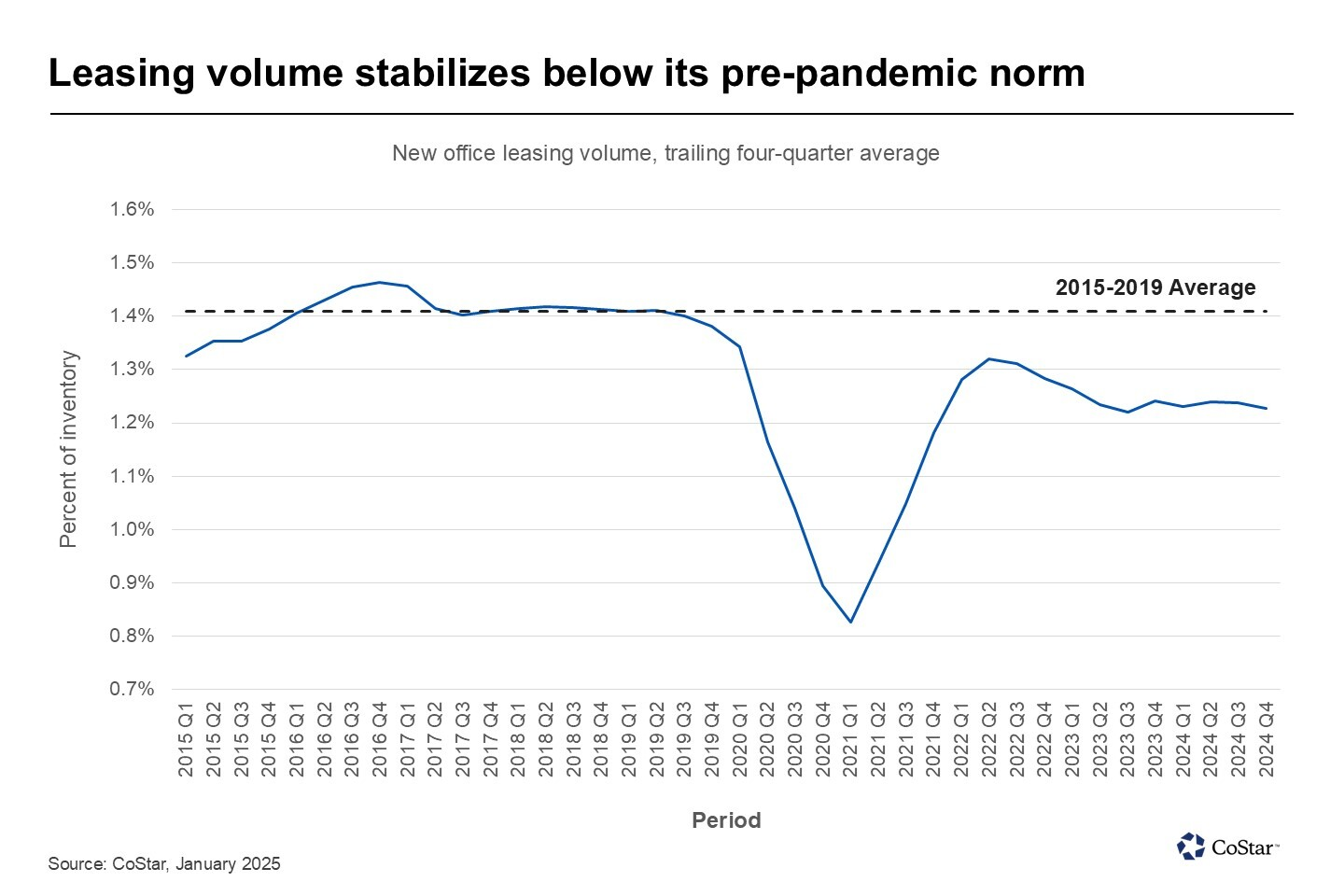

- Office leasing volume in 2024 reached 417 MSF, a consistent 1.2% of inventory per quarter, signaling stability in the market.

- While still below pre-pandemic levels, leasing activity has been resilient as companies adjust to new space needs and fewer move-outs.

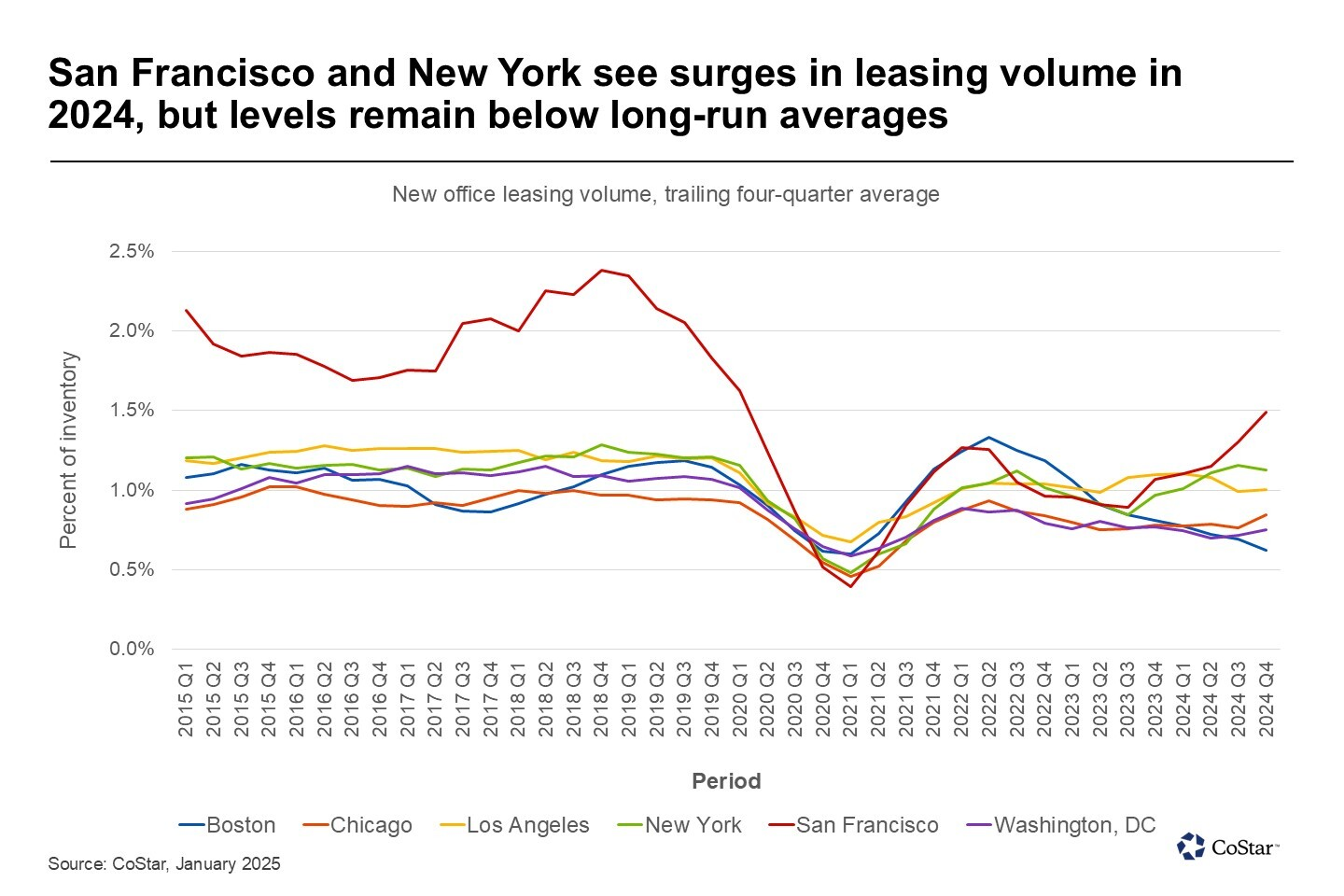

- San Francisco saw a remarkable 40% spike in leasing volume in 2024, one of the highest growth rates nationally, alongside Austin.

