- The self-storage sector’s growth slowed in 2Q24 due to lower occupancy and street rates. Average same-store revenue growth inched down (-0.2%) for the first time since 3Q20.

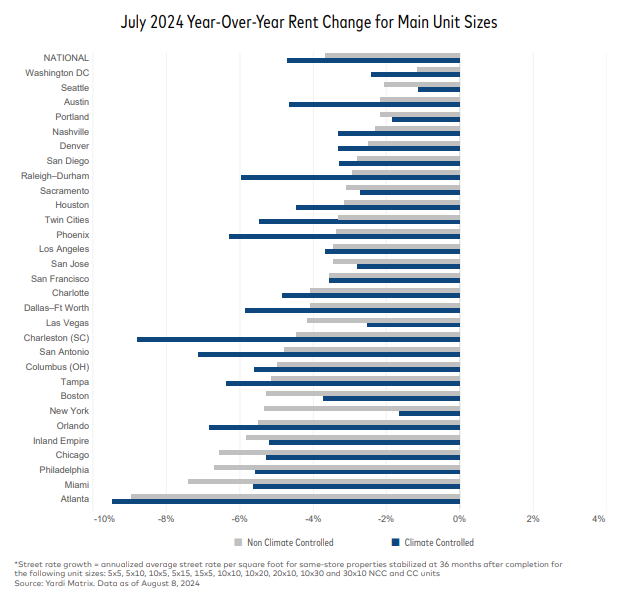

- Nationwide, advertised self-storage rates fell 4.1% YoY in July, up from prior months. All top 30 metros saw declines in climate-controlled (CC) and non-climate-controlled (NCC) units.rn

- The national self-storage construction pipeline equaled 3.5% of existing stock, with forecasts predicting more pullbacks and contraction through 2026–2029.

The U.S. self-storage market is facing a serious slowdown in growth in 2H24, with lower occupancy rates and slipping street rents putting pressure on the sector.

Self Storage Slowdown

According to Yardi Matrix’s August 2024 report, the self-storage sector is decelerating, driven by a combination of oversupply in key markets and softer demand.

The report offers a detailed breakdown of performance across the country, including rent trends, supply pipeline updates, and market-specific highlights.

Self Storage Slowdown

In 2Q24, average same-store revenue growth dipped into negative territory for the first time since Q3 3Q20, a decline driven by lower occupancy rates and street rates.

Performance varied across markets, with some—like New York, Denver, and Washington, D.C.—showing strength after underperforming in previous years. In contrast, sun belt markets like Cape Coral, Orlando, and Atlanta faced challenges due to an oversupply of new units.

Nationwide Trends

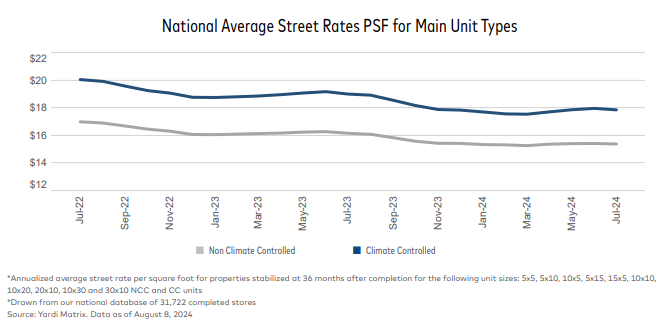

Nationally, advertised rates for self-storage units continued to fall YoY in July. The average nationwide PSF rate tumbled to $16.40, down from $17.28 in July 2023.

Although the annualized decline was 4.1%, this marks a slight improvement compared to earlier months in 2024. Self-storage REITs also saw a sharp drop in advertised rents (-5.3%) compared to non-REIT competitors (-3.7%).

Regional Performance

Some metros experienced unique market dynamics, with self-storage and multifamily sectors aligning.

Washington, D.C., stood out for its solid performance in both sectors, while cities like Atlanta struggled with declining rents in both self-storage and multifamily markets due to high levels of new supply.

Supply Pipeline

Nationally, self-storage development activity is decelerating, with the total construction pipeline shrinking to 3.5% of existing stock.

Yardi Matrix forecasts that new supply will moderate to 3.2% in 2024 and 2.6% in 2025, with further declines expected in coming years as developers pull back on new projects.

For now, Sacramento has emerged as the top metro for under-construction projects, overtaking Orlando, which is seeing a slowdown in new deliveries.