. And within shelter, the metrics “Rent of Primary Residence” and “Owners’ Equivalent Rent” dominate.

Both are based on a monthly survey of around 7,000 renters, and the data flows into CPI on a lagged basis, which made inflation “stickier” on the way down. That same lag now makes CPI resistant to any rapid re-acceleration—like a semi truck slowly descending a hill with its brakes on.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Rent Inflation Is Now Clearly Cooling

According to the latest CPI data, shelter inflation is down to 3% year-over-year, the lowest since August 2021. But even that lags behind what’s happening in real-time.

Market-based rent data—from sources like Zillow, Apartment List, and RealPage—show national rents are flat or even declining. And based on current trends, CPI shelter inflation will keep drifting lower through 2026.

Why Rent is Falling: Supply Surge Meets Softer Demand

The U.S. just experienced the biggest apartment construction boom in 50 years. Hundreds of thousands of new units have entered the market, overwhelming even strong post-pandemic demand.

Many of those units are still in lease-up phases and will take time to absorb, keeping downward pressure on rents. This surge in supply won’t fully taper off until 2026, meaning the CPI won’t show any rent re-acceleration until at least 2027, and more likely 2028, given the lag in how rent data feeds into inflation metrics.

What It Means for Policy and Markets

This rent dynamic gives the Federal Reserve a longer runway. Despite the noise in today’s CPI numbers—complicated by delayed data collection and seasonal adjustments—the underlying shelter trend is clear: there’s a structural cap on how high inflation can run in the near future.

While other categories like goods or services may fluctuate, shelter’s size in the CPI basket makes it a powerful disinflationary force.

What’s Next

The Fed is closely watching CPI, and while some policymakers remain cautious, falling shelter inflation increases the likelihood of rate cuts in 2026. The key: housing costs aren’t just a drag on CPI today—they’re poised to keep it grounded for years to come.

Bottom line: Rent isn’t just cooling. It’s the silent anchor keeping inflation from drifting back up—and it’s not going anywhere fast.