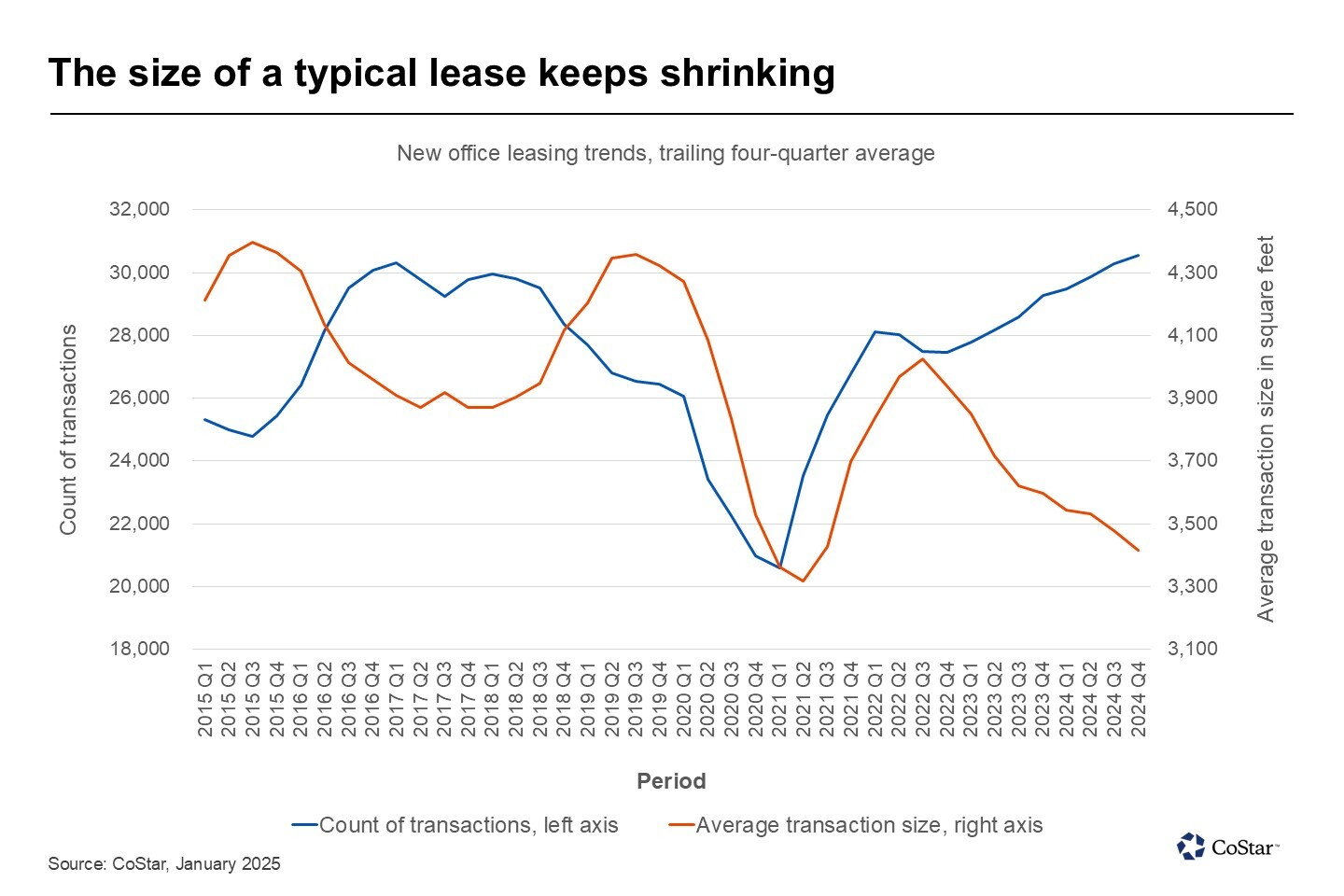

- Despite overall smaller lease sizes, leasing activity is robust, with new deals averaging just over 3.4 KSF.

The US office leasing market found a new equilibrium in 2024, showing both stability and cautious growth as companies adapt to the post-pandemic landscape.

While leasing volumes are still below the peak levels seen before the pandemic, the past year marked a significant recovery, per CoStar.

US leasing activity has remained steady since late 2022, providing a foundation for demand growth, as tenants slow their downsizing efforts and settle into more permanent office space arrangements.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Stable Leasing, Slow Recovery

In 2024, tenants signed for around 417 MSF of office space, approximately 1.2% of the total office inventory per quarter. This has been a consistent trend since at least the end of 2022, suggesting the office market has stabilized after the uncertainty of the pandemic years.

However, the leasing volume remains about 13% below pre-pandemic levels, indicating a continued adjustment to smaller office footprints and more flexible workspace arrangements.

The steady leasing pace signals that while companies aren’t returning to the large office spaces of the past, they are finding stability in their current office footprints. This has allowed overall occupancy to stabilize, even as the leasing activity remains somewhat subdued.

The trend of tenants executing smaller leases, averaging 3.4 KSF, has also persisted, revealing the broader shift to more compact, efficient office spaces.

Shifting Leasing Landscape

Despite a nationwide trend of smaller office lease transactions, certain markets saw notable exceptions in 2024. San Francisco and Austin were standout performers, indicating some regions are seeing stronger office leasing recovery than others.

San Francisco saw a dramatic 40% spike in office leasing volume in 2024, making it the leader among major US markets. By Q4, leasing volume had reached 1.5% of the market inventory, a significant rebound from the slow leasing activity seen in previous years.

Although still below the pre-pandemic 2% leasing level, the city’s recovery suggests demand for office space is gradually returning, particularly as companies weigh the benefits of having a physical presence in the city’s key business districts.

Austin was the only market to surpass San Francisco in leasing growth. The city’s booming tech industry and influx of new residents continue to fuel demand for office space, resulting in a larger-than-expected surge in leasing activity.

Falling Leasing Trends

In contrast to the positive performance seen in San Francisco and Austin, other US office markets continued to struggle with lower leasing activity.

Markets like Boston, for example, showed a steady decline in leasing volume throughout 2024, with the Q4 leasing volume dipping to just 0.6% of inventory.

On the other hand, New York showed encouraging signs of recovery in 2024, with 16% higher leasing volume compared to 2023. This rise was led by a surge in leasing activity during the final months of the year, bringing the city’s office leasing figures close to pre-pandemic norms.

Looking Ahead

As we head into 2025, the US office leasing market appears to be on a slow but steady path toward recovery. While leasing volumes remain below historical averages, certain cities like San Francisco and Austin provide optimism that demand is not just stabilizing but slowly recovering.

The trend toward smaller office spaces, however, is likely to continue, reshaping the market as companies optimize their real estate strategies to align with hybrid work models and evolving employee needs.