- Self storage new supply forecast for 2026 and beyond increased by Yardi Matrix.

- National advertised rental rates stabilized and began modest growth in late 2025.

- Development pipelines for planned and prospective projects continue to contract.

- Long-term supply is now expected to bottom above prior forecasts at around 1.7% of stock.

Self Storage New Supply Forecast Raised

Yardi Matrix has increased its self storage new supply forecast in its Q1 2026 update, citing an uptick in construction starts and a larger under-construction pipeline. Forecast completions for 2026 are now 6% higher than previously estimated, reaching 51.1M NRSF, while 2027 is forecasted up by 4.8% to 44.0M NRSF.

Completions projections for later years are also raised, with the 2028 self storage new supply forecast up 13.7% to 37.6M NRSF and 2029 up 15% to 38.0M NRSF, indicating a higher bottom than earlier scenarios.

Stabilizing Fundamentals and Pipeline Activity

Advertised rental rates for self storage stabilized in 2H 2025, increasing 0.3% year-over-year in December after previous declines. Together with rising construction starts, these indicators suggest market stabilization and support the higher self storage new supply forecast for the coming years. This shift comes as supply growth begins to moderate, even as elevated construction costs and capital constraints continue to shape development decisions across the sector.

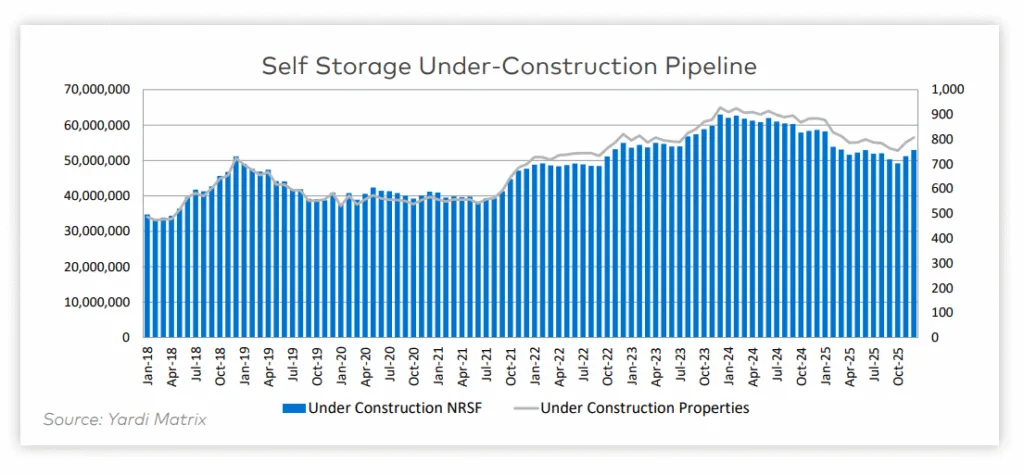

The under-construction pipeline rose 5.3% quarterly to 52.96M NRSF, reversing declines since 2023. Most of this volume is set to deliver in 2026 or early 2027. However, development remains hindered by high interest rates and sluggish home sales—key drivers that continue to cap new supply and underlying demand. The average construction completion time reached a series high of 431 days (14.4 months) for properties finished in Q4.

Development Pipeline Contraction Persists

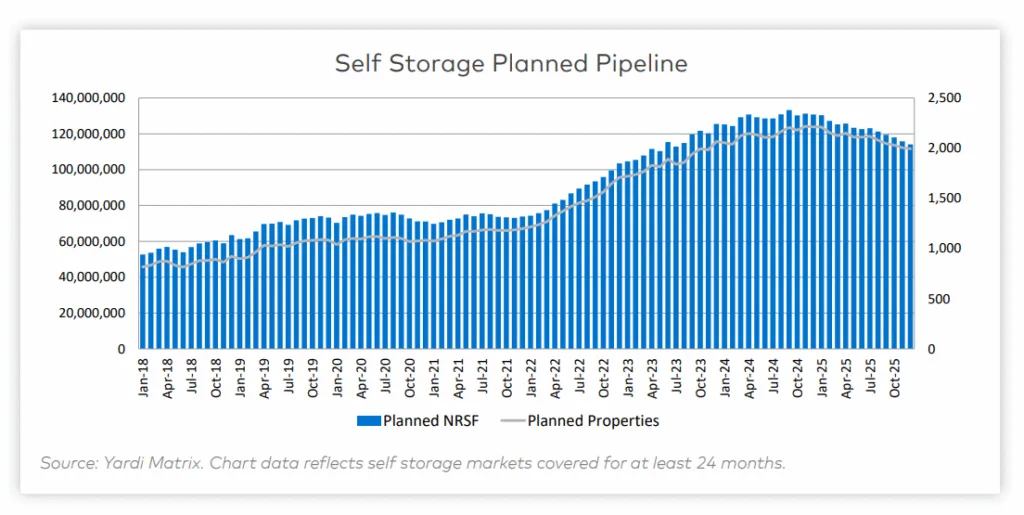

The planned self storage pipeline declined 4.6% Q/Q and 12.8% Y/Y, now sitting at 114.1M NRSF for established markets. The planned pipeline remains 2.15 times larger than the under-construction pipeline, but shrinking plans and long ‘days in planned’ reflect ongoing hesitation among developers. The prospective pipeline dropped 6.8% Q/Q and 21.7% Y/Y, now at 31.5M NRSF—down over 40% from its 2023 peak, nearing pre-pandemic levels. Deferred projects, although down 8.1% in Q4, remain more than twice the size of the last cycle’s peak.

Outlook and Bottom Line

Yardi Matrix expects self storage supply to remain above prior forecast troughs over the long term. The firm now models supply at 1.7% of total stock through 2031. Stronger rental rate trends and a modest rebound in construction starts support this outlook.

However, long-term development interest remains subdued. Planned and prospective pipelines continue to shrink. Deferred projects also remain elevated, limiting broader expansion plans.

If rental rate growth and construction momentum continue through 2026, Yardi Matrix could raise its forecast again. For now, supply growth should moderate. Even so, it will likely stay above previous cyclical lows.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes