- August’s CPI rose 0.4% month-over-month and 2.9% year-over-year, slightly higher than July’s figures but in line with expectations.

- Core CPI remained steady at 3.1% annually, reinforcing a consistent inflation trend the Fed closely watches.

- Despite the CPI uptick, deteriorating labor market data continues to push the Fed toward rate cuts—potentially as soon as the next meeting.

- A more dovish rate outlook is good news for the rental housing sector, which has been struggling under the weight of elevated borrowing costs.

Inflation Still Running Warm — But Not Hot Enough To Stop Rate Cuts

August’s inflation report showed a modest rise in consumer prices, reports Chandan. The Consumer Price Index (CPI) increased by 0.4% month-over-month. On a year-over-year basis, CPI rose by 2.9%. Core CPI, which excludes volatile food and energy prices, remained unchanged at 3.1%. This suggests that underlying inflation is stable.

The numbers were slightly above July’s pace but came in close to market expectations, easing fears of a major inflation rebound. That consistency could be just enough to keep the Federal Reserve on course to cut rates in the coming months.

All Eyes On The Fed

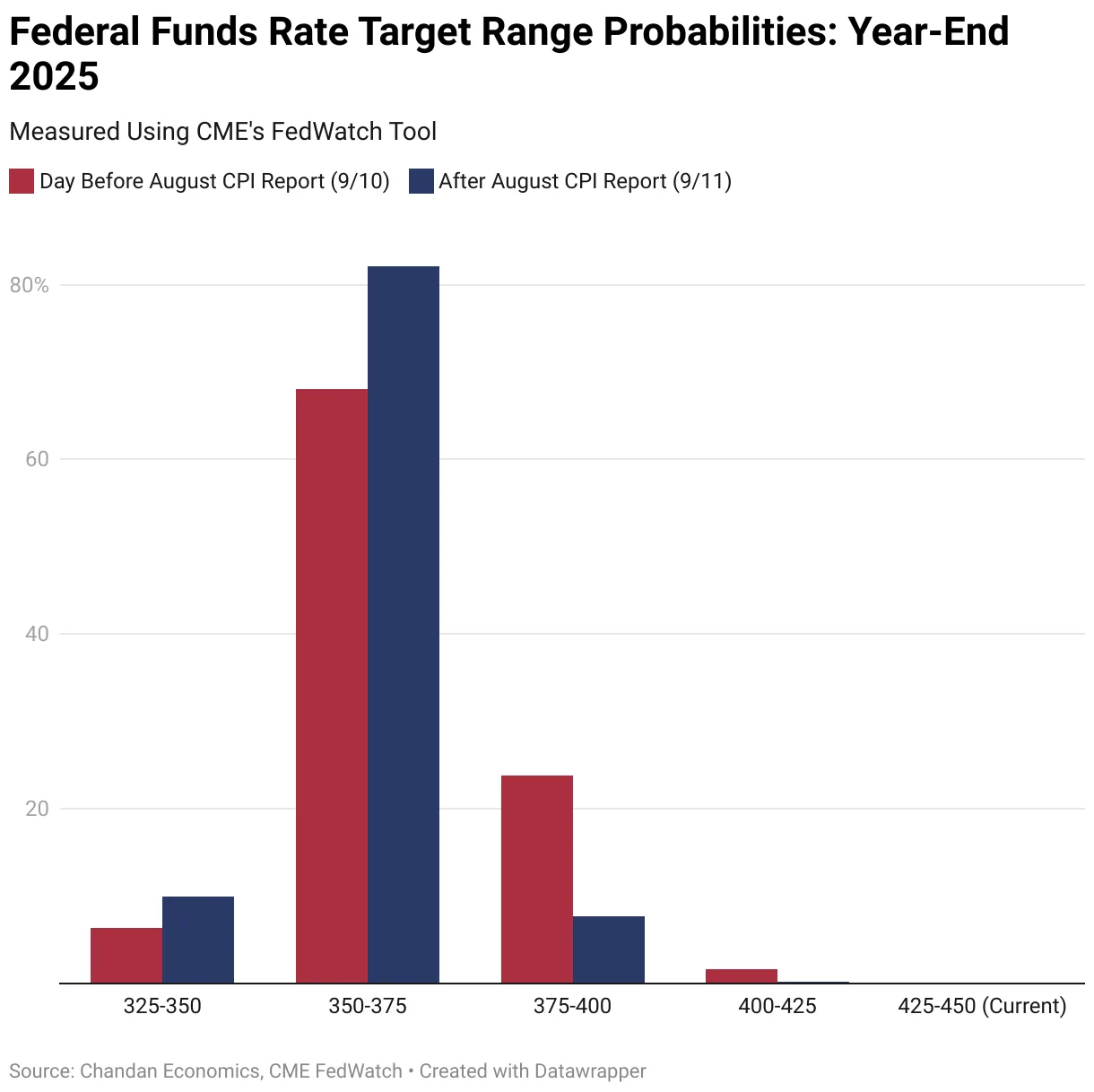

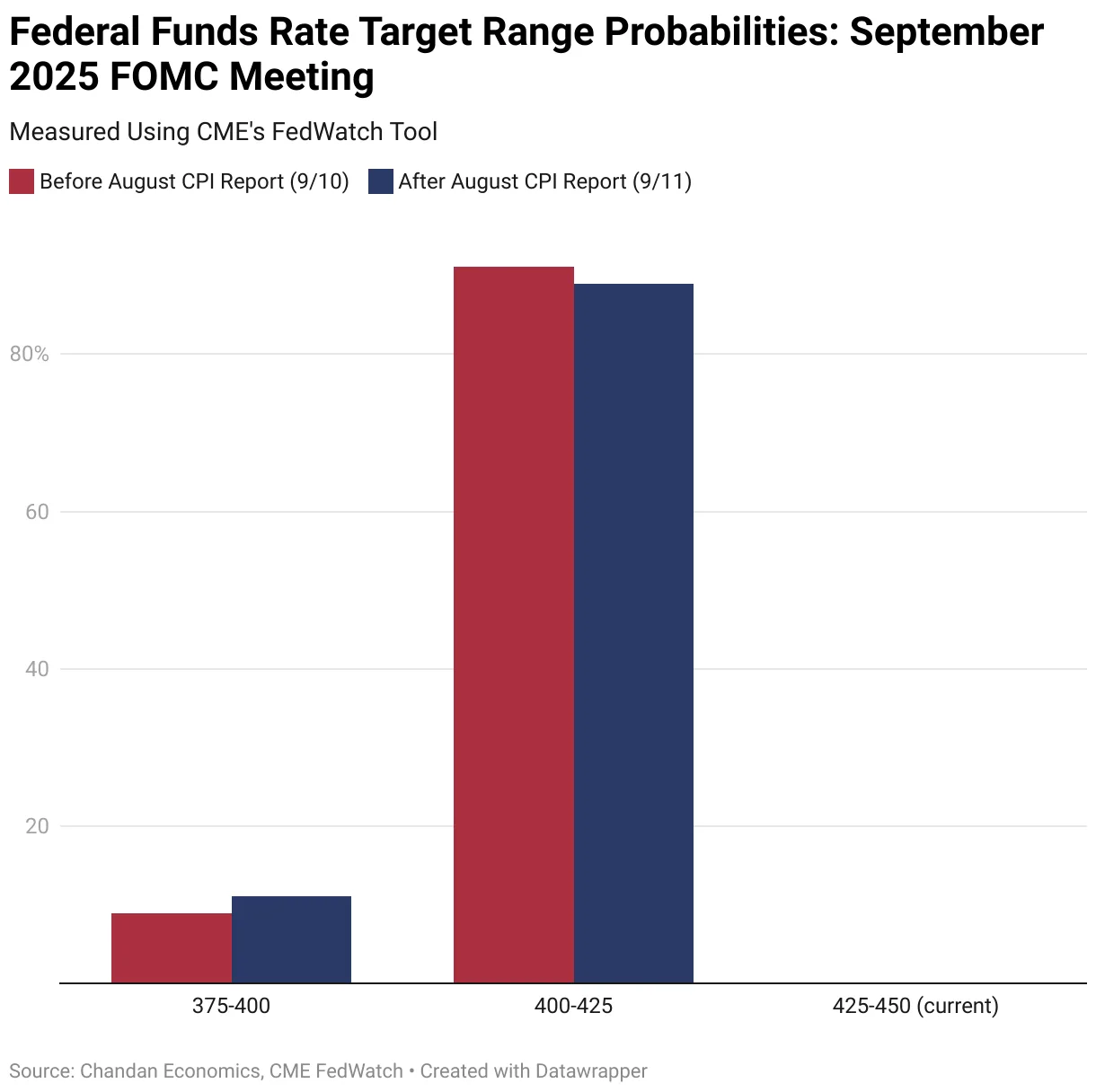

Federal Funds futures held steady following the CPI release, with traders pricing in continued rate cuts through year-end. According to CME FedWatch data:

- The odds of a 25-basis point cut at the Fed’s next meeting dipped slightly from 91.1% to 88.1%.

- The chance of a more aggressive 50-basis point cut rose modestly from 8.9% to 11.9%.

More significantly, markets are now almost certain that two or more cuts are coming before the end of 2025—with a 92.1% chance of three or more cuts. That dovish turn follows not only the CPI data but also weak August jobs numbers. In addition, downward revisions revealed the economy added 911K fewer jobs than previously reported over the past year.

A Welcome Shift For Borrowers

The Fed’s shifting stance is welcome news for the rental housing sector. It’s especially beneficial for multifamily developers and builders, who have been squeezed by high borrowing costs and tighter capital markets.

Lower interest rates would:

- Reduce financing costs for ground-up development.

- Improve project feasibility amid rising construction costs.

- Ease pressure on cap rates, which have widened in the face of higher Treasury yields.

For renters, the benefit is indirect. While inflation remains a concern—especially for housing costs—lower rates could spur more supply in the long term, eventually easing affordability pressures.

Caution Flags Remain

Despite the dovish tilt, risks remain. The slight CPI uptick could signal that tariff-related costs are starting to bleed into consumer prices, even though producer prices actually fell in August. If inflation continues to rise—even modestly—it could delay or complicate the Fed’s timeline for cuts.

The Fed is now balancing two competing forces: a weakening labor market and persistent—but manageable—inflation. While the path toward rate cuts is clearer than before, it’s not without hurdles.

What’s Next

The next FOMC meeting will be a critical test of how much inflation the Fed is willing to tolerate in the face of slowing job growth. For now, rental housing developers can be cautiously optimistic that lower rates are on the way—offering some long-awaited relief.

Stay tuned: With inflation still running warm, and labor data cooling fast, the Fed’s next move could define the outlook for rental housing well into 2026